Yahoo Finance

Yahoo Finance We Think Transurban Group (ASX:TCL) Is Taking Some Risk With Its Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Transurban Group (ASX:TCL) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Transurban Group

How Much Debt Does Transurban Group Carry?

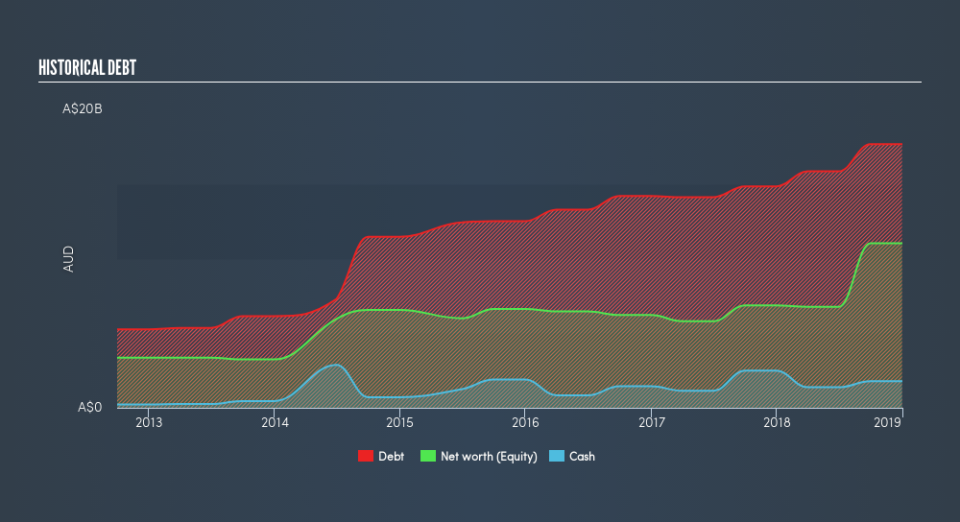

You can click the graphic below for the historical numbers, but it shows that as of December 2018 Transurban Group had AU$17.7b of debt, an increase on AU$14.8b, over one year. On the flip side, it has AU$1.78b in cash leading to net debt of about AU$15.9b.

How Healthy Is Transurban Group's Balance Sheet?

According to the last reported balance sheet, Transurban Group had liabilities of AU$3.26b due within 12 months, and liabilities of AU$18.9b due beyond 12 months. Offsetting this, it had AU$1.78b in cash and AU$362.0m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by AU$20.0b.

Transurban Group has a very large market capitalization of AU$41.6b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Weak interest cover of 1.5 times and a disturbingly high net debt to EBITDA ratio of 8.8 hit our confidence in Transurban Group like a one-two punch to the gut. This means we'd consider it to have a heavy debt load. Notably, Transurban Group's EBIT was pretty flat over the last year, which isn't ideal given the debt load. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Transurban Group can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Considering the last three years, Transurban Group actually recorded a cash outflow, overall. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

To be frank both Transurban Group's interest cover and its track record of managing its debt, based on its EBITDA, make us rather uncomfortable with its debt levels. But at least its EBIT growth rate is not so bad. It's also worth noting that Transurban Group is in the Infrastructure industry, which is often considered to be quite defensive. Looking at the bigger picture, it seems clear to us that Transurban Group's use of debt is creating risks for the company. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. Given our hesitation about the stock, it would be good to know if Transurban Group insiders have sold any shares recently. You click here to find out if insiders have sold recently.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.