Yahoo Finance

Yahoo Finance How to Tell If You're Ready to Retire

Despite what it may seem like after seeing the news or spending a few minutes on your favorite social media site, we live in amazing times. This is especially true for many Americans who are approaching retirement age, who will live longer, more active lives than any prior generation.

Unfortunately, far too many individuals won't retire at the best time. That decision could have major repercussions on the quality of their lives and can impact family members who may have to care for and support them later in life, while also affecting society by putting more pressure on government resources to bridge the gap for the most at-risk of our seniors.

Image source: Getty Images.

So before you retire, it's worth taking the time to ask yourself a few key questions. Not only could this uncover a potential hole in your retirement plans, but it could give you a chance to make changes and get back on track.

Do you know how much income you'll really have in retirement?

If you're like many Americans, your retirement savings are probably worth a lot less in spending power than you realize. According to various sources, the average American around 65 has less than $200,000 in their 401(k) or IRA accounts. If that's your situation, let's take a step back and look at what $200,000 is worth in sustainable income.

Image source: Getty Images.

According to the 4% rule (where you withdraw 4% of your retirement savings in year one and then increase that based on inflation each year thereafter), $200,000 in retirement savings would only produce $8,000 the first year. If we combine that with the average $16,320 that Social Security says it pays the average retiree, that's barely over $20,000 per year from two of the most important sources of retirement income for the average American worker.

So what if you take out more than 5% per year from your retirement savings? If you're only counting on $16,000 per year from Social Security and don't have a pension to count on -- 90% of us don't -- then you'll almost certainly have to take out bigger distributions.

The risk in that case is outliving your retirement savings. The average American man who reaches 65 will live past 80, while the average American woman will live even longer.

Do you know much income you'll really need?

It costs most people less money to make ends meet in retirement. After all, you'll probably spend less money eating out for lunch and buy less gas for the daily commute, among other things. Many retirees also choose to downsize their homes, which can lead to lower energy costs, a smaller insurance bill, and less property taxes, too.

Image source: Getty Images.

On the other hand, you probably don't want to putter around the house all day, either. And if you're not careful, you'll end up taking on a hobby that costs a lot more than you expected. Just ask anyone who bought a boat after they retired....

The point is, don't just assume you're going to spend a lot less money after you retire. Take the time to put together a real-world budget and include more than just the bare necessities. Budget for travel, gifts for the grandkids, and all of the little things you only do a few times per year that inevitably get left out of the budget.

When you're on a fixed income, these unplanned expenses can start taking a big bite out of your retirement savings and force you to go back to work. The worst case scenario is that you could use up your retirement savings years before you're done living -- potentially when you're no longer physically able to work.

Have you considered how retiring now could impact your spouse?

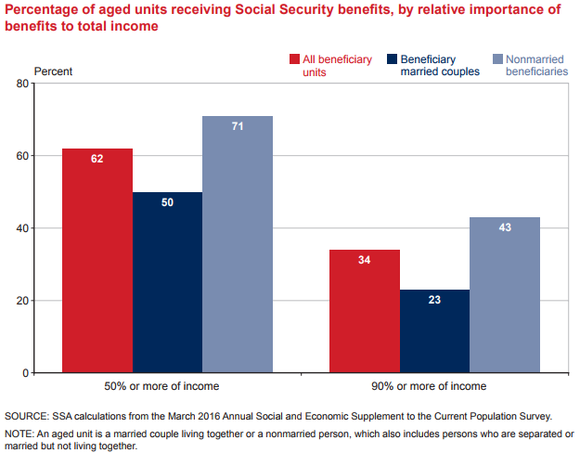

According to the Social Security Administration, half of married couples count on Social Security for at least half of their income. The numbers are even higher for non-married recipients:

Image source: Social Security Administration.

A significant portion of non-married retirees are widows and widowers, many of whom saw their household income fall sharply when their spouse died.

When one spouse dies, the surviving spouse will be able to continue receiving an amount equal to either their Social Security benefit or their spouse's if it was higher -- but not both. Many pensions work the same way, with surviving spouses often getting a reduced -- or even no -- benefit.

This means many people will see their household income fall more than their cost of living does when their spouse dies. If retiring today would potentially put your spouse in dire financial straits if they outlive you by a substantial number of years, you might not be ready to retire.

Have you considered what you'll do when you retire?

Daily golf with the occasional fishing trip sprinkled in may sound great, but many retirees find themselves with far more hours of idle time than they expected to have. For many retirees, the freedom and idle time they looked forward to before retiring actually become a problem.

Image source: Getty Images.

Retirees are far more likely to suffer depression than younger Americans. Far too many retirees lose their social connections and sense of purpose, and find themselves with hours of isolated idle time on their hands after they retire.

In addition to the emotional consequences, there are potential financial ones. Too many retirees fill their free time with shopping, gambling, or other expensive activities that can quickly wipe out retirement savings.

Answer these questions, then retire when you're really ready

Once you've answered these questions, you'll be empowered to retire on your own terms. You may have to make more than one adjustment to your original retirement plan. This might be working a little longer to make sure you're financially ready. It could mean working part time for a few years, too (something that would have social benefits, as well as extra money). You may also enjoy finding organizations to volunteer for that could benefit from your skills or simply your time, if you don't need to earn any income but find yourself with a lot of free time on your hands.

But even if it means a slightly different version of the retirement you originally expected, it will almost certainly be better than the one you could have ended up having if you had ignored these critically important questions and retired before you were really ready.

More From The Motley Fool

NVIDIA Scores 2 Drone Wins -- Including the AI for an E-Commerce Giant's Delivery Drones

Why You're Smart to Buy Shopify Inc. (US) -- Despite Citron's Report

6 Years Later, 6 Charts That Show How Far Apple, Inc. Has Come Since Steve Jobs' Passing

The Motley Fool has a disclosure policy.