Yahoo Finance

Yahoo Finance Vulcan (VMC) Rides on Public Sector Demand, Operational Plans

Vulcan Materials Company VMC is riding on robust public sector demand and strategic operational initiatives like strong pricing and fixed-cost leverage. Also, strategic acquisitions bode well for the company.

Recently, Vulcan reported impressive first-quarter 2023 results, with earnings and revenues beating the Zacks Consensus Estimate by 48.4% and 4.3%, respectively. Also, the top and bottom lines grew year over year by 7% and 30.1%, respectively. Focus on operating disciplines and strong pricing actions to overcome inflationary pressure resulted in growth.

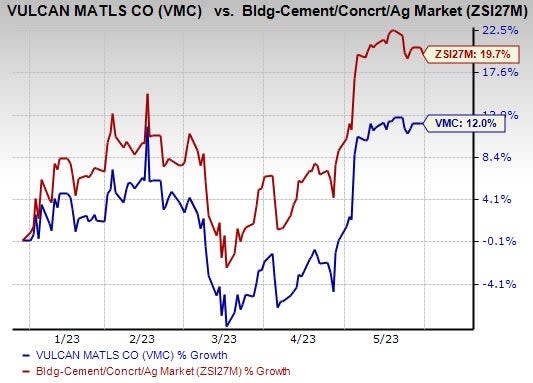

Shares of VMC have increased 12% in the year-to-date period compared with the Zacks Building Products - Concrete and Aggregates industry’s 19.7% growth. Although it has underperformed the industry, earnings estimates for 2023 have moved north to $6.45 per share from $5.87 in the past 30 days. This depicts analysts' optimism over the company’s prospects.

Image Source: Zacks Investment Research

VMC has a trailing four-quarter earnings surprise of 7.1%, on average. The Zacks Consensus Estimate for the company’s 2023 sales and earnings per share (EPS) indicates a rise of 5.9% and 26.2%, respectively, from the year-ago period’s levels.

Factors Favoring VMC

Vulcan has been witnessing strong pricing, underpinned by growing public demand (mainly transport) and operational discipline. Public sector construction includes spending by federal, state and local governments for the construction of highways, bridges, airports, dams, roads and other infrastructure construction.

During first-quarter 2023, the company noted that highway starts were more than $100 billion. Other infrastructure starts rose 23% in the trailing 12 months. In Texas, public sector lettings are expected to be almost $8 billion, an all-time high, in the first half of 2023. The company expects the current strength in private non-residential construction activity and increased public funding to offset residential market woes in the remainder of 2023.

VMC remains focused on creating long-term value by compounding unit margins through four strategic initiatives — Commercial Excellence, Operational Excellence, Strategic Sourcing and Logistics Innovation — that enhance price growth and operating efficiencies. Higher price realizations and its four strategic initiatives should continue to increase unit profitability.

The improvement in pricing, fixed cost leverage and operating efficiencies helped the company achieve 28% growth in unit profitability of the Aggregates segment and 15% improvement in adjusted EBITDA in first-quarter 2023. In the trailing 12 months period, adjusted EBITDA rose 11.2% despite persisting inflationary pressure.

Also, Vulcan have been following a systematic inorganic strategy for expansion and has wrapped up various bolt-on acquisitions that contributed significantly to its growth. Big or small acquisitions have been a key strategy for the company. In 2022, the company acquired five aggregates facilities in Texas, four ready-mixed concrete facilities and two idle ready-mixed concrete sites in Virginia, eight aggregates, four asphalt mix and seven ready-mixed concrete operations in California, and an aggregates operation serving limited markets along the Gulf Coast in Honduras for $594.6 million. In 2023, Vulcan expects to spend between $600 and $650 million on capital expenditures.

Zacks Rank & Other Key Picks

VMC currently carries a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Here are some other top-ranked stocks that investors may consider from the Zacks Construction sector.

Martin Marietta Materials, Inc. MLM currently sports a Zacks Rank #1. MLM delivered a trailing four-quarter earnings surprise of 31%, on average. Shares of the company have gained 17.9% in the year-to-date period.

The Zacks Consensus Estimate for MLM’s 2023 sales and EPS indicates growth of 19% and 32.1%, respectively, from the previous year’s reported levels.

Watsco, Inc. WSO currently sports a Zacks Rank #1. WSO delivered a trailing four-quarter earnings surprise of 5.3%, on average. Shares of the company have gained 32.7% in the year-to-date period.

The Zacks Consensus Estimate for WSO’s 2023 sales and EPS indicates growth of 3.1% and 2.1%, respectively, from the previous year’s reported levels.

Otis Worldwide Corporation OTIS currently carries a Zacks Rank #2 (Buy). OTIS has a trailing four-quarter earnings surprise of 5.9%, on average. Shares of the company have gained 3.8% in the year-to-date period.

The Zacks Consensus Estimate for OTIS’ 2023 sales and EPS indicates growth of 2.9% and 8.8%, respectively, from the previous year’s reported levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Watsco, Inc. (WSO) : Free Stock Analysis Report

Vulcan Materials Company (VMC) : Free Stock Analysis Report

Martin Marietta Materials, Inc. (MLM) : Free Stock Analysis Report

Otis Worldwide Corporation (OTIS) : Free Stock Analysis Report