Yahoo Finance

Yahoo Finance StockRank Movers - March 3rd: Value in Greece

Greece has been making headlines recently. The left-wing Syriza party secured their election victory on the back of promises to end austerity measures, which have hitherto been a precondition for debt relief. The prospect of another Eurozone crisis is on everyone's mind again. Athens' main stock index was down 3.2% the day after Syriza's victory. The full impact of Syriza's policy may well take some time to play out, but at Stockopedia we couldn't help wondering whether there might be any opportunity to pick up good quality Greek shares at knock-down prices.

Is Greece undervalued?

At the start of 2014, Meb Faber (CEO: Cambria Investment Management) showed that Greek stocks were, on average, the cheapest in the world (see here). Faber uses the CAPE to analyse stocks. The CAPE, or cyclically adjusted P/E ratio, is defined as price divided by the average of ten years of earnings. It therefore seeks to smooth out the economic cycle and allow for better comparisons over time.

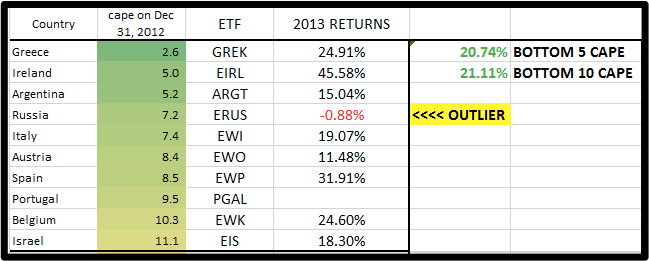

Faber's research suggests that companies, and indeed countries, with lower CAPEs tend to outperform countries with higher CAPEs. For example, in 2013 cheap countries like Greece and Ireland returned 24% and 45% respectively (see below);

(Source: CAPE Returns for 2013, Meb Faber Research)

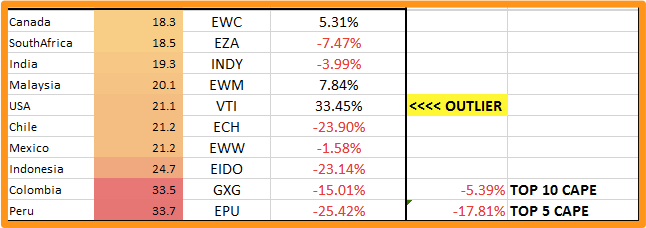

On the other hand, expensive countries like Colombia and Peru dropped by 15% and 25%...

(Source: CAPE Returns for 2013, Meb Faber Research)

Is Greece still cheap? We can use the StockRanks to see the wood through the trees and analyse individual stocks.

Aegean Airlines SA (AEGN)

Aegean Airlines (Greece's largest airline) has the characteristics of a recovery stock. A useful metric to identify cheap companies on the mend is the Piotroski F-Score, which looks for companies that are profit-making, have improving margins, don't employ any accounting tricks and have strengthening balance sheets. Aegean Airlines has a good F-Score - 8 out of 9.

This progress has been supported by network expansion, as well as the acquisition of Olympic Air in 2013. At one point it looked like the acquisition would be blocked by the European Commission, on the basis that the merger would have created a "quasi-monopoly" in Greece's air transport market. Aegean could now be better placed to charge higher prices from its passengers. The firm gained control of more than 90% of the Greek domestic air market when the merger finally went through.

However, Aegean currently has a P/E ratio of just 6.6. Why is the market pessimistic? The company still faces a weak domestic market. Revenues have also been unstable. They fell in 2010 then they rose in 2011, before dropping again in 2012. Perhaps this instability leads the market to view Aegean Airlines as a risky investment. However, the company's overall StockRank is 99.

FHL - Kiriakidis Marbles and Granites SA (KYRM)

Stocks sometimes become cheap when they are painted with the same common brush. For example, the Greek marble mining company, FHL, has a P/E ratio of just 4.3. FHL is Greek - and Greece faces microeconomic challenges. Perhaps FHL is cheap for a reason.

On the other hand, the market may have overreacted to bad news about the Greek economy. Two-thirds of the company's sales are made overseas in Europe, the United States, the Middle and Far East. Indeed, the company has recently supplied marble to huge construction projects including the Cathedral of Christ Saviour in Moscow's Red Square, the Grand Mosque of Abu Dhabi and the Uzbekistan Parliament building.

Furthermore, FHL has a high return on capital employed (27%) and strong profit margins (37%). Why is the company so profitable? Their Volakas quarry in northern Greece covers a surface area of 350,000 square meters. This makes it the largest quarry of Volakas marble in the world, enabling FHL to run operations on an economy of scale basis. FHL also enjoys a virtual monopoly (85%) of the Greek Volakas marble market, placing it in a good position to charge higher prices. The company has a low MomentumRank (36), but also has a top decile ValueRank (90), QualityRank (95) and overall StockRank (91).

Conclusions

In you want to learn more about the CAPE, see this article by Faber for more details, as well as this paper for longer-term results. As always - these are not share tips and should not be read as investment advice. Please do your own research before investing.

Read More about Aegion on Stockopedia

Discuss Aegion on Stockopedia