Yahoo Finance

Yahoo Finance The Silicon joke? London's journey from universal derision to Europe's biggest tech hub

Exactly 10 years ago, in March 2008, a small technology company called Doppler waved goodbye to its cramped premises above a pub in Hoxton in London’s East End, and relocated to a bigger office nearby, on 100 City Road.

For Doppler’s 32-year-old chief technology officer, Matt Biddulph, the move offered a double advantage. Not only was there more space, but it also opened a door into a young, energetic social world of pub nights and parties, where coders, software engineers, budding entrepreneurs and digital wannabes gathered to gossip and share tales of triumph and disaster in their efforts to build online businesses.

At the heart of this world was Moo.com, which was developing both a customised printing business and a reputation for great booze-ups. And it just so happened that Doppler’s new office space was sublet from Moo.

“It was very sociable,” Matt Biddulph recalls now. “There were a good number of companies in the area. Friday nights we would always go round to someone’s place for a few drinks, a barbecue on the roof.”

After a few months, it dawned on Biddulph that this disorganised but congenial congregation of digital companies amounted to London’s very own technology hub. He reckoned that if Britain had an equivalent to California’s all-conquering Silicon Valley - home to Google, Facebook, and Apple - he was at the heart of it.

Directly out of his window was Old Street’s grey, dreary, deeply uninspiring, traffic-clogged junction - gleaming City towers and Georgian Bloomsbury facades to the south and west, Hackney Marshes and London Fields to the north and east. California it wasn’t. So, tongue firmly in his cheek, he took to the then new social media platform, Twitter, and wrote: “‘Silicon Roundabout’: the ever-growing community of fun start-ups in London’s Old Street area.”

It was meant to be funny, a very British acknowledgement of the gulf that existed between the scale and ambition of America’s technology titans - which promised nothing less than a revolution in human communication and commerce - and our own, rather more humble aspirations, to print nice stationery, perhaps, like moo.com.

“It was absolutely a joke,” says Biddulph. “There was this classically British community of people, creating a bunch of great things, but with a healthy dose of cynicism.”

Ten years on, Silicon Roundabout is no longer a joke. In fact, after the continent economies of America and China, this country has become - by almost any metric - the most powerful technology hub in the world. Indeed by some measures, such as start-ups per capita, Britain now beats the United States.

Last year, London raised more than twice the amount of money to fund digital companies than any other city in Europe. Between 2012 and 2016, total investment in Britain reached £28bn, as much as our closest three rivals - France, Germany, the Netherlands - combined.

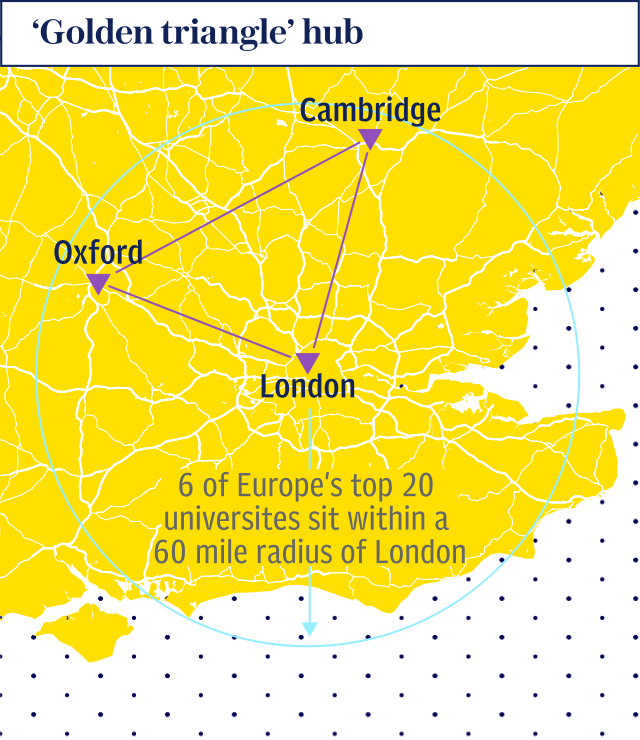

One reason is obvious. Britain is home to eight of Europe’s top 20 universities. The “golden triangle” of Oxbridge and London alone offers six within a 60-mile radius.

The results are equally evident: some 40 per cent of Europe’s “unicorns” - new tech companies worth $1bn or more - are British. If their names - Deliveroo, Rightmove, Transferwise - are not familiar to you yet, they will be soon, changing everything about the way you eat, live, and spend.

