Yahoo Finance

Yahoo Finance SEHK Growth Companies With High Insider Ownership And At Least 15% Revenue Growth

Amidst a backdrop of fluctuating global markets, the Hong Kong stock market has shown resilience, with the Hang Seng Index recently witnessing a significant gain. This context sets an intriguing stage for investors interested in growth companies with high insider ownership in Hong Kong, particularly those demonstrating robust revenue growth. In current market conditions, companies that combine substantial insider stakes with strong financial performance may offer valuable stability and alignment of interests between shareholders and management.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

Name | Insider Ownership | Earnings Growth |

iDreamSky Technology Holdings (SEHK:1119) | 20.1% | 104.1% |

New Horizon Health (SEHK:6606) | 16.6% | 61% |

Fenbi (SEHK:2469) | 32.1% | 43% |

Meitu (SEHK:1357) | 38% | 34.3% |

Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.5% | 79.3% |

Adicon Holdings (SEHK:9860) | 22.3% | 29.6% |

Tian Tu Capital (SEHK:1973) | 34% | 70.5% |

Beijing Airdoc Technology (SEHK:2251) | 26.7% | 83.9% |

Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 15.7% | 100.1% |

Ocumension Therapeutics (SEHK:1477) | 17.7% | 93.7% |

Let's take a closer look at a couple of our picks from the screened companies.

China Ruyi Holdings

Simply Wall St Growth Rating: ★★★★☆☆

Overview: China Ruyi Holdings Limited operates as an investment holding company, focusing on content production and online streaming in the People's Republic of China, Hong Kong, Europe, and internationally, with a market capitalization of approximately HK$25.37 billion.

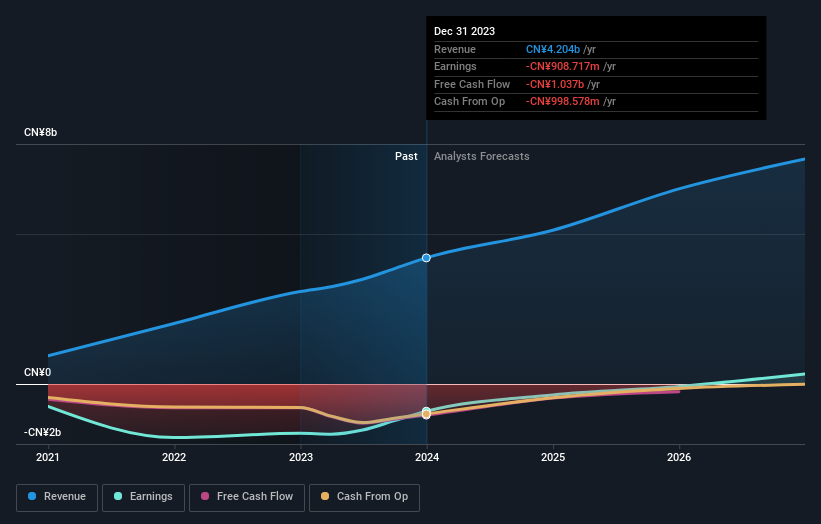

Operations: The company generates revenue primarily through its content production business, which brought in CN¥2.23 billion, and its online streaming and gaming segments, which together accounted for CN¥1.38 billion.

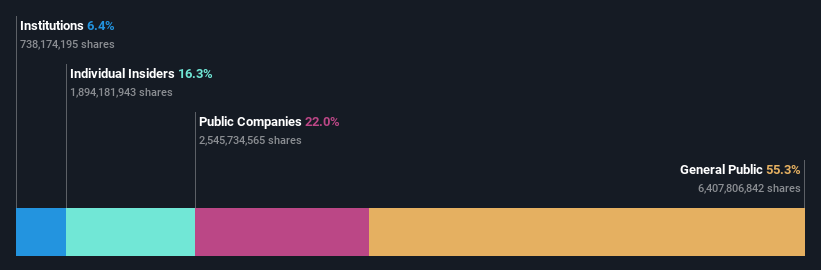

Insider Ownership: 16.3%

Revenue Growth Forecast: 27.7% p.a.

China Ruyi Holdings is trading at 67.2% below its estimated fair value, indicating potential undervaluation. The company's revenue growth at 27.7% per year outpaces the Hong Kong market average of 8%, with earnings expected to grow by 14.7% annually, slightly above the market's 12.2%. However, profit margins have declined from last year's 59.8% to current levels of 19%, and recent financial results show a decrease in net income and earnings per share compared to the previous year, despite substantial sales growth from CNY1.32 billion to CNY3.63 billion.

Dongyue Group

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Dongyue Group Limited operates as an investment holding company, focusing on the manufacture and distribution of polymers, organic silicone, refrigerants, and other chemical products across China and globally, with a market capitalization of approximately HK$16.48 billion.

Operations: Dongyue Group's revenue is primarily derived from polymers (CN¥4.55 billion), refrigerants (CN¥5.48 billion), and organic silicon (CN¥4.86 billion).

Insider Ownership: 15.4%

Revenue Growth Forecast: 15.4% p.a.

Dongyue Group Limited shows a robust earnings growth forecast at 35.7% per year, significantly outpacing the Hong Kong market average of 12.2%. However, its return on equity is expected to remain low at 12.9% in three years, and recent financial reports indicate a sharp decline in net income from CNY 3.86 billion to CNY 707.79 million year-over-year, alongside reduced revenue and basic earnings per share. Recent board changes and executive resignations could signal shifts in corporate governance or strategic direction.

Beijing Fourth Paradigm Technology

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Beijing Fourth Paradigm Technology Co., Ltd. is an investment holding company that delivers platform-centric artificial intelligence solutions in the People's Republic of China, with a market capitalization of approximately HK$23.99 billion.

Operations: The company's revenue is generated from three primary segments: the Sage AI Platform, which contributes CN¥2.51 billion, SageGPT AIGS Services at CN¥0.42 billion, and Shift Intelligent Solutions totaling CN¥1.28 billion.

Insider Ownership: 22.8%

Revenue Growth Forecast: 19.3% p.a.

Beijing Fourth Paradigm Technology, despite its volatile share price, is set to increase shareholder value through a recent buyback initiative. The company's revenue growth at 19.3% annually outstrips the Hong Kong market average. Although its return on equity is projected low at 6%, earnings are expected to surge by 95.97% per year, with the firm becoming profitable within three years. This growth trajectory underscores its potential amidst high insider ownership and strategic repurchases enhancing earnings per share.

Key Takeaways

Get an in-depth perspective on all 52 Fast Growing SEHK Companies With High Insider Ownership by using our screener here.

Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready For A Different Approach?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:136SEHK:189SEHK:6682

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com