Yahoo Finance

Yahoo Finance Is Taylor Wimpey (LON:TW.) A Risky Investment?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk'. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Taylor Wimpey plc (LON:TW.) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Taylor Wimpey

What Is Taylor Wimpey's Debt?

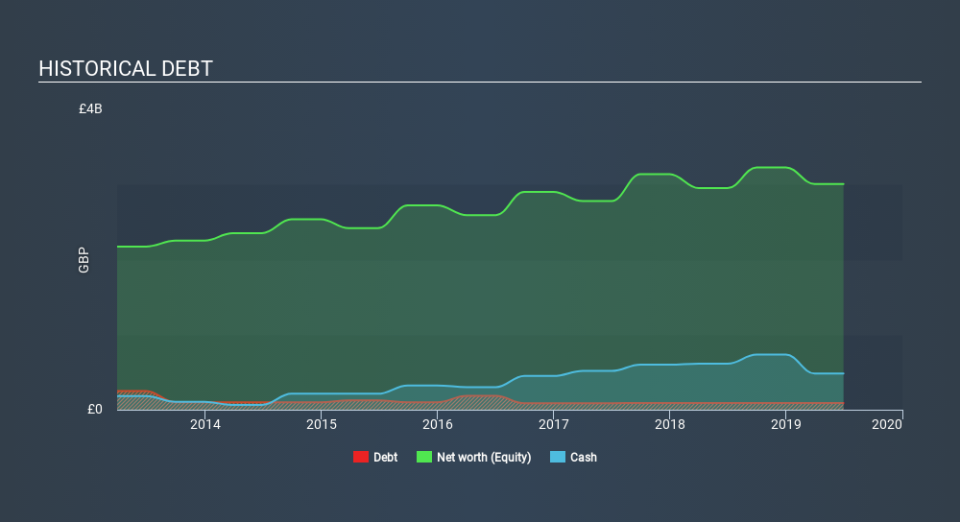

The chart below, which you can click on for greater detail, shows that Taylor Wimpey had UK£89.3m in debt in June 2019; about the same as the year before. However, its balance sheet shows it holds UK£481.3m in cash, so it actually has UK£392.0m net cash.

How Healthy Is Taylor Wimpey's Balance Sheet?

According to the last reported balance sheet, Taylor Wimpey had liabilities of UK£1.52b due within 12 months, and liabilities of UK£763.4m due beyond 12 months. On the other hand, it had cash of UK£481.3m and UK£188.5m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by UK£1.61b.

Taylor Wimpey has a market capitalization of UK£7.11b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. Despite its noteworthy liabilities, Taylor Wimpey boasts net cash, so it's fair to say it does not have a heavy debt load!

Taylor Wimpey's EBIT was pretty flat over the last year, but that shouldn't be an issue given the it doesn't have a lot of debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Taylor Wimpey's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Taylor Wimpey has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the most recent three years, Taylor Wimpey recorded free cash flow worth 69% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

While Taylor Wimpey does have more liabilities than liquid assets, it also has net cash of UK£392.0m. And it impressed us with free cash flow of UK£415m, being 69% of its EBIT. So we are not troubled with Taylor Wimpey's debt use. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Take risks, for example - Taylor Wimpey has 1 warning sign we think you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.