Yahoo Finance

Yahoo Finance

United States Bus Market Report 2022-2030 Featuring Key Players - REV, Daimler, Navistar, The Lion Electric Co, Volvo, Blue Bird, GILLIG, NFI, GreenPower Motor Co, and BYD

U.S. Bus Market

Dublin, Aug. 31, 2022 (GLOBE NEWSWIRE) -- The "U.S. Bus Market Report: By Vehicle Type, Body Type, Ownership, Propulsion, Length, Seating Capacity - Industry Revenue Estimation and Demand Forecast to 2030" report has been added to ResearchAndMarkets.com's offering.

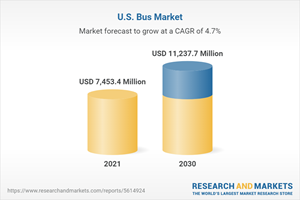

The U.S. bus market was worth $7,453.4 million in 2021, which is projected to reach $11,237.7 million by 2030, rising at a 4.7% CAGR from 2021 to 2030

This can be credited to the rising urbanization rate, growing population, as well as the increasing government investment in public transportation upgrades. Furthermore, the significant demand for school buses promotes the market expansion in the country.

Collaborations, partnerships, product debuts, and contract wins have all been used by the players in the U.S. bus market to obtain a competitive advantage. REV Group Inc., Daimler Truck AG, Navistar International Corporation, The Lion Electric Company, AB Volvo, Blue Bird Corporation, GILLIG LLC, NFI Group Inc., GreenPower Motor Company Inc., and BYD Company Limited are the key market players.

Standard buses had the bigger revenue share in 2021, and the category is expected to continue to dominate the U.S. bus market in the coming years. This will be due to the widespread usage of standard buses in public transit and school fleets. Furthermore, schools do not allow customized vehicles, which increases the demand for standard buses.

The usage of public transportation has the potential to enhance traffic safety, personal health, accessibility, and air quality. In comparison to private vehicles, public transportation consumes less fuel and emits less volatile organic compounds, carbon dioxide, and carbon monoxide per passenger mile. In addition to the environmental advantages, it has far lower crash severity rates than personal transport.

Key Findings of U.S. Bus Market Report

In 2021, the Californian bus market had the largest share in the U.S. Its large population has been increasingly demanding fast and efficient transportation networks. Furthermore, California is becoming a hotspot for innovative electric buses.

Based on seating capacity, buses with 30-50 seats had the biggest U.S. bus market revenue share, because they can transport more passengers, while using a lesser amount of fuel.

During 2021-2030, 8.1-10-meter buses are predicted to be the most popular. This bus model provides superior passenger comfort and mileage as compared to others.

In terms of revenue, the electric propulsion category is expected to advance at the highest rate throughout the forecast period. This is because the transport sector accounts for 27% of the GHG emissions in the U.S., which is why the government is now offering subsidies on EVs.

Robotic Research. RR.AI and GILLIG LLC started a partnership in January 2022 to create advanced driver assistance systems and level 4 autonomous vehicle technologies for transit buses in North America.

AB Volvo (Volvo Buses) introduced the new Volvo BZL Electric chassis in September 2021 to enhance its global electromobility offerings.

Key Topics Covered:

