Yahoo Finance

Yahoo Finance Why there's 'no future for bond holders' as Venezuela staggers into default

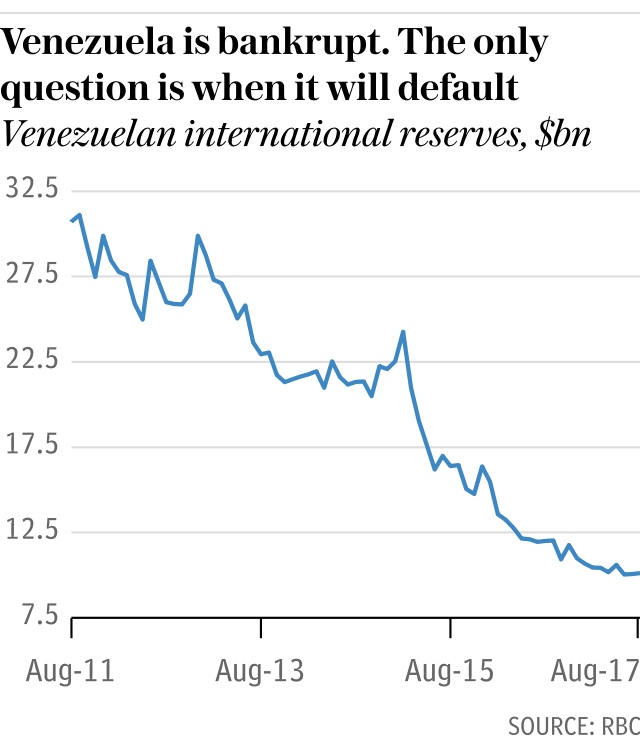

Venezuela, with its extraordinarily rich oil reserves, is now crippled by debt, and has started to default on bond pay-outs.

Maduro's spin on the situation is to claim that he is restructuring foreign debt; slowly renegotiating terms with Russia – so far, Venezuela's lender of last resort – and China.

A tweet from Delcy Rodriguez, a long term servant of the successive Chavez and inspired governments, reads that Venezuela has "initiated a successful refinancing of its debt. An imperial blockade will not tarnish Venezuela's financial prestige!"

Black, it seems, is white as far as the brutal regime goes. But not on the bond markets and not for ratings agencies: repayments of £200m have been missed, and credit ratings agency Standard and Poor's has declared the country to be in "selective default". It is joined in this verdict by fellow agencies Fitch and Moody's.

What does this mean for the holders of what have been described as "hunger bonds"? And, what might it mean for the starving people of what was once considered the shining economic jewel of Latin America?

Why won't the International Monetary Fund step in?

There are two main reasons why the IMF – the world's lender of last resort, which bailed out Greece and Ukraine among others in recent years – will not be stepping in to aid a Venezuelan default any time soon.

One is the US. Its sanctions regime against, and attitude towards the oppressive regime of President Nicolas Maduro, supposed heir to Hugo Chavez, is hostile.

The other is the sheer amount of money involved. Even if there were a regime change which was sufficient to satisfy the US's objections, the scale of the funds required to restructure the country's finances is vast.

IMF multi-year programmes are limited to 435pc of a country's quota (that's an amount it can access based on its relative position in the world economy). In practical terms that would mean $23bn over three to four years for Venezuela. It needs more like $32bn a year.

But Greece was allowed a special deal, why not Venezuela?

In order to get that level of funding Venezuela would need what is known as "exceptional access" to the IMF's cash. This was allowed in the case of Greece, but it was extremely controversial, and led by a desire to keep the Greece within the European Union, and save banks reliant on the euro currency.

Seven years on from the initial agreement for the IMF to release funds to Greece, handing over the final tranche of it at the turn of 2017 was hotly contested, with the US Congress calling for European institutions to solve the Greek debt-crisis on their own.

The idea that the same magnitude of allowance would be made, while any trace of the Chavista revolution (the socialist movement sanctioned against by the US for decades) remains in Venezuela, is highly unlikely. The US would simply veto any such move.

It's also worth noting that while speculation as to the scale of any Venezuelan bail-out is rife, it cut the last of its ties with the IMF in 2007, which means that attempts to gather intelligence as to the real state of its economy are seriously curtailed.

Who could lose money as a result of the default?

Bondholders who are owed $60bn. Which while it sounds obvious, some exposure to debt may have reached quite surprising places: most money has been moving on the secondary bond market – as the US stepped up sanctions against deals with the Maduro regime.

The largest institutional holders of Venezuelan debt are Fidelity Investment, $572m; T. Rowe Price, $370m; BlackRock iShares, $222m; Goldman Sachs, $187m; and Invesco Powershares at $113m, according to CNN.

Professor Ricardo Hausmann, a Harvard-based expert on the Venezuelan economy, told The Daily Telegraph that there was unlikely to be any change to the situation in the immediate future.

Observers need to comprehend the level to which the economy has imploded: "There is no economic plan," he explains. Oil production is declining sharply, and there is currently no value – with close to zero imports halting most production in the country – being created in the economy. That means there is no sort of exchange to be made with the country's debtors: "there is no future for bondholders [under the Maduro regime]," he says.

Nothing short of regime change and dramatic increase in imports in order to revive production can turn things around. Until then, Hausmann can see "no swift resolution".

Speaking last month, Casey Reckman, an emerging markets expert at Credit Suisse, noted that the Argentine restructuring process took roughly 15 years to be completed, if you include resolving the dispute with holdout creditors.

There is no future for bondholders under the Maduro regime

"In Venezuela you have the ICSID (International Centre for Settlement of Investment Disputes) claimants, the bond holders (Venezuela PDVSA – the state oil company bonds), commercial arrears of the government and with PDVSA’s suppliers as well as large bilateral loans from countries like China and Russia," she said.

In their latest meeting in Caracas with the authorities on Monday, rather than being given clarity on the likely terms of any repayment, over 100 bond holders including some from New York, were given a goody bag with state produced chocolates and coffee according to Reuters, but no clarity on repayments.

That sounds funny at first, but Venezuelan bonds are called "hunger bonds" for a reason. There are accounts of people breaking into zoos to kill animals, so desperate is their search for food. In 2016, three quarters of the population lost an average of 19 pounds in weight.

Even if regime change were to come to the suffering country, anything short of a complete rejection of Chavista ideology makes an IMF bailout unlikely.

When Argentina defaulted, Hugo Chavez attempted to step in, and lend it funds, rather than it being at the mercy of the IMF's stringent terms. He paid off debts to the World Bank ahead of schedule in 1999, and attempted to set up the Bank of the South, an alternative Latin American lender of last resort.

The scale of change needed in order for any kind of rebuilding of the Venezuelan economy, with clear and proper efforts to pay off creditors, is of an ideological and economic order that is hard to envisage coming to pass.