Yahoo Finance

Yahoo Finance Vanguard Perspective: Hybrid Annuity TDFs and the Search for Income in Retirement

The search for better retirement income solutions has led to the emergence of target-date funds (TDFs) with an annuity component. Our researchOpens in a new tab finds that this innovative strategy shows investment merit for certain investors, said Roger Aliaga-Diaz, Ph.D., Vanguard's global head of portfolio construction and chief economist, Americas. But there are many potential challenges around suitability, complexity, and costs that need to be addressed in order to unlock its benefits.

How typical hybrid annuity TDFs work

While traditional target-date funds have become a tool that more than half of all 401(k) participants use to build their retirement savings, it's much harder to find broadly suitable products to help retirees turn their retirement savings into income, said Aliaga-Diaz.1

Hybrid annuity TDFs are designed to meet that need. In this type of fund, the allocation to a growth-focused multi-asset portfolio like that of a traditional TDF is decreased ahead of retirement to prefund the purchase of an annuity that is expected to provide a certain level of guaranteed income throughout retirement.2 (How much, if any, of the prefunding is used to buy an annuity is left to the discretion of the investor, for many product offerings in the marketplace.)

There are three types of fixed-rate annuities commonly used in hybrid annuity TDFs.3 These types differ by when the retiree would begin receiving income:

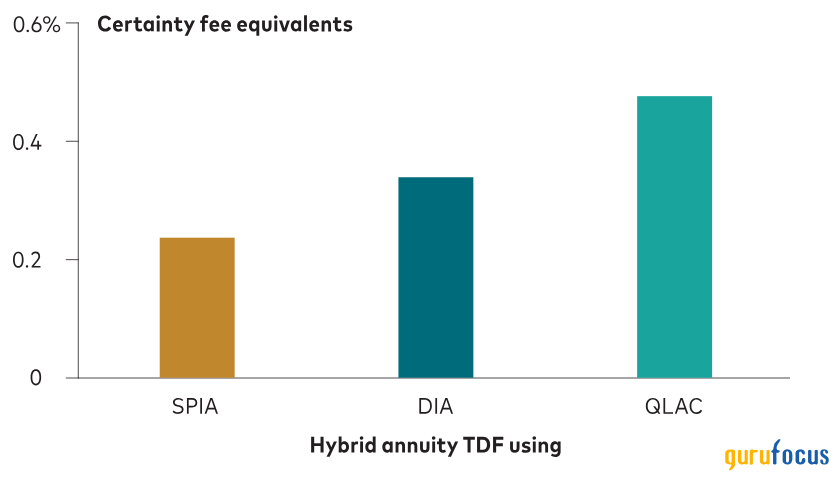

Single premium immediate annuity (SPIA): Starts providing income immediately after the annuity purchase.

Deferred income annuity (DIA): Starts providing income at a future date after the annuity purchase.

Qualified longevity annuity contract (QLAC): Starts providing income at a later stage of retirement (age 78-plus). This deferred annuity is exempt from required minimum distributions.

The investment merit of hybrid annuity TDFs

While Vanguard does not offer hybrid annuity TDFs, we have conducted extensive research into these products as part of our continuing efforts to lead the advancement of investment thinking and practice in the asset management industry.

In our evaluation of hybrid annuity TDFs, we used our proprietary Vanguard Life-Cycle Investing Model (VLCM)4 to quantify the additional benefits an investor could receive from blending annuities into traditional target-date funds, said Aliaga-Diaz. Using VLCM, we can measure the degree of improvement in an investor's ability to afford expected living standards throughout retirement, the reduction in the risk of outliving one's wealth, and mitigation of market risk when using a hybrid annuity TDF versus a traditional TDF.

The figure below shows the results of our evaluation, using a design close to some of the hybrid annuity TDFs available in the market. (Read more here about our research and the assumptions we used.)

The value offered to a participant depends on the design of the hybrid annuity TDF and is influenced by factors like timing and the amount and type of annuity used. Hybrid annuity TDFs provide higher investment value for retirees across all three types of annuities. The overall improvement in value to investorsmeasured by VLCM in terms of certainty-fee-equivalent (CFE)5 unitsranged from 0.24% for an SPIA to 0.48% for a QLAC.

Hybrid annuity TDFs show good investment value for certain investors

Notes: The income funding strategy start age is 55, while the maximum allocation to the income funding strategy is 25% and the share of the income funding strategy used for the annuity purchase is 100%. See the Hybrid annuity TDF assumptions and Life-cycle modeling inputs sections in the Appendix of our research for additional details.

