Yahoo Finance

Yahoo Finance This stock has trebled since we tipped it but is better value now than it was then

Few things are as alluring to investors as a growing dividend. Companies that are able to raise their payouts continually have widespread appeal, and not just to investors who focus on income.

That’s because they tend to be strong share price performers too. Rising dividends are usually the product of rising profits, which tend to prompt a rising share price.

The trade-off, however, is that companies with strong dividend growth tend to offer a lower initial yield than investors would be able to secure elsewhere.

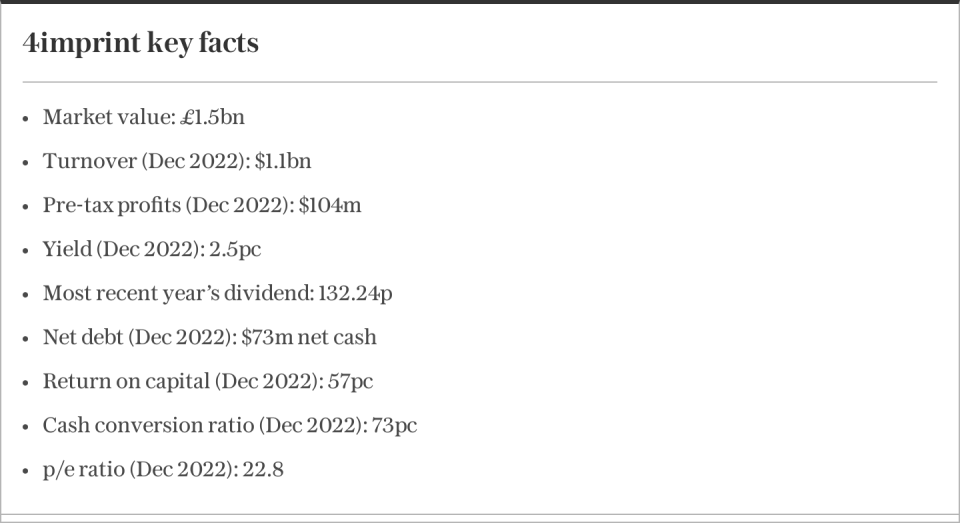

On the face of it, 4imprint, a distributor of corporate promotional products, fits that mould: its dividends have risen substantially over the past few years and its yield of 2.5pc is solid but not spectacular. Yet those facts tell only part of the story.

When Questor first tipped the shares six years ago at £17.68, we did so in part thanks to the prospect of special dividends as a cycle of capital expenditure ended and cash was building up on the balance sheet.

A substantial special dividend of 43.17p duly arrived the following May, which doubled the total payout to shareholders that year. It has taken another five years, but in June 4imprint, which makes the bulk of its money in America, paid its second special dividend.

In between, the company’s profits had been hit by Covid, leading it to suspend payouts, before both profits and dividends came roaring back.

It has been worth the wait: this year’s special dividend, at 165.38p, was nearly four times the size of the first.

Normal dividends have also grown significantly since they were reinstated and are now more than three times higher than when we first recommended the shares.

The share price has risen by 196pc since that tip, while the dividends of 477.06p paid since then, if reinvested, take the total return to 244pc – an outperformance of the FTSE 100 of 215 percentage points.

More than half of those cash returns have come in the past year, with a 297.62p total payout for the 2022 financial year if we include the special dividend, which equates to a yield of 5.7pc at the current share price. More than just solid, perhaps.

This has not been lost on professional investors.

4imprint’s strong growth and rising cash returns to shareholders have attracted some of the world’s best fund managers to its shares, according to the financial publisher Citywire, whose Elite Companies website rates companies on the basis on their backing by the top-performing 5pc of equity fund managers from its database of more than 10,000 across the world.

4imprint, which counts nine of these investors as backers, has secured its top AAA rating.

Samantha Gleave of Liontrust Asset Management is one of these top fund managers and an investor in 4imprint since 2019. She is eyeing continued growth in dividends and says investors won’t need to wait another five years for the next special.

“It wouldn’t surprise, given the cash returns they’ve got, if for 2023 they did announce another special dividend,” she says.

Profits would need to keep growing in order to fund such dividend rises and on that front both 4imprint’s record and guidance from the company are encouraging.

Revenues hit $1.1bn last year, 45pc higher than in 2021, although perhaps a fairer comparison is the 32pc rise on 2019’s sales, when the pandemic had yet to hit the business.

Pre-tax profits of $104m were 92pc higher than 2019 levels.

So far this year progress is strong: ahead of interim results, the company announced last week that it expected revenues of “slightly above” $1.3bn this year and pre-tax profits of more than $125m.

A lack of debt – 4imprint had net cash of $73m at the end of last year – together with a management team that is not prioritising acquisitions means that a lot of those profits should find their way back to shareholders.

Funding organic growth is the first priority for the cash it generates, but as a sales outfit, acting as a middleman between suppliers and customers, 4imprint’s investment requirements are not onerous.

The shares trade on 20 times forecast earnings. While that is not cheap, it is less expensive than they were on that measure when Questor first tipped them. This is a sign of how much earnings are growing, outpacing even the 196pc rise in the share price over that period. Keep buying.

Questor says: buy

Ticker: FOUR

Share price at close: £50.80

Daniel Grote is editor of Citywire Elite Companies, which rates companies based on their backing by the world’s best fund managers

Read the latest Questor column on telegraph.co.uk every Tuesday, Wednesday, Thursday and Friday from 6am

Read Questor’s rules of investment before you follow our tips