Yahoo Finance

Yahoo Finance With Sustained Growth and More Buybacks, Accenture (NYSE:ACN) is Keeping Up the Strong Performance

The price of Accenture plc (NYSE:ACN) stock is up an impressive 182% over the last five years. On top of that, the share price is up 16% in about a quarter. The recent report outlined healthy progress for investors. Accenture will continue with the current pace and also approved an additional share repurchase program of US$3b.

So let's investigate and see if the longer term performance of the company has been in line with the underlying business' progress.

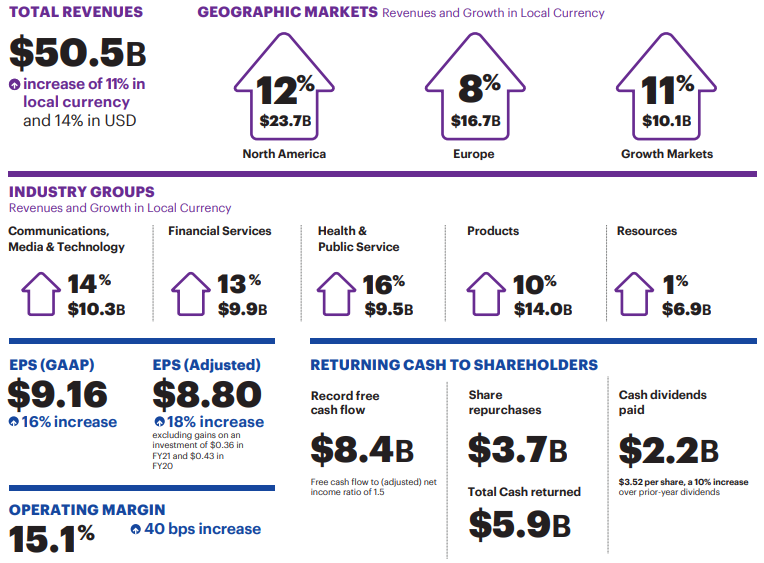

Accenture released its 4th quarter results and full year report. The company managed to meet growth expectations and delivered both on revenue and EPS estimates. The company grew revenues by 14% and EPS by 16%. Most of their growth comes both from North America & Emerging Markets.

View our latest analysis for Accenture

By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

Before the last results, during five years of share price growth, Accenture achieved compound earnings per share (EPS) growth of 8.5% per year. This EPS growth is lower than the 23% average annual increase in the share price. So it's fair to assume the market has a higher opinion of the business than it did five years ago. And that's hardly shocking given the track record of growth.

We know that Accenture has improved its bottom line lately, but is it going to grow revenue? Check if analysts think Accenture will grow revenue in the future.

Not All Earnings Are Equal

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time.

The ratio shows us how much a company's profit exceeds its FCF.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking. A negative accrual ratio is sometimes seen as a leading indicator to a better financial performance in the future.

Over the twelve months to May 2021, Accenture recorded an accrual ratio of -0.34.

That implies it has very good cash conversion, and that its earnings in the last year actually significantly understate its free cash flow.

Accenture produced free cash flow of US$8.4b ending with the fourth quarter, dwarfing its reported profit of US$5.9b. Accenture's free cash flow improved over the last year, which is generally good to see.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

What About Dividends?

When looking at investment returns, it is important to consider the difference between total shareholder return (TSR) and share price return. Whereas the share price return only reflects the change in the share price, the TSR includes the value of dividends (assuming they were reinvested) and the benefit of any discounted capital raising or spin-off. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. We note that for Accenture the TSR over the last 5 years was 207%, which is better than the share price return mentioned above. The dividends paid by the company have thus boosted the total shareholder return.

Key Takeaways

It's good to see that Accenture has rewarded shareholders with a total shareholder return of 62% in the last twelve months. The leadership is continuing with their share repurchase program and added US$3b in the program.

The one-year Total Stock Return is better than the five-year TSR (the latter coming in at 25% per year), it would seem that the stock's performance has improved in recent times. In the best case scenario, this may hint at some real business momentum, implying that now could be a great time to delve deeper.

Of course Accenture may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com