Yahoo Finance

Yahoo Finance StockRanks - upgrades and downgrades - October 14th: MOSB; MTC; IGG; CAY

This column usually analyses stocks on a company by company basis, but we will take a different approach this week and compare companies within particular sectors. In the consumer cyclicals sector, we contrast Moss Bros with Mothercare. In the financial sector, IG Group goes head to head with Charles Stanley.

Consumer Cyclicals: Moss Bros vs. Mothercare

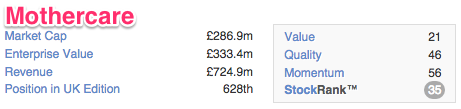

Moss Bros has a StockRank of 81, up 20 from last week, while Mothercare has a StockRank of 35. Last week it was 41. What is Moss Bros doing right? What is Mothercare doing wrong?

Sales growth (Quality)

Both companies have enjoyed different fortunes when it comes to sales growth. Moss Bros has managed to grow revenues each year since 2011. This is thanks partly to online sales. Internet sales doubled over the last half year. They now account for around 7% of total revenues. The company also continues to develop new products, having recently launched a series of sub-brands, including Moss London, Moss 1851 and Moss Esquire. Brokers predict that these products will help the company grow revenues by around 5% in 2014.

The picture is more gloomy for Mothercare, where sales have consistently fallen since 2012 and are expected to fall again in the twelve months to March 2015. Weaker footfall and price cutting have both worked to hit sales and margins.

Productivity (Quality)

Both companies are becoming more productive. Moss Bros has a Piotroski score of 7 out of 9 and is more productive than it was last year. Asset turnover can be used to measure productivity. It shows how effective a company is at using assets to generate revenues. Moss Bros asset turnover is now 1.9, compared to 1.8 last year. The company closed 9 stores for refurbishment last year and another 14 units will be refurbished in the second half of their year. The company’s management team claim that their refurbished stores deliver a sales increase of between 8 to 10 per cent in the first year. Mothercare has a lower Piotroski score of 5 out of 9, but generated a higher asset turnover this year compared to last year. The company has closed 80 UK stores under its restructuring plan to date and at the start of the year announced that it could make 500 staff redundant.

Broker forecasts (Momentum)

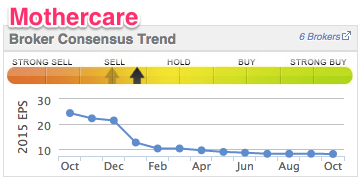

The brokers have been getting increasingly optimistic about Moss Bros. The EPS estimate has risen from 3p to 3.5p over the last year - an increase of 16%. Its a different story at Mothercare. In October 2013, the brokers EPS consensus was 24.42p, but this has now fallen massively to 8.2p. The respective earnings consensus for both companies has essentially moved in the opposite direction, as the charts below show.

Financials: IG Group vs. Charles Stanley

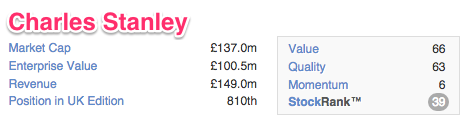

IG Group has a StockRank of 87, up from 78 last week. On the other hand, Charles Stanley’s StockRank has dropped from 44 to 39 over the last week.

Profitability and sales growth (Quality)

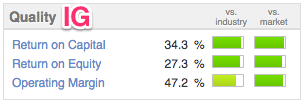

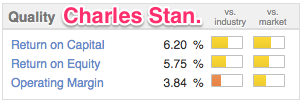

Charles Stanley and IG have respective QualityRanks of 63 and 99. This difference can be attributed mainly to both company’s profitability levels. Indeed, Charles Stanley issued a profit warning in September, noting that profit margins were under pressure after low transaction volumes continued to hit commission income. The company’s operating profits have indeed dropped from 10.3% (2011) to 3.8% (2014), whereas IG’s operating profits have grown to 47.2% (2014), up from 40% (2010). Net profits were also down by a massive 29% at Charles Stanley (Year end March 2014), whereas net profits edged up by nearly 4% at IG (Year end May 2014). IG’s client numbers have dropped by 13%, but the average revenue per client rose by 19%, as the company tried to retain only those clients with the highest levels of trading activity.

Momentum

The market has unsurprisingly responded to Charles Stanley’s profit warnings by driving the share price down. The graph below shows a sharp drop when the profit warning came in early September. The company has indeed underperformed the market by a massive 32% over the last twelve months and now trades 43% below its 52 week high. IG Group has not exactly rallied (see graph) but has beaten the market by 4% over the last 12 months and 10% over the last three months.

Read More about Moss Bros on Stockopedia

Discuss Moss Bros on Stockopedia