Yahoo Finance

Yahoo Finance Targa (TRGP) Stock Leaves No Mark Missing on Q2 Earnings

Shares of Targa Resources Corp. TRGP have seen no significant change since the firm’s second-quarter 2021 earnings release on Aug 5.

Despite the company’s raised adjusted EBITDA guidance for 2021 owing to anexcellent business performance and a more optimistic commodity pricing outlook for the rest of the year, the stock failed to display an uptrend.

Behind the Earnings Headlines

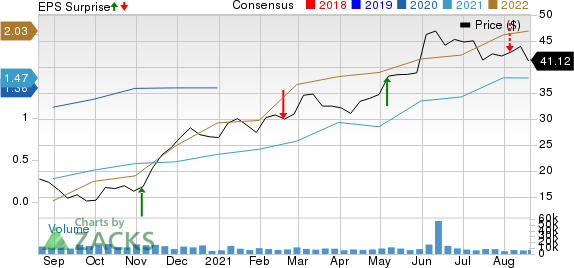

The company reported second-quarter 2021 adjusted net income per share of 15 cents, falling short of the Zacks Consensus Estimate of 29 cents and decreasing 28.6% year over year due to increased operating expenses as a consequence of greater repairs and maintenance costs, higher system throughput expenditures, and a rise in labor and material costs.

Adjusted EBITDA rose from $351.2 million a year earlier to $460 million in the second quarter of 2021.

Total revenues of $3.42 billion were 124.1% higher than the year-ago quarter’s level and also outpaced the Zacks Consensus Estimate of $3.36 billion.

Operational Performance

The Gathering and Processing segment recorded an operating margin of $301.2 million during the quarter, up 27% from $237.2 million achieved in the year-ago period. Moreover, Permian Basin volumes expanded year over year to 2,765.9 million cubic feet per day.

In the Logistics and Transportation (or the Downstream) segment, the company reported an operating margin of $291.4 million, up 26% year over year. Targa Resources saw a pipeline throughput rise from 256.1 thousand barrels per day (mbpd) to 391.7 mbpd, soaring 53% year over year. Export volumes grew 34% year over year while natural gas liquids sale surged 30% year over year.

Targa Resources, Inc. Price, Consensus and EPS Surprise

Targa Resources, Inc. price-consensus-eps-surprise-chart | Targa Resources, Inc. Quote

DCF, Capex & Balance Sheet

Second-quarter 2021 distributable cash flow (DCF) was $339.5 million, 24% above $273.7 million in the year-ago period. Targa Resources paid out a dividend of 10 cents per share.

As of Jun 30, 2020, the company had $209 million in cash and cash equivalents and $6.6 billion of long-term debt. Debt-to-capitalization was 53.2%.

Guidance

For 2021, Targa Resources reiterates its growth-driving capital spending guidance in the $350-$450 million range. Full-year maintenance capex is projected to be around $120 million.

With the energy player’s excellent business performance as well as a more bullish commodity pricing estimate for the remaining year, it lifts its 2021 adjusted EBITDA view to the $1.9-$2 billion band.

Zacks Rank & Key Picks

Targa Resources currently carries a Zacks Rank #3 (Hold). Some better-ranked players in the energy space are Matador Resources Co. MTDR, Devon Energy Corp. DVN and Continental Resources, Inc. CLR, each presently flaunting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Devon Energy Corporation (DVN) : Free Stock Analysis Report

Continental Resources, Inc. (CLR) : Free Stock Analysis Report

Matador Resources Company (MTDR) : Free Stock Analysis Report

Targa Resources, Inc. (TRGP) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research