Growth is phenomenal. According to the Government’s digital strategy, published last year, fixed internet traffic in Britain is doubling every two years, while mobile data traffic increases by more than 40 per cent annually. Around the world, the volume of global internet traffic in 2020 will be almost 100-fold greater than it was shortly before Matt Biddulph coined the phrase Silicon Roundabout, and connected devices will outnumber the global population by nearly seven to one.

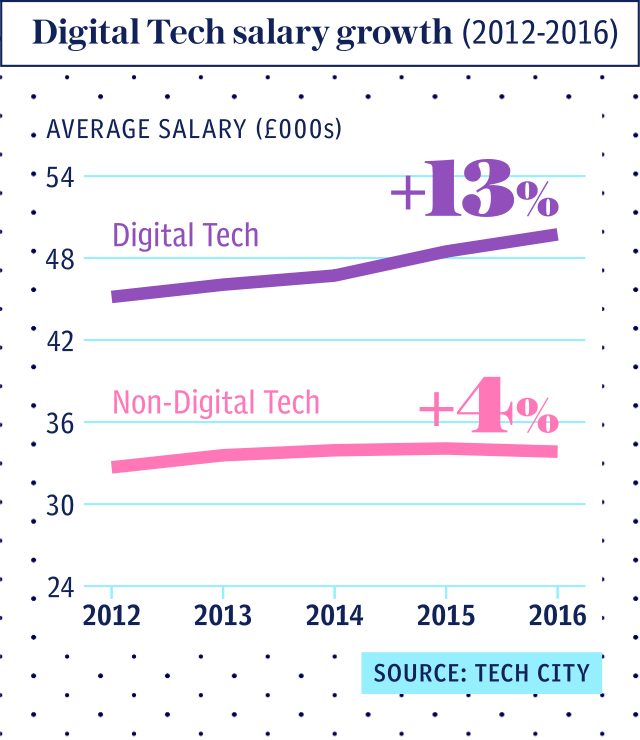

To fuel that astonishing development, Britain’s so-called digital economy, already home to 1.6million workers, will suck in an estimated half million new recruits in the next four years. It is a high-growth, high-productivity sector in a country where, for the last decade at least, both have been been a problem. Average salaries for British tech workers - more than £50,000 - are half as much again as the typical annual wage.

The bashful, forelock-tugging Silicon Roundabout of a decade ago now attracts global tech titans to its door. The world’s largest technology fund, run by Japan’s SoftBank, with $100bn to invest, set up shop in Mayfair last year.

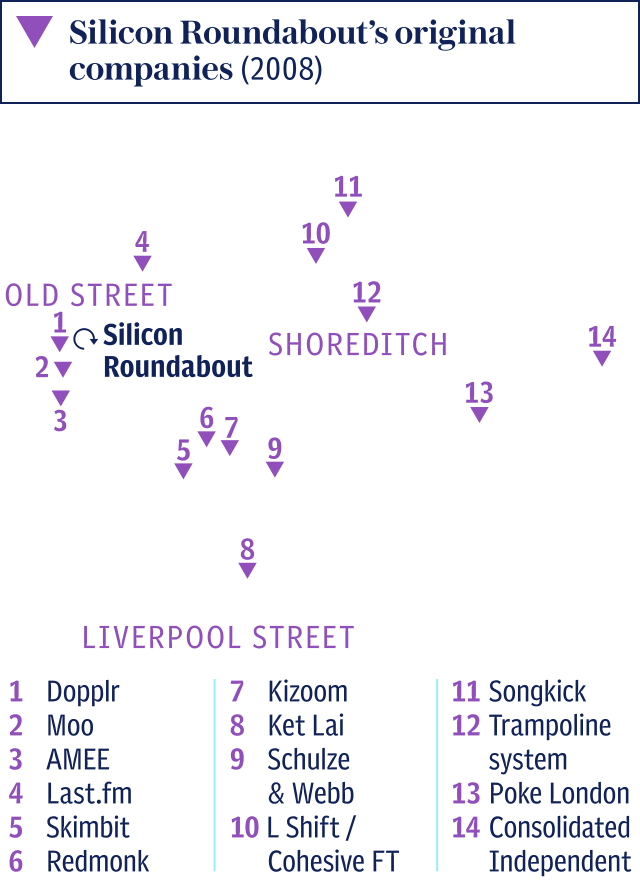

Meanwhile Google is developing a huge campus around King’s Cross, much of it devoted to its British artificial intelligence (AI) offshoot, DeepMind, which it acquired in 2014 for $500m. And Facebook is finalising plans to open a huge new headquarters in the same area. When Matt Biddulph drew up a map of Old Street start-ups in 2008, it featured 16 companies.

