Yahoo Finance

Yahoo Finance Thor Industries (THO): Climbing a Wall of Worry

Thor Industries Inc. (NYSE:THO) is a leading RV manufacturer in North America. It also has a significant market share in Europe. I'm bullish on the stock because I believe its earnings are bottoming and that the stock is climbing a wall of worry. Earnings should rebound in 2025, a significant catalyst that could boost its undervalued shares.

The company operates in what Stanley Druckenmiller (Trades, Portfolio) would call a "leading industry" and should be monitored by all investors - its results point to a rebound in Europe and a coming recession in North America.

The track record

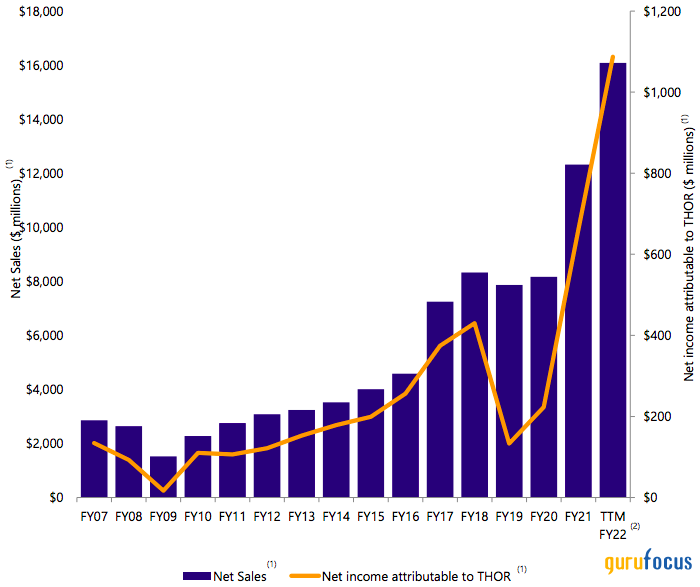

Thor's track record speaks for itself. The company has grown tremendously by making smart acquisitions at accretive prices, benefiting from the adoption of recreational vehicles and using its huge market share and pricing power to offset inflation.

Of course, the RV business is very cyclical; there was a major downturn in 2009 and 2020, but Thor managed to report a profit each time. The company was certainly over-earning in 2021 and 2022, but earnings have since dropped to $272 million ($5.05 diluted per share) on a trailing 12-month basis. Thor expects continued weakness into 2024, guiding toward $5 to $5.50 in diluted earnings per share. The company also expects capital expenditures to remain below depreciation and amortization at $180 million.

Thor's gotten bigger and bigger over the years. The company's market share for travel trailers and motorhomes in North America is 42% and 49%, respectively. This gives Thor an economies of scale position in the United States and Canada, where it primarily competes with Winnebago (NYSE:WGO) and Forest Rivers. The company also made a huge acquisition in Europe in 2019 and now has a 20% market share there. Here is Thor's history of acquisitions:

Thor has acquired a bunch of parts manufacturers over the years, making it a more integrated business.

Second-quarter takeaways

I have owned Thor shares on and off since early 2022. For some time now, I have expected a rebound in the company's European business, as well as a decline in the North American business. Europe's economy struggled in 2022 as the Russia-Ukraine war caused energy prices to spike and consumer confidence to plummet. Meanwhile, the U.S. economy was running hot.

In Thor's second quarter, my expectations for a reversal finally proved correct. North American sales are falling, but the company's European business is now beginning to shine. European sales were up 21% year over year. Its newfound geographic diversification is beginning to prove useful, with sales from Europe making up 38% of the company's second-quarter revenue.

