Yahoo Finance

Yahoo Finance Tutor Perini Corporation (NYSE:TPC) Analysts Are Reducing Their Forecasts For This Year

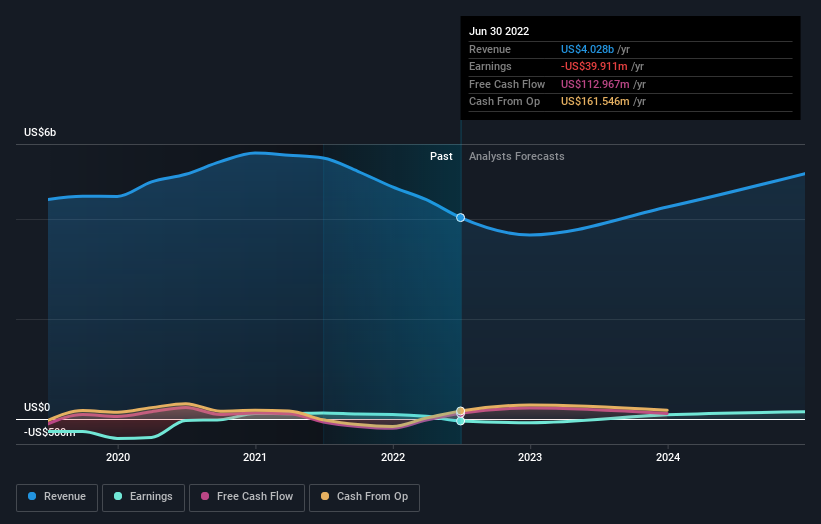

One thing we could say about the analysts on Tutor Perini Corporation (NYSE:TPC) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting analysts have soured majorly on the business.

Following the latest downgrade, the current consensus, from the three analysts covering Tutor Perini, is for revenues of US$3.7b in 2022, which would reflect an uncomfortable 8.7% reduction in Tutor Perini's sales over the past 12 months. Losses are supposed to balloon 87% to US$1.46 per share. Previously, the analysts had been modelling revenues of US$4.4b and earnings per share (EPS) of US$1.13 in 2022. So we can see that the consensus has become notably more bearish on Tutor Perini's outlook with these numbers, making a substantial drop in this year's revenue estimates. Furthermore, they expect the business to be loss-making this year, compared to their previous forecasts of a profit.

View our latest analysis for Tutor Perini

The consensus price target fell 13% to US$11.33, with the analysts clearly concerned about the company following the weaker revenue and earnings outlook. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on Tutor Perini, with the most bullish analyst valuing it at US$14.00 and the most bearish at US$9.00 per share. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Tutor Perini's past performance and to peers in the same industry. We would highlight that sales are expected to reverse, with a forecast 17% annualised revenue decline to the end of 2022. That is a notable change from historical growth of 0.4% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 6.7% per year. It's pretty clear that Tutor Perini's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest low-light for us was that the forecasts for Tutor Perini dropped from profits to a loss this year. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that Tutor Perini's revenues are expected to grow slower than the wider market. After such a stark change in sentiment from analysts, we'd understand if readers now felt a bit wary of Tutor Perini.

That said, the analysts might have good reason to be negative on Tutor Perini, given recent substantial insider selling. Learn more, and discover the 1 other concern we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here