Now London has an estimated 6,000. Far from being a road to nowhere, Silicon Roundabout has taken this country a long way.

Not that the cultural chasm to Silicon Valley has been completely bridged. According to Saul Klein, one of the most influential investors in British technology, “Silicon Valley is a mindset, not a location. It’s about energy, ambition - an almost on-the-spectrum desire to make something without really thinking about the consequences of what you’re trying to do.”

Harry Briggs, a venture capitalist specialising in early-stage technology companies, puts it more bluntly: “In Britain if you’re offered $50m or $100m to sell your company you think: ‘I can be one of the richest people I know, and a big success’.

In Silicon Valley if you sell for $100m you’re a nobody, you’re a loser. I heard someone from Silicon Valley say recently they want to be remembered as long as Julius Caesar. That’s just a different scale of self-belief and ambition.”

America has seen plenty of digital emperors. Bill Gates, of Microsoft, ruled the desktop age. Steve Jobs, of Apple, dominated the move to mobile. Mark Zuckerberg, of Facebook, foresaw the rise of, and then conquered, social media. Not to mention Amazon’s Jeff Bezos, or Tesla’s Elon Musk, both of whom already seem to have tired of earthly conquest and set their eyes set on space. Can Britain produce a figure of similar stature?

On a February day, with blizzards sweeping the monolithic grey facades along Whitehall, and London feeling a world away from California, it is up to

Matt Hancock, the newly-appointed, fresh faced and habitually red-socked Secretary of State for Digital, Culture, Media and Sport, to provide the sunny disposition.

And he does, enthusiastically recounting how, since coming to office (in coalition) in 2010, his party has helped the British tech sector emulate American audacity in myriad ways.

One fundamental part of the transformation the Conservatives claim credit for has occurred within the corridors of power themselves. Until recently, the institutional reflex there was to hoard the vast troves of information that the state gathers in all its guises: central and local government spending, civil servant salaries, you name it; the numbers and spreadsheets were jealously guarded.

Then, a young policy advisor called Rohan Silva, talent-spotted by then chancellor George Osborne, drove a whole new agenda: open data. As Matt Hancock notes: “Instead of being closed, the default became that government data sets were open unless there was a good reason.”

It was the movement that would come to allow private developers to build businesses around public sector information - whether school performance tables or the location and timeliness of buses. As a result, commuters now routinely plug in a destination on their mobiles and cross cities using real-time public transport information. Residents can see exactly how many burglaries there have been in their street.

“The first serious move was crime data, released by Theresa May,” says Hancock. “But the open data agenda was driven from David Cameron down.”

Government, whose services are today undergoing their own digital revolution at the hands of Liam Maxwell, Britain’s first National Technology Adviser, can justifiably claim credit for other encouraging gambits, too.

One is Tech City, founded and funded in 2010 by Cameron, to nurture young companies around Silicon Roundabout. Another was the tax credit SEIS, introduced in 2012 to tempt investors to back risky new ventures; a third is the British Business Bank, founded in 2014, which allocates enormous sums to venture capital funds to disburse to new tech companies.

Brexit means British companies will lose access to £2bn of EU investment, but, as Hancock says, “we’ve already committed the British Business Bank paying extra funds, to assure that the current European funding is at least matched”.

If government played its part, though, the two things that most drove the British tech sector into the mainstream occurred well before David Cameron’s arrival as prime minister, and had little to do with politics. The first was the recycling of talent from those few companies that had surfed (and sometimes been sunk by) the first major wave of the internet boom. Perhaps most famous of these was lastminute.com, the site which made household names of its founders Brent Hoberman and Martha (now Dame Martha) Lane Fox.

From his office just off Kensington High Street, Hoberman now talks about “the mafia” - tight-knit groups of employees who worked in pioneering digital firms in the early to mid-2000s, then emerged to form a host of new companies themselves.

“There was the Skype mafia, the Betfair mafia, the Lastminute mafia,” he says. “All came out with experience and the confidence to build new things. From lastminute we’ve probably had 10 who started business worth over 100 million, just out of that mafia.”

