Yahoo Finance

Yahoo Finance There's A Lot To Like About Thomson Reuters' (TSE:TRI) Upcoming US$0.54 Dividend

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Thomson Reuters Corporation (TSE:TRI) is about to go ex-dividend in just three days. The ex-dividend date is one business day before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. Accordingly, Thomson Reuters investors that purchase the stock on or after the 15th of May will not receive the dividend, which will be paid on the 10th of June.

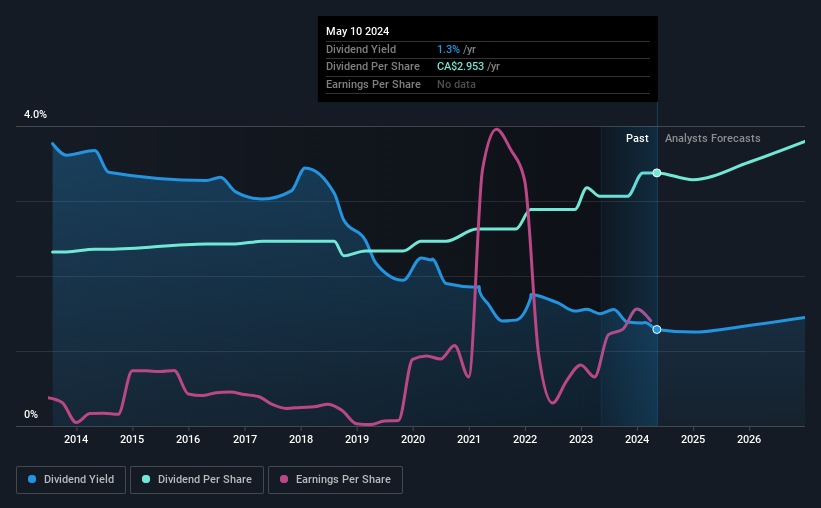

The company's next dividend payment will be US$0.54 per share, on the back of last year when the company paid a total of US$2.16 to shareholders. Based on the last year's worth of payments, Thomson Reuters has a trailing yield of 1.3% on the current stock price of CA$229.48. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to check whether the dividend payments are covered, and if earnings are growing.

See our latest analysis for Thomson Reuters

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Fortunately Thomson Reuters's payout ratio is modest, at just 39% of profit. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. It distributed 46% of its free cash flow as dividends, a comfortable payout level for most companies.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. That's why it's comforting to see Thomson Reuters's earnings have been skyrocketing, up 117% per annum for the past five years. Earnings per share have been growing very quickly, and the company is paying out a relatively low percentage of its profit and cash flow. This is a very favourable combination that can often lead to the dividend multiplying over the long term, if earnings grow and the company pays out a higher percentage of its earnings.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Thomson Reuters has delivered an average of 3.8% per year annual increase in its dividend, based on the past 10 years of dividend payments. Earnings per share have been growing much quicker than dividends, potentially because Thomson Reuters is keeping back more of its profits to grow the business.

To Sum It Up

From a dividend perspective, should investors buy or avoid Thomson Reuters? Thomson Reuters has grown its earnings per share while simultaneously reinvesting in the business. Unfortunately it's cut the dividend at least once in the past 10 years, but the conservative payout ratio makes the current dividend look sustainable. Overall we think this is an attractive combination and worthy of further research.

So while Thomson Reuters looks good from a dividend perspective, it's always worthwhile being up to date with the risks involved in this stock. To that end, you should learn about the 2 warning signs we've spotted with Thomson Reuters (including 1 which is a bit concerning).

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.