Sources: Vanguard and CANNEX.

Some caveats to consider

Hybrid annuity TDFs are unlike traditional TDFs in that they are far less of a one-size-fits-all solution. Here are some of the hurdles in making this new solution accessible and beneficial for investors.

Suitability: As investors move from building to spending their retirement savings, their investment needs become more specific. That's due to individual factors such as health, family dependencies, a desire (or not) to leave a financial legacy, and risk preferences.

Complexity: Many hybrid annuity TDFs include an option to use none, some, or all of the annuity prefunding set aside for the purchase of an annuity. That puts the onus on the investor to determine the optimal purchase amount given their particular income needs (which will evolve over time), desire for liquidity, and tolerance for potentially outliving their savings.

Cost: Hybrid annuity TDFs tend to cost more than off-the-shelf TDFs. There are additional, often opaque, expenses associated with the annuity component that need to be considered.

The takeaway

Hybrid annuity TDFs have the potential to help retirees manage and spend what they've worked hard to save by blending the growth potential of traditional TDFs with the stability of annuities offering guaranteed income throughout retirement, said Aliaga-Diaz. While hybrid annuity TDFs show promise in providing a more secure retirement, they also introduce complexities and higher costs. Addressing these challenges through strategic planning and tailored solutions could make hybrid annuity TDFs a viable option for a broader range of investors, ultimately leading to more personalized and effective retirement outcomes.

1 How America Saves 2024

2 Product guarantees are subject to the claims-paying ability of the issuing insurance company.

3 Hybrid annuity TDF providers also use other insurance products like indexed or variable annuities.

4 The VLCM is a proprietary model for glide-path construction that can assist in the creation of custom investment portfolios for retirement as well as nonretirement goals. For a more detailed explanation, read Vanguard's Life-CycleOpens in a new tab Investing Model (VLCM): A general portfolio framework for goals-based investingOpens in a new tab

5 CFE can be thought of as the additional annual fee a participant would be willing to pay for an alternative asset allocation (e.g., a hybrid annuity TDF) relative to a reference asset allocation (e.g., a traditional TDF). A positive CFE indicates higher utility from the hybrid annuity TDF compared with the traditional TDF, while a negative CFE indicates lower utility.

Notes:

The Vanguard Life-Cycle Investing Model (VLCM) is designed to identify the product design that represents the best investment solution for a theoretical, representative investor who uses the target-date funds to accumulate wealth for retirement. The VLCM generates an optimal custom glide path for a participant population by assessing the trade-offs between the expected wealth accumulation and the uncertainty about that wealth outcome, for thousands of potential glide paths. The VLCM does this by combining two sets of inputs: the asset class return projections from the Vanguard Capital Markets Model (VCMM) and the average characteristics of the participant population. Along with the optimal custom glide path, the VLCM generates a wide range of portfolio metrics such as improvement in expected participant welfare as measured by certainty fee equivalent, distribution of potential wealth accumulation outcomes, risk and return distributions for the asset allocation, and probability of ruin, such as the odds of participants depleting their wealth by age 95.

The VLCM inherits the distributional forecasting framework of the VCMM and applies to it the calculation of wealth outcomes from any given portfolio.

The most impactful drivers of glide-path changes within the VLCM tend to be risk aversion, the presence of a defined benefit plan, retirement age, saving rate, and starting compensation. The VLCM chooses among glide paths by scoring them according to the Constant Relative Risk Aversion utility function and choosing the one with the highest score. The VLCM does not optimize the levels of spending and contribution rates. Rather, the VLCM optimizes the glide path for a given customizable level of spending, growth rate of contributions, and other participant and plan sponsor characteristics.

A full dynamic stochastic life-cycle model, including optimization of a savings strategy and dynamic spending in retirement, is beyond the scope of this framework.

All investing is subject to risk, including the possible loss of the money you invest.

Diversification does not ensure a profit or protect against a loss.

There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income.

Investments in target-date funds are subject to the risks of their underlying funds. The year in the fund name refers to the approximate year (the target date) when an investor in the fund would retire and leave the workforce. The fund will gradually shift its emphasis from more aggressive investments to more conservative ones based on its target date. An investment in target-date funds is not guaranteed at any time, including on or after the target date.

This article first appeared on GuruFocus.