Much more important, however, was 2008, and the financial crash. If there was a single event that transformed British technology, it was the crash. Almost overnight, large numbers of highly-motivated people with serious financial experience were fired. A huge talent pool was dumped onto the open market.

“The crash pushed a whole load more people to want to be entrepreneurs,” says Hoberman. “Entrepreneurship is really risky. Then it turned out that so is working in a bank, so a lot more brilliant people said: ‘Well, why not be an entrepreneur?’”

The City had been a veritable talent Hoover. “So many founders have come to start-ups having left a Goldman Sachs,” says Sarah Drinkwater, who runs Google Campus, near Old Street, where refugees from the Square Mile can pull up a stool at a shared desk, log on to the free wifi, and plug away at their business idea. Every day, dozens of new members post a sticker on the campus notice board to announce who are they are and what they’re doing. “They’ve either just been made redundant or are at an inflection point in their lives,” says Drinkwater.

The crash didn’t just affect the people who had been fired. It changed the mindset of those looking for their first job, too. For generations, the best and brightest had emerged from universities and were tempted to make money in the City that they could not make elsewhere.

But after the crash, a career in banking was freighted not only with risk, but also with some stigma. Banking was out, tech entrepreneurship was in.

“Of my 100-strong graduating class,” says Suranga Chandratillake, who left Cambridge with a degree in computer science 20 years ago, “the biggest employer was the City. Almost one third became bankers. Last year, the biggest employer was Entrepreneur First” - a prestigious “incubator” for start-ups whose embryonic firms are often then snapped up by investors like Chandratillake himself, now a venture capitalist at Balderton Capital. “Goldman Sachs is having to compete hard to be attractive again for graduates,” he says.

The challenge is about more than money. Time and again in Britain, you hear the phrase “tech for good”. Founders of new companies believe they can have it all: money, prestige and a company which changes lives for the better.

Gordon Gecko might despair, but greed alone is no longer good. The most talented today want to be rich and have a shiny conscience. “They ask: ‘How can I actually do good in the world?’” says Mustafa Suleyman, one of the founders of DeepMind. “I think people really do care. There’s this judgement about the cultures of other industries, like the banking of the past. There’s some tough judgement about.”

Or as Gerard Grech, CEO of Tech City, puts it: “Tech can be a force for good. That’s part of the UK tech brand, and I’ve not seen it elsewhere in the world.” Chandratillake concurs: “If you look at Millennials, it’s about money and success, of course, but it’s also about mission and sense of social achievement. Tech has managed to have a positive story to tell. For example Transferwise [a slick, low-cost, user-friendly online money transfer service] sells itself as being the living embodiment of everything traditional financial services are not.”

Of course the City will survive the British technological revolution. Indeed its dominance and talent pool have helped make this country a world leader in new digital financial platforms just like Transferwise - collectively known as fintech - which offer everything from current accounts to mortgages to investment accounts, most controlled through your mobile phone.

But the tech revolution will not be so kind to other celebrated names on the British high street, or their employees. For while technology is helping build new businesses, it is helping to kill old ones. Adapt or die is the mantra now.

One famous casualty looks likely to be Marks & Spencer. Beloved by many, M&S has failed to keep pace with the developments in e-retailing. Observers note how it has not carved out a clear strategy, neither establishing itself as a market leader in-store, or online. In the language of the industry it is trying both “bricks” and “clicks” - and failing at both. “M&S is not going to be a going concern on its own in the next five years, they’re not going to make it,” says Russ Shaw, the influential founder of Tech London Advocates, a 4,000-strong group dedicated to championing the capital as a hub for digital businesses. “Tech is hitting everything. On the high street, either you’re going to go a Primark route, where there’s no online, or you’re going to be an adopter like John Lewis, which is looking pretty adept. But M&S are not cutting it. Their website is clunky. If you’re going to survive as a retailer you’ve got to be on the cutting edge of it.”

There is an irony here. Lord Stuart Rose, who was chief executive of M&S from 2004-2010, went on to lead the pro-EU Britain Stronger in Europe campaign ahead of the referendum in 2016. As it turned out, there was an existential threat to his former business, but it was technology, not Brexit.

