Yahoo Finance

Yahoo Finance Starbucks Corporation's (NASDAQ:SBUX) Optimistic Valuation may put the Stock Price at Risk of Further Downside

This article originally appeared on Simply Wall St News.

Shares of Starbucks Corporation ( NASDAQ:SBUX ) have come under pressure in the last two trading sessions. The selling seems to have mostly been caused by Yum China ( NYSE:YUMC ) warning that its third quarter profits may fall more than 50% as a result of the spread of the Covid-19 Delta variant .

The other reason some investors have cited for the weakness is yesterday’s IPO of Dutch Bros ( NYSE:BROS ). Dutch Bros, which sells coffee and energy drinks, started trading with a market value of $5.6 billion. Some investors appear to see more upside for the smaller company, when compared to Starbucks.

Starbucks is trading on a price-to-earnings (or "P/E") ratio of 47.8x while the P/E ratio of the average US listed company is below 17x. Price-to-earnings ratios can tell us a lot about investor expectations, especially when we compare them to growth forecasts for a company.

Check out our latest analysis for Starbucks

Does Growth Match the High P/E?

A ratio of 47.8x isn’t unusual for a growth company, particularly one that has performed as well as Starbuck has over the last year. In the 12 months to June, Starbuck’s earnings grew 108%. However, this was off a low base, as trailing 12-months earnings growth was down between 60 and 82% in the previous four quarters. This wasn’t surprising as Starbucks was badly affected by the Covid-19 pandemic.

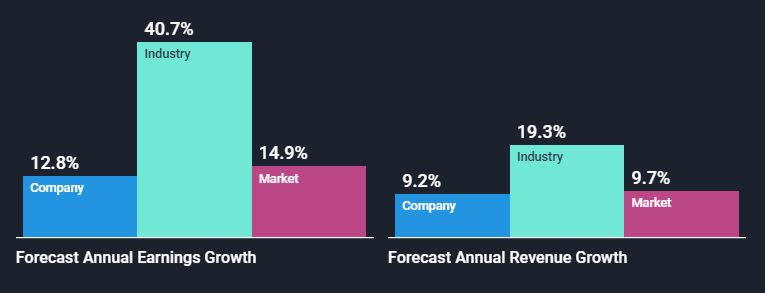

To really put the Starbucks P/E ratio in context we need to look at future growth forecasts. In order to justify its P/E ratio, Starbucks would need to produce outstanding growth well in excess of the market. Unfortunately, current forecasts don't suggest this will be the case.

The earnings and revenue forecasts for the next year are shown below. As you can see Starbucks is expected to lag its industry and perform broadly in line with the market. Analysts do have high expectations for the current quarter, but expect growth to slow after that. Looking further ahead, analysts are on average expecting earnings growth of between 13% and 16% out to 2025.

The Final Word

Starbucks P/E is actually quite low compared to where it has been historically. The P/E was a lot higher in the 2013 to 2015 period when the company was recording earnings growth rates above 20%. But, now that the company has over 30,000 stores worldwide, that sort of growth rate is more difficult to achieve.

The fact that the P/E ratio doesn’t line up with growth forecasts doesn’t mean Starbucks price will fall further. Forecasts may rise, or the stock may trade in a range until earnings catch up with the valuation. But it does mean investors should manage their expectations, and exercise caution. If earnings for the current quarter disappoint, the share price may be at risk.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Starbucks (1 doesn't sit too well with us) you should be aware of.

If these risks are making you reconsider your opinion on Starbucks , explore our interactive list of high quality stocks to get an idea of what else is out there.

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com