Yahoo Finance

Yahoo Finance Shareholders in Cooper-Standard Holdings (NYSE:CPS) are in the red if they invested five years ago

Statistically speaking, long term investing is a profitable endeavour. But unfortunately, some companies simply don't succeed. To wit, the Cooper-Standard Holdings Inc. (NYSE:CPS) share price managed to fall 68% over five long years. That is extremely sub-optimal, to say the least. Furthermore, it's down 23% in about a quarter. That's not much fun for holders. This could be related to the recent financial results - you can catch up on the most recent data by reading our company report.

Now let's have a look at the company's fundamentals, and see if the long term shareholder return has matched the performance of the underlying business.

Check out our latest analysis for Cooper-Standard Holdings

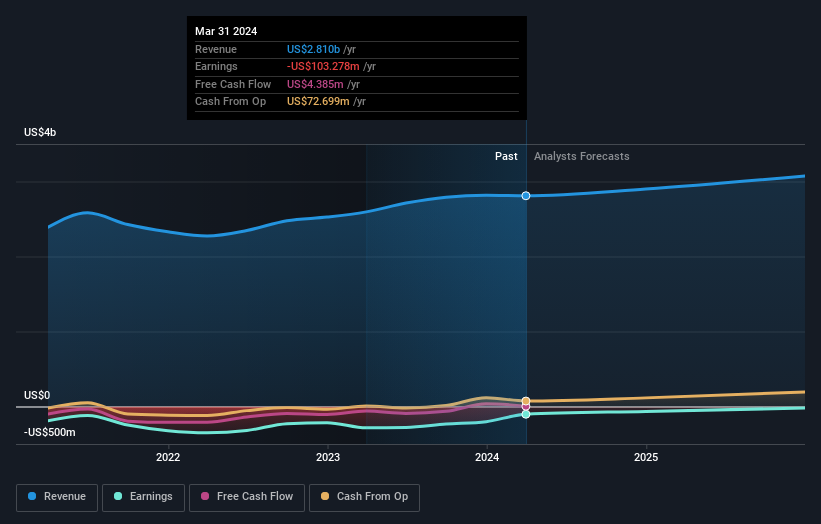

Cooper-Standard Holdings wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. When a company doesn't make profits, we'd generally hope to see good revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

Over half a decade Cooper-Standard Holdings reduced its trailing twelve month revenue by 3.9% for each year. That's not what investors generally want to see. With neither profit nor revenue growth, the loss of 11% per year doesn't really surprise us. The chance of imminent investor enthusiasm for this stock seems slimmer than Louise Brooks. Not that many investors like to invest in companies that are losing money and not growing revenue.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

Take a more thorough look at Cooper-Standard Holdings' financial health with this free report on its balance sheet.

A Different Perspective

It's nice to see that Cooper-Standard Holdings shareholders have received a total shareholder return of 44% over the last year. There's no doubt those recent returns are much better than the TSR loss of 11% per year over five years. This makes us a little wary, but the business might have turned around its fortunes. It's always interesting to track share price performance over the longer term. But to understand Cooper-Standard Holdings better, we need to consider many other factors. For example, we've discovered 3 warning signs for Cooper-Standard Holdings (1 doesn't sit too well with us!) that you should be aware of before investing here.

Of course Cooper-Standard Holdings may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.