By contrast, technology businesses, which pride themselves on their adaptability and ingenuity, are more sanguine about Brexit than you might imagine. There are certainly concerns about access both to European talent and the Digital Single Market - which aims to allow online companies and websites to operate easily across the EU, just as mobile phones do since roaming charges were abolished last year. But at Tech City, where Gerard Grech keep tabs on all the key statistics, all is not doom and gloom. “The three top countries for tech skills immigrants coming to this country in 2016 [the last year for which data is available] were not in the EU but the US, India and Australia,” he notes. “So the UK should not be shy. We have taken a risk leaving the EU, in a self-determining way. With risk must come opportunity, otherwise what’s the point in doing it? This entrepreneurial community says we’ll rise to this challenge. Entrepreneurial risk culture is part of making this a success. As we leave the EU, the whole country has to be readied to make the most of the change that is coming. It will be a constant revolution, for which we will need to psychological fitness, staying power and resilience. It’s a state of mind. The country needs to be ready for that.”

Some in the tech world moan that such positivity does not always radiate from the Prime Minister, Theresa May. That, at just the moment a cheerleader is required, we have a dour manager in charge. “We’re expecting the Government to create the conditions to allow business to thrive,” says Dom Hallas, who until January was an official at the Department for Exiting the European Union but is now Executive Director of Coadec, which acts as an intermediary between start-ups and government. “One of the challenges we have, quite frankly, is that unfortunately we have a PM who… is not very business minded. That’s the reality. And so concerning.”

More than that, Hallas says that Mrs May’s default response to technology is wariness and suspicion -, that where others see opportunity, she sees threats. “You start a conversation about technology and within two sentences you’re talking about paedophiles. It’s extraordinary. It’s baffling. That’s the [official] mindset that frankly flows from the top.”

It was significant, therefore, that Mrs May chose artificial intelligence as the theme of her speech in Davos this year. For many, Britain has a real opportunity to become a world leader in the field. DeepMind may have been bought by Google, but it remains in London - a platform which draws machine learning pioneers from around the world, and from where they can go on to create countless AI spinoffs of their own.

Suleyman, who says DeepMind has “made London the leading city in the world for AI” calls “Terminator-style super intelligence a long-term speculative fantasy, and basically a distraction”. But he admits that “technologies, by their design, are not destined to be good”. Increasingly, therefore, the nature and imposition of regulation will be critical: “Reassurance comes from understanding the governance mechanisms for these technologies.”

Already technology companies are colliding with the state over the precise nature of that governance. Technology is not just about emails and texts any more. Uber is changing travel, Airbnb is changing housing. So called “Healthtech” - from wearables that can tell your your insulin levels, to repeat prescription notifications on your mobile - will sweep through the NHS. “Edtech”, facilitating online learning, will change the very basics of how the state’s teachers teach.

As companies unleash such revolution, they face increasing pushback from state regulators. Last year, Uber fought a legal battle against Transport for London over its reporting of criminal offences. Consumers are long used to seeing tech titans get their way, so it was something of a surprise when, in September 2017, Uber was found not “fit and proper” and stripped it of its licence.

“For things to exist at mainstream scale, one has to have governance,” says Saul Klein. “Obviously the EU model is top-down regulation, similar to the Chinese model. A lot of the US system is self-regulated. The UK has always sort of had a hybrid role. We strike the balance between self-regulation and regulation without stifling innovation. And I think the UK has a track record of playing that role, and it’s a massive opportunity now because ultimately these technologies, these innovations at scale, need to be regulated.” Or, as Matt Hancock affirms in bold terms: “Freedom operates within a framework. The Wild West for the tech companies is over.”

In particular, this will matter in the next 10-15 years, as companies amass huge amounts of data, much of it on individuals, and process it with highly sophisticated algorithms.

That, in essence, is AI. It’s what Mustafa Suleyman calls “the ability to extract structured knowledge from unstructured data”, and with it comes huge potential, but also significant risk. Suleyman, in his office in King’s Cross, thinks Britain is uniquely placed to balance the two.

“The technology industry in general is very rapidly learning to grow up and sensitively engage with the reality of the status quo. People are excited about disruption in some respects and threatened and intimidated by it when it is delivered in the narrowest, most crude form. I think the opportunity of developing these kinds of technologies in London is that we have an incredibly diverse, open, critical, multicultural city. And that means that many of those values bleed into the organisations. That is unique.”

Silicon Valley, he says, suffers from its technological solipsism. "Frankly that creates a particular culture which can appear tone deaf to the needs and requirements of other stakeholders in society.”

