Yahoo Finance

Yahoo Finance Is Weakness In Delignit AG (ETR:DLX) Stock A Sign That The Market Could be Wrong Given Its Strong Financial Prospects?

It is hard to get excited after looking at Delignit's (ETR:DLX) recent performance, when its stock has declined 14% over the past month. However, stock prices are usually driven by a company’s financial performance over the long term, which in this case looks quite promising. Particularly, we will be paying attention to Delignit's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Put another way, it reveals the company's success at turning shareholder investments into profits.

Check out our latest analysis for Delignit

How Is ROE Calculated?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Delignit is:

16% = €4.6m ÷ €29m (Based on the trailing twelve months to June 2023).

The 'return' refers to a company's earnings over the last year. So, this means that for every €1 of its shareholder's investments, the company generates a profit of €0.16.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Delignit's Earnings Growth And 16% ROE

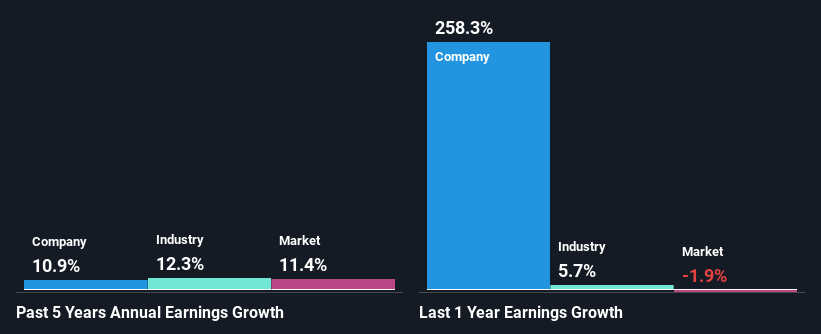

To start with, Delignit's ROE looks acceptable. Further, the company's ROE is similar to the industry average of 16%. This certainly adds some context to Delignit's moderate 11% net income growth seen over the past five years.

Next, on comparing Delignit's net income growth with the industry, we found that the company's reported growth is similar to the industry average growth rate of 12% over the last few years.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. If you're wondering about Delignit's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Delignit Efficiently Re-investing Its Profits?

In Delignit's case, its respectable earnings growth can probably be explained by its low three-year median payout ratio of 8.9% (or a retention ratio of 91%), which suggests that the company is investing most of its profits to grow its business.

Additionally, Delignit has paid dividends over a period of nine years which means that the company is pretty serious about sharing its profits with shareholders. Looking at the current analyst consensus data, we can see that the company's future payout ratio is expected to rise to 13% over the next three years. Consequently, the higher expected payout ratio explains the decline in the company's expected ROE (to 12%) over the same period.

Conclusion

In total, we are pretty happy with Delignit's performance. In particular, it's great to see that the company is investing heavily into its business and along with a high rate of return, that has resulted in a sizeable growth in its earnings. On studying current analyst estimates, we found that analysts expect the company to continue its recent growth streak. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.