Yahoo Finance

Yahoo Finance The Seeing Machines (LON:SEE) Share Price Is Up 168% And Shareholders Are Boasting About It

It hasn't been the best quarter for Seeing Machines Limited (LON:SEE) shareholders, since the share price has fallen 26% in that time. But that doesn't detract from the splendid returns of the last year. Like an eagle, the share price soared 168% in that time. So it is important to view the recent reduction in price through that lense. The real question is whether the business is trending in the right direction.

See our latest analysis for Seeing Machines

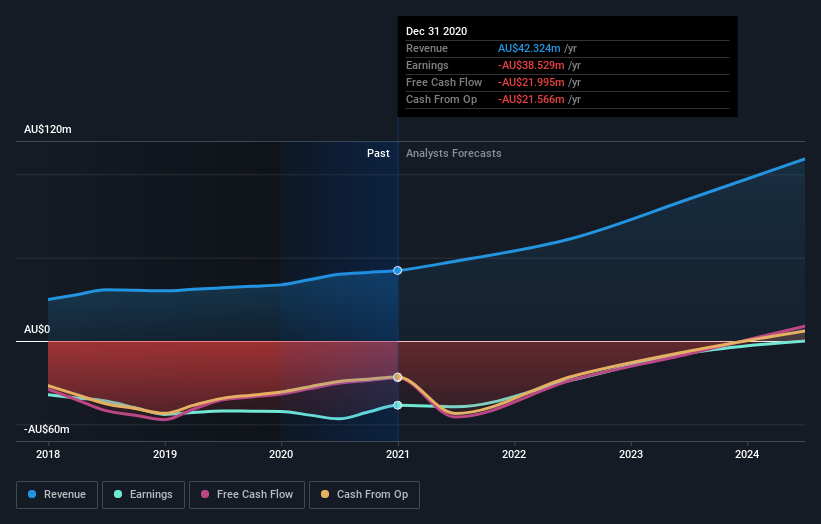

Because Seeing Machines made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

Seeing Machines grew its revenue by 26% last year. That's a fairly respectable growth rate. The revenue growth is decent but the share price had an even better year, gaining 168%. If the profitability is on the horizon then now could be a very exciting time to be a shareholder. But investors need to be wary of how the 'fear of missing out' could influence them to buy without doing thorough research.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

This free interactive report on Seeing Machines' balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

We're pleased to report that Seeing Machines shareholders have received a total shareholder return of 168% over one year. That gain is better than the annual TSR over five years, which is 15%. Therefore it seems like sentiment around the company has been positive lately. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. It's always interesting to track share price performance over the longer term. But to understand Seeing Machines better, we need to consider many other factors. Case in point: We've spotted 3 warning signs for Seeing Machines you should be aware of.

But note: Seeing Machines may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on GB exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.