Chapter 1. Research Background

Chapter 2. Research Methodology

Chapter 3. Executive Summary

Chapter 4. Market Indicators

4.1 Growing Working Population

Chapter 5. Definition of Market Segments

5.1 By Vehicle Type

5.1.1 Inter-City Buses

5.1.2 Intra-City Buses

5.1.3 School Buses

5.1.4 Others

5.2 By Body Type

5.2.1 Standard

5.2.2 Customizable

5.3 By Ownership

5.3.1 Individual

5.3.2 Fleet

5.3.3 Government

5.4 By Propulsion

5.4.1 Diesel

5.4.2 Gasoline

5.4.3 CNG

5.4.4 Electric

5.4.5 Fuel Cell

5.4.6 Others

5.5 By Length

5.5.1 Below 6 m

5.5.2 6-8 m

5.5.3 8.1-10 m

5.5.4 10.1-12 m

5.5.5 Above 12 m

5.6 By Seating Capacity

5.6.1 Less than 30 Seats

5.6.2 30-50 Seats

5.6.3 More than 50 Seats

Chapter 6. Industry Outlook

6.1 Market Dynamics

6.1.1 Trends

6.1.1.1 Increasing government initiatives to adopt electric buses

6.1.1.2 Falling battery costs and improving operational efficiencies

6.1.2 Drivers

6.1.2.1 Advantages associated with public transportation

6.1.2.2 Availability of local, state, and federal funding

6.1.2.3 A large number of school buses

6.1.3 Impact Analysis of Drivers on Market Forecast

6.1.4 Restraints

6.1.4.1 Less convenient

6.1.4.2 Impact analysis of restraints on market forecast

6.1.5 Opportunities

6.1.5.1 Increasing replacement sales

6.2 Impact of COVID-19

6.3 Value Chain Analysis

6.4 Porter's Five Forces Analysis

Chapter 7. U.S. Bus Market Size and Forecast

7.1 Overview

7.2 Market Volume, by Vehicle Type (2017-2030)

7.3 Market Revenue, by Vehicle Type (2017-2030)

7.4 Market Volume, by Body Type (2017-2030)

7.5 Market Revenue, by Body Type (2017-2030)

7.6 Market Volume, by Ownership (2017-2030)

7.7 Market Revenue, by Ownership (2017-2030)

7.8 Market Volume, by Propulsion (2017-2030)

7.9 Market Revenue, by Propulsion (2017-2030)

7.10 Market Volume, by Length (2017-2030)

7.11 Market Revenue, by Length (2017-2030)

7.12 Market Volume, by Seating Capacity (2017-2030)

7.13 Market Revenue, by Seating Capacity (2017-2030)

7.14 Market Volume, by State (2017-2030)

7.15 Market Revenue, by State (2017-2030)

Chapter 8. Major Electric Bus Deployment Initiatives and Policy and Regulatory Landscape

8.1 Major Electric Bus Deployment Initiatives

8.2 Policy and Regulatory Landscape for Electric Buses

8.2.1 Overview

8.2.2 Incentive Schemes and Programs

8.2.2.1 Alabama

8.2.2.2 California

8.2.2.3 Colorado

8.2.2.4 Maryland

8.2.2.5 Massachusetts

8.2.2.6 Minnesota

8.2.2.7 Missouri

8.2.2.8 Nevada

8.2.2.9 New York

8.2.2.10 Ohio

8.2.2.11 Pennsylvania

8.2.2.12 Rhode Island

8.2.2.13 Texas

8.2.2.14 Utah

8.2.2.15 Virginia

8.2.2.16 Washington

Chapter 9. Competitive Landscape

9.1 Market Share Analysis of Key Players

9.1.1 U.S. Bus Market Share of Key Players (2021)

9.1.2 U.S. Electric Bus Market Share of Key Players (2021)

9.2 Product Benchmarking of Key Players

9.2.1 Electric Buses

9.3 Product Benchmarking of Key Players

9.3.1 Non-Electric Buses

9.4 Recent Strategic Developments of Player/Key Players

9.4.1 Client Wins

9.4.2 Partnerships & Collaborations

9.4.3 Geographic Expansions

9.4.4 Product Launches

Chapter 10. Company Profiles

10.1 Proterra Inc.

10.2 BYD Company Limited

10.3 New Flyer Industries (NFI) Group Inc.

10.4 GreenPower Motor Company Inc.

10.5 GILLIG LLC

10.6 Blue Bird Corporation

10.7 AB Volvo

10.8 The Lion Electric Company

10.9 Daimler Truck AG

10.10 REV Group Inc.

10.11 Navistar International Corporation

For more information about this report visit https://www.researchandmarkets.com/r/3xfmba

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood, Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900