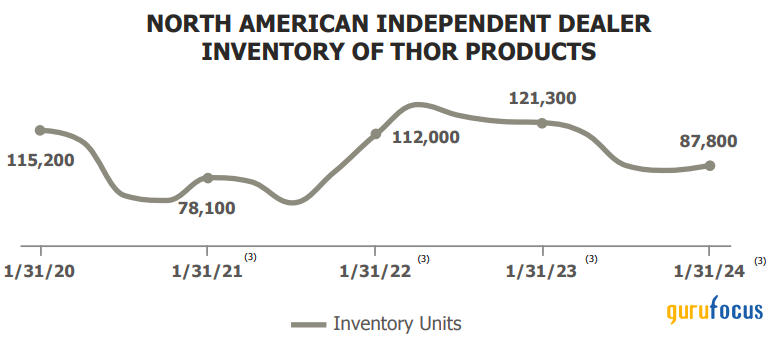

Customer inventories in North America have fallen, which, more often than not, signals we are near the bottom of the cycle:

What's also telling is that, in 2023, RV industry shipments saw their largest year-over-year drop since 2008, according to RV Industry Association. Should North American sales rebound in 2025 or 2026, Thor's optically cheap shares could trade higher. I think this is an important catalyst for the stock.

I also want to point out an important trend I have noticed in the North American towables business. For a long time now, RV prices have been sky-high in North America, a trend that seemed unstainable with interest rates increasing rapidly. It turns out, these prices were unstainable, but Thor is positioned well for a shift to cheaper travel trailers. The company said:

Overall net price per [towable] unit decreased 22.1% primarily due to the combined impact of a shift in product mix toward travel trailers and more moderately-priced units ~ [Meanwhile], unit shipments increased 10.2% primarily due to heightened demand for lower-cost travel trailer units.

With elevated interest rates and high energy prices, consumers may continue to gravitate toward Thor's affordable travel trailers. This has the potential to set the company apart from its competitors.

Normalized earnings valuation

Because of booms and busts in the economy, we have to look at Thor's average return on assets and profit margins to determine its normalized earnings. The company has averaged a 9.16% return on assets and a 4.75% net profit margin over the past 10 years. If we apply this to the company's $7.23 billion in assets and four-year average revenue of $11.98 billion, we get normalized earnings figures of $662 million and $569 million, for an average of $616 million ($11.55 per share). This gives Thor Industries a normalized price-earnings ratio of 8.60.

In recent years, Thor has started to buy back shares. These share buybacks, along with acquisitions and increased RV adoption, should bolster the company's growth. I think the world's RV market has a lot of room to run. RV's are primarily used in rich, developed economies. But, as countries like China, India, Mexico and Brazil grow wealthier, there should be even more opportunities for expansion. Given Thor's economies of scale position and long-term opportunity, I think the company could grow its normalized earnings at a mid-single-digit compound annual rate in the decade ahead.

Risks

Thor has a pretty strong balance sheet with a good current ratio (1.75) and manageable debt position. So I am not too worried about preservation of capital at a valuation of 1.30 times book. However, investors should monitor this over the years, especially if the company should make some big acquisitions using debt.

I also think there is a chance Thor could have to spend a substantial amount of investment capital to transition its motorhome business in an era of electric vehicles and autonomous driving technology (the towables business should not be affected much). This could be expensive, but Thor generates ample cash to do it.

Lastly, Thor probably will not live up to its 2027 earnings guidance of $27 per share, which is far too aggressive, in my opinion. Achieving this would be a heroic feat, given the company is currently earning just $5.10 per share, and our normalized earnings estimate is just $11.55 per share.

Summary

Thor's business has more geographic diversification than ever before, with more than a third of its second-quarter sales coming from Europe. Despite the downturn in North America, I see Thor as being well-positioned as consumers transition to more affordable travel trailers. The company's normalized earnings appear to be about $11.55 per share, with all signs pointing to an earnings trough in 2024. Thor is an aggressive competitor with an economies of scale position. I think the earnings guidance of $27 per share in 2027 is far too aggressive, but the company's shares still look very attractive at these levels.

This article first appeared on GuruFocus.