“I saw that when I was working with Microsoft in the late 1990s,” says Saul Klein. “There were no distractions and it was this ivory tower. Workers at Microsoft found it really hard to understand why people didn’t like them, or were angry with them. Facebook is going through that right now.”

Britain then, having come from nowhere, is now perfectly positioned to exploit the powerful emerging technologies of the coming decades. Free from the heavy state control of China or the EU, but attuned to the need to protect users from over-mighty companies, this country is striking a “golden mean”. London, in particular, has the advantages of size, without the problems of vast distance - which separates Silicon Valley's innovators in California, say, from US government in Washington.

“In London you’ve got everything. You’ve got consumers at scale, you’ve got enterprise buyers. It’s the largest English-speaking city in the world,” says Klein. “It’s Facebook’s number one English-speaking city; it’s Twitter’s number one English-speaking city. Any consumer service you want to launch you can launch it in London and you will know within 18 to 24 months: do people love this product or service? Are they prepared to pay for this? How much will they use it? Do the economics of this business work? If you tick all of those boxes you can grow very rapidly.”

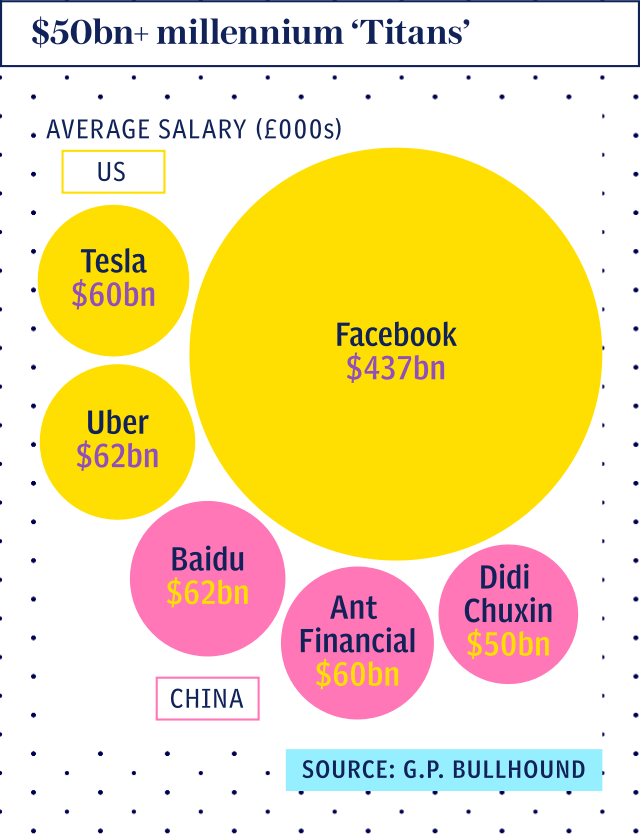

How far can Britain go? Well, of the 53 European billion-dollar tech companies, 22 are British. But growing much bigger is hugely difficult: globally only six companies formed since 2000 are now worth more than $50bn: Facebook, Uber, and Tesla in America, and search engine Baidu, Ant Financial and Didi Chuxing, a ride-sharing Uber-rival in China. Of these, Facebook is far ahead, valued at almost $500bn - half a trillion dollars. Yet some people believe that the world’s first trillion dollar company will be British.

Apple is currently worth $900bn. And Saudi Arabia’s state-owned oil company, Aramco, planning to float on the stock market, will probably be valued at considerably more than $1tn. But Apple, for all its cutting edge tech, is 42 years old. Aramco’s roots go back to the early 1920s.

“The world’s first trillion dollar company will be here,” says Sherry Coutu, who founded Interactive Investor International, and has made her name since as a serial entrepreneur. She is from North America, so her judgement is not down to blind loyalty. Rather, she says there is a confluence of two emerging technologies that, together, “will fix the whole world and you’ll be able to commercialise it on a global basis.” She thinks that one nation, a leader in both fields, will best exploit that confluence: Britain.

To get there, however, Britain still has a host of problems to overcome - in education, training and lack of diversity with tech; in transforming academic research into world-changing businesses and fostering a little more of the entrepreneurial ambition that drives Silicon Valley; in scaling-up promising new companies into “unicorns” worth billions; and finally in turning one of those behemoths into a trillion-dollar beast. How we get to do that, and the identity of that trillion dollar company, is the subject of this series.