Yahoo Finance

Yahoo Finance We Think H C Slingsby (LON:SLNG) Is Taking Some Risk With Its Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that H C Slingsby plc (LON:SLNG) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for H C Slingsby

What Is H C Slingsby's Debt?

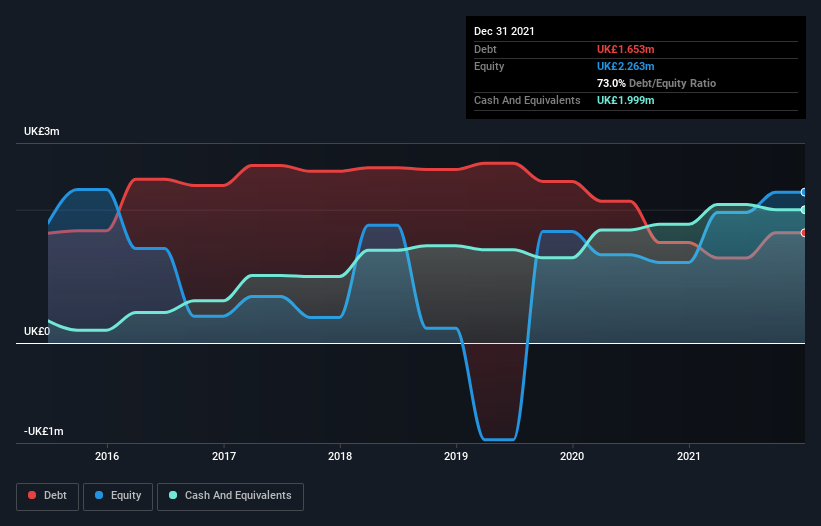

The image below, which you can click on for greater detail, shows that at December 2021 H C Slingsby had debt of UK£1.65m, up from UK£1.51m in one year. However, it does have UK£2.00m in cash offsetting this, leading to net cash of UK£346.0k.

A Look At H C Slingsby's Liabilities

Zooming in on the latest balance sheet data, we can see that H C Slingsby had liabilities of UK£4.63m due within 12 months and liabilities of UK£8.66m due beyond that. Offsetting this, it had UK£2.00m in cash and UK£2.40m in receivables that were due within 12 months. So it has liabilities totalling UK£8.88m more than its cash and near-term receivables, combined.

This deficit casts a shadow over the UK£2.42m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, H C Slingsby would likely require a major re-capitalisation if it had to pay its creditors today. H C Slingsby boasts net cash, so it's fair to say it does not have a heavy debt load, even if it does have very significant liabilities, in total.

It is just as well that H C Slingsby's load is not too heavy, because its EBIT was down 74% over the last year. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. When analysing debt levels, the balance sheet is the obvious place to start. But it is H C Slingsby's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. H C Slingsby may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, H C Slingsby recorded free cash flow worth a fulsome 93% of its EBIT, which is stronger than we'd usually expect. That puts it in a very strong position to pay down debt.

Summing up

While H C Slingsby does have more liabilities than liquid assets, it also has net cash of UK£346.0k. And it impressed us with free cash flow of UK£79k, being 93% of its EBIT. Despite the cash, we do find H C Slingsby's level of total liabilities concerning, so we're not particularly comfortable with the stock. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 3 warning signs for H C Slingsby (2 can't be ignored) you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.