Yahoo Finance

Yahoo Finance Solid State (LON:SOLI) Will Pay A Larger Dividend Than Last Year At £0.1325

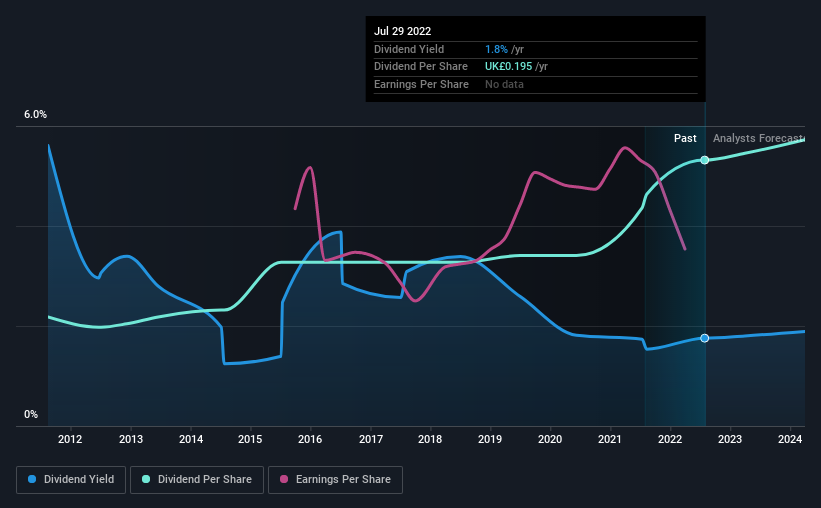

The board of Solid State plc (LON:SOLI) has announced that it will be paying its dividend of £0.1325 on the 5th of October, an increased payment from last year's comparable dividend. This will take the annual payment to 1.8% of the stock price, which is above what most companies in the industry pay.

Check out our latest analysis for Solid State

Solid State's Earnings Easily Cover The Distributions

If the payments aren't sustainable, a high yield for a few years won't matter that much. However, Solid State's earnings easily cover the dividend. This means that most of its earnings are being retained to grow the business.

Over the next year, EPS is forecast to expand by 109.8%. If the dividend continues along recent trends, we estimate the payout ratio will be 43%, which is in the range that makes us comfortable with the sustainability of the dividend.

Solid State Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. The annual payment during the last 10 years was £0.08 in 2012, and the most recent fiscal year payment was £0.195. This implies that the company grew its distributions at a yearly rate of about 9.3% over that duration. Dividends have grown at a reasonable rate over this period, and without any major cuts in the payment over time, we think this is an attractive combination as it provides a nice boost to shareholder returns.

Dividend Growth May Be Hard To Achieve

Investors could be attracted to the stock based on the quality of its payment history. Let's not jump to conclusions as things might not be as good as they appear on the surface. It's not great to see that Solid State's earnings per share has fallen at approximately 3.9% per year over the past five years. A modest decline in earnings isn't great, and it makes it quite unlikely that the dividend will grow in the future unless that trend can be reversed. Earnings are forecast to grow over the next 12 months and if that happens we could still be a little bit cautious until it becomes a pattern.

We should note that Solid State has issued stock equal to 32% of shares outstanding. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

In Summary

Overall, it's great to see the dividend being raised and that it is still in a sustainable range. The earnings coverage is acceptable for now, but with earnings on the decline we would definitely keep an eye on the payout ratio. Taking all of this into consideration, the dividend looks viable moving forward, but investors should be mindful that the company has pushed the boundaries of sustainability in the past and may do so again.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Taking the debate a bit further, we've identified 2 warning signs for Solid State that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here