Yahoo Finance

Yahoo Finance Why an 84-month auto loan is a clunker for your finances

Imagine buying a new car, getting the keys, signing a financing agreement — and then realizing you’ll still be making payments seven years later.

That's a real possibility, as more car dealerships and lenders offer 84-month auto loans.

A seven-year loan may seem like a great option; after all, a longer term means a smaller monthly payment.

But that doesn't make it a good idea. Here’s what you need to consider before getting an 84-month car loan.

More from MoneyWise:

A large percentage of Americans could be missing out on lower car insurance premiums

Invest like the 1% and get in on these 5 alternative investments that outperform the S&P

Popular microinvesting apps can build an income-generating investment portfolio for you

Why you might consider an 84-month car loan

The loans seem more affordable

For many years, the longest car loan most lenders would consider was 72 months, or six years.

Newer, 84-month loans tempt borrowers with even smaller payments over an even lengthier term.

This can seem very appealing if you have a limited budget and can't afford the payments on a shorter-term loan.

You'd have more money to invest

The smaller payments with an 84-month auto loan theoretically free up money you could put toward other uses.

The idea makes sense if you feel confident your investments will net you a higher return than the interest on the loan.

But don’t let the mere possibility fool you into choosing an 84-month car loan. If you don’t actually invest more, then you’re just suffering the downsides of a longer loan for no reason.

Disadvantages of an 84-month car loan

You'll pay a ton more in interest

Though an 84-month loan means a smaller payment every month, your total interest will be higher because you'll be paying interest longer.

And a seven-year loan typically comes with a higher interest rate than a shorter-term loan.

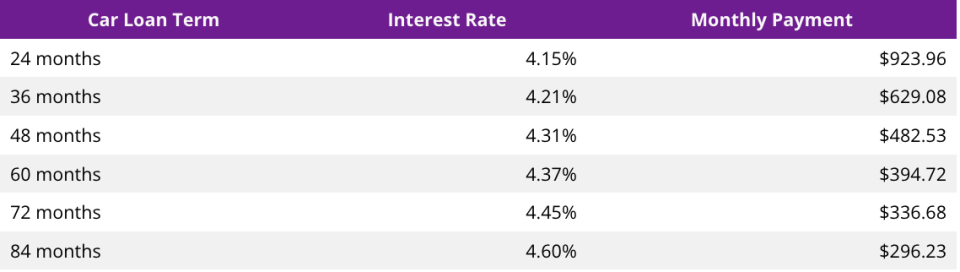

Let’s take a look at what your monthly payment might be on a $20,000 loan based on the length of your term, assuming you have an excellent credit score.

Now let’s see how much interest you’d pay in total for each of these terms.

As you can see, the monthly payment on a 60-month loan is about $100 more a month than the monthly payment on an 84-month loan, but you’d save $1,200 in interest over the course of your loan.

You could always try to pay back an 84-month loan sooner to cut down your total interest, but many lenders charge a prepayment fee for paying off your loan early, so it may not be worth it.

If you really need a seven-year loan to buy your dream vehicle, take that as a sign that it's well out of your price range.

You could find yourself upside-down on the loan

Unlike a house, vehicles almost never appreciate in value over time. So making a commitment to long-term financing is not a good idea.

New cars lose about 23.5% of their value after a year and about 60% after five years, according to the automotive site Edmunds.

Your car will likely depreciate faster than you can pay it off, leaving you upside-down on your loan. In other words, if you were to sell the car for market value before your 84-month loan term is up, you'd still owe some money to your lender.

And if you get into an accident before your car is fully paid off, your insurance provider may only cover the market price of the car, which will likely be less than what you owe.

Even if your car is totalled and no longer drivable, you could still be on the hook for your monthly payments until your loan is paid off.

You may get caught in a negative equity cycle

If you decide you want to trade in your car before your 84-month loan is paid off, you could get caught in what’s known as a negative equity cycle, in which you owe more every time you take out a new loan.

Let’s say you buy a $20,000 car on an 84-month financing plan at 4.6%, like in our example above, and your monthly payment is $296.23.

You drive it for four years, then you decide you want to trade it in for a new car that costs $25,000. Because you took out an 84-month loan, you still owe $10,664.28 on your trade-in.

However, your car has depreciated in value since you bought it and you’ve put a fair number of miles on the odometer, so your trade-in is only worth $8,000.

You now have $2,664.28 of negative equity, which means you’ll need to borrow $27,664.28 for your new car. With the same 84-month loan, your new monthly payment will be $409.53.

If you do the same thing with your subsequent cars and trade them in before your loan term ends, you’ll continue to accumulate negative equity and your debt will just keep growing.

Your warranty will expire first

A big selling point on new vehicles is the warranty that covers repairs in the early years.

However, most warranties don't last seven years, and as your loan ages, your vehicle will probably need repairs that are more involved and expensive.

That means you'll be paying for repairs out of your own pocket while you're still paying for your car.

And if you buy a used car, the odds that it will need serious repairs before the end of an 84-month loan are even higher.

For example, if you purchase a five-year-old car with an 84-month loan, it’ll be 12 years old by the time your loan is fully paid off.

Even if you spend a bundle on repairs, there’s a chance that your five-year-old car will eventually be undrivable before your 84-month loan term is up.

Alternatives to 84-month loans

There are several alternatives to taking out an 84-month loan that may be better a better option for you:

Look into refinancing

If you’ve already taken the plunge and locked in an 84-month loan, don’t panic.

As long as you have a decent credit score, you may be able to refinance your loan into a shorter term with a better rate.

Don’t buy, lease

If you’ve got your heart set on a car that’s out of your price range, your best bet may be to lease it instead of buying.

Leasing often requires a lower monthly payment, since payments are based on the car’s depreciation during the lease period instead of the sticker price.

And if you decide you still want the car when your lease is up, you’ll have the option to buy it at an amount stipulated in your contract.

Save up for a larger down payment

Instead of jumping into a lengthy loan right away, you could spend some time building up your savings — ideally in a high-yield account.

That way you’ll be able to make a larger down payment and take out a smaller loan with a lower monthly payment.

This article provides information only and should not be construed as advice. It is provided without warranty of any kind.