Yahoo Finance

Yahoo Finance Low-income Americans need more wealth — not more debt

It’s been said of academia that the fights are so vicious because the stakes are so small. The same could be said of fights over bank regulation. Take the current heated debate over banks’ obligations to lend to low and moderate income (LMI) communities under the Community Reinvestment Act (CRA). Regulators are arguing over the right metrics to use in crediting banks with CRA lending. But they are failing to ask the more fundamental question of whether increased debt is really the right way to help financially vulnerable families.

The CRA was enacted in 1977 to combat the then-prevalent practice of banks “red-lining” economically distressed neighborhoods as no-credit zones. Banks would happily extract deposits from families living in those areas, but would deem them too risky for loans. With the CRA, Congress aimed to reverse the harmful impact of redlining by imposing affirmative obligations on FDIC-insured banks to lend in the low and moderate income (LMI) areas that they serve.

Two of the three banking regulators, the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC), have proposed changes to CRA regulations, arguing that they need to be modernized. They point out that technology has expanded the reach of banks’ lending far beyond their brick and mortar locations, and want to give banks more leeway to make CRA loans in neighborhoods remote from their physical facilities. They want to expand the kinds of lending that qualify for CRA credit and revise the way banks are scored. Low-income community advocates have attacked the changes as diluting CRA effectiveness. The Federal Reserve has refused to sign on to the proposed changes, and the FDIC published them on a divided vote.

A new problem for lower income communities

I do not discount the importance of these disagreements. The CRA has provided tremendous benefits to LMI neighborhoods. But the problem it was designed to address is not the problem that confronts these communities today. In 1977, the problem was a credit shortage for lower income families. Now, it is the existence of too much credit, often high-cost and aggressively marketed to financially distressed households. With consumer debt once again at historic highs and disproportionately falling on low-income families, the government’s focus should be on helping those families build wealth and reduce reliance on debt. True modernization would focus on this reality.

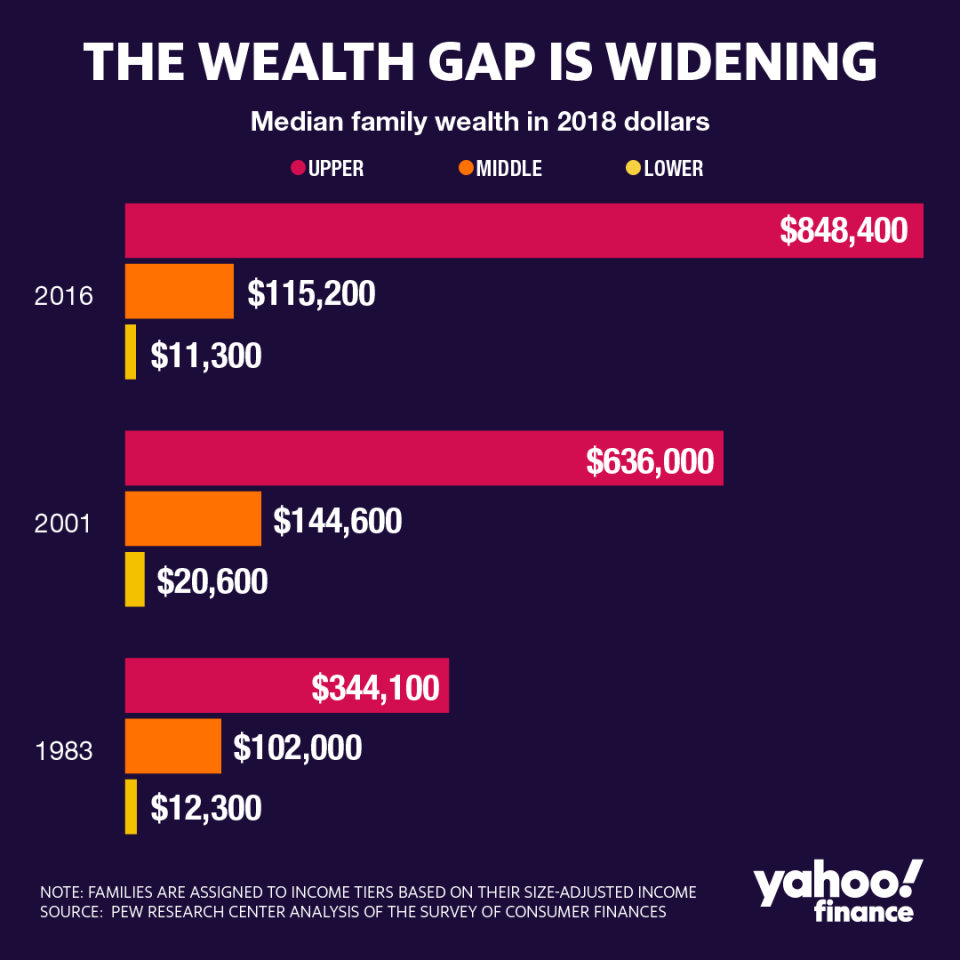

The financial crisis and its aftermath took a terrible toll on LMI communities. Massive foreclosures stripped them of any chance to recover lost home equity. Job loss hit them hardest and even after regaining employment, they suffered years of stagnant wage growth. Available data indicate that their real net worth is substantially lower than it was in 2001, even as the wealth of high-income families has soared.

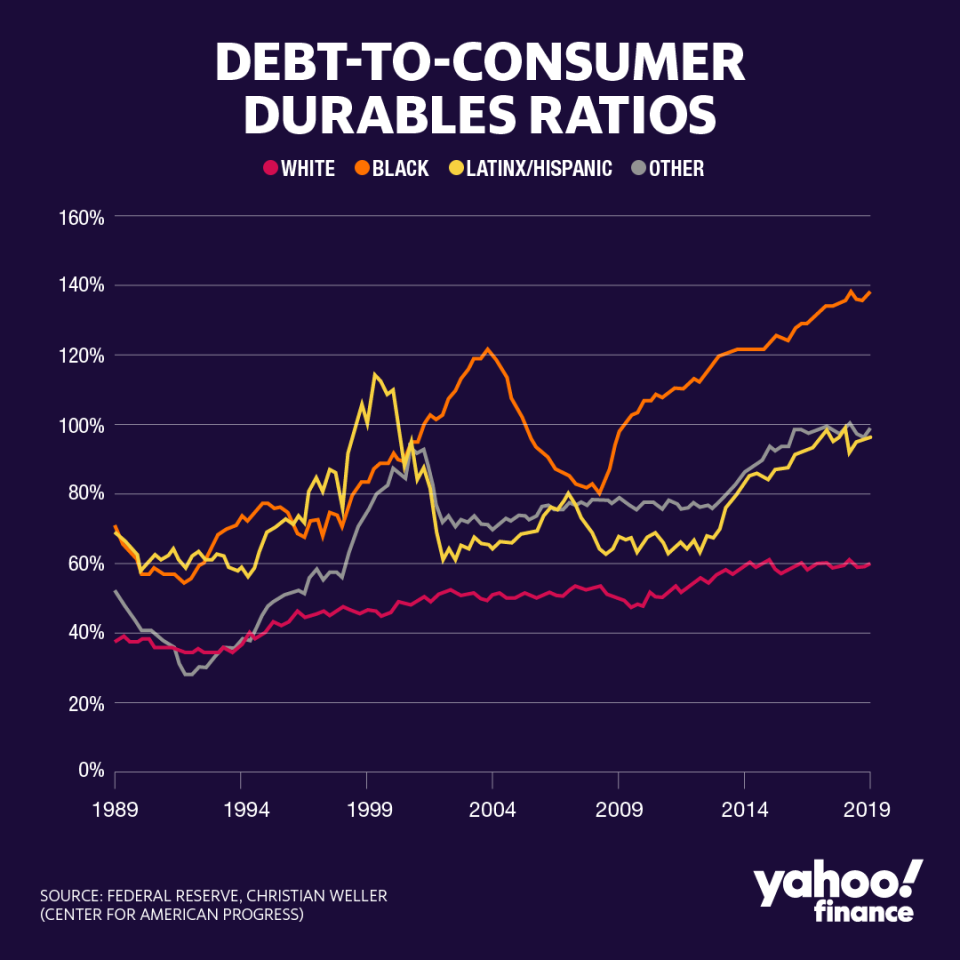

African-American families are in particular trouble. They are the only group whose debt exceeds the value of the goods they own. And the debt they owe carries substantially higher interest costs than that owed by white families.

The 2008 financial crisis underscores the folly of excessive debt as a path to upward mobility. Critics of CRA have argued that it caused the subprime mortgage crisis by pressuring banks to make unaffordable home loans to LMI families. That is categorically false. Greed drove the crisis. Lenders gave risky mortgages to subprime borrowers to make money, and the overwhelming majority of subprime loans were made by nonbank lenders. According to Federal Reserve data, only 6% of subprime loans were made by CRA lenders. At the same time, while CRA did not drive the crisis, it was used to reward bad behavior. Six percent of over 7 million subprime borrowers is not insignificant, and now-discredited lenders like Countrywide and IndyMac were given satisfactory CRA ratings by their regulators. Government encouragement for even one of these abusive loans was one too many.

A new focus on wealth building — and away from lending

Regulatory missteps during the subprime crisis underscore the risks in the government trying to direct profit-seeking banks to lend to financially inexperienced borrowers. Congress should consider reorienting CRA to wealth building, and away from lending. Let’s reward banks working with their mortgage borrowers to build home equity through regular pay-down of principal rather than giving them credit for cash-out re-financings or home equity loans. Let’s laud banks offering no-fee, interest bearing savings accounts to help LMI families build next eggs, instead of showering them with high-interest credit cards. Let’s encourage banks to contribute scholarship funding to support low income students instead of lending to students already maxed out on government borrowing.

If we are going to impose affirmative obligations on banks, then we should celebrate those that can demonstrate they are helping build wealth for their customers. Banks will continue to make all sorts of loans, but the only ones the government should encourage through CRA are those that demonstrably contribute to wealth building and financial security. The CRA does need to be modernized, but in a way that will meet the current needs of the communities it was meant to help. At-risk families need to improve their net worth, not get deeper into debt.

Regrettably, CRA is just one example of how government policies continue to encourage borrowing in the misguided belief that debt expands economic opportunity and growth. We have piled $1.5 trillion of student debt on the future of our young people. We continue to provide massive subsidies for other forms of borrowing and further encourage it through ultra-low interest rates. But debt is not a sustainable engine for prosperity. Borrowers can only borrow so much. Eventually it needs to be repaid. A vibrant middle class supported by real wage growth and wealth accumulation is the only path to lasting economic health.

Sheila Bair is the former Chair of the FDIC and has held senior appointments in both Republican and Democrat Administrations. She currently serves as a board member or advisor to a several companies and is a founding board member of the Volcker Alliance, a nonprofit established to rebuild trust in government.

Read more:

Why student loan forgiveness should target graduates who need it the most

Why the Fed should oversee Facebook’s Libra

How regulators can stop leveraged lending from becoming the new subprime

The $1.4 trillion student loan market faces a huge issue — transparency

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.