Why Britain’s state pension time bomb is about to explode

The last Baby Boomer turns 60 this year. Many born between 1946 and 1964 have already retired, and millions more will follow in the coming years, with the number of people reaching state pension age forecast to hit a record 800,000 in 2028 for the first time. By then the earliest anyone will be able to claim their state pension will be 67, up from 66 today.

Rising longevity meant that for decades, raising the state pension age was the silver bullet that helped to defuse Britain’s demographic time bomb. But not for much longer.

Until now, a rising age limit has kept the Baby Boomers working, boosting a jobs-rich recovery in the wake of the financial crisis and keeping the economy afloat.

It meant politicians could think of paying pensions as tomorrow’s problem – a long-term challenge of slow-moving demographics that could always be left to a future government.

But that time bomb is still ticking. And Britain’s falling birth rate and life expectancy means it’s about to explode amid this huge wave of retirement.

The Telegraph is examining the future of the state pension in a three-part series that will focus on the implications for work, retirement and living standards for different generations.

In this first instalment, we look at whether the Government can keep making the sums add up when the pensioner population is expected to rise from 12m today to 17m by 2070.

Trouble ahead

The working age population is expected to increase by just over 1m to 44m over that period.

Already, £1 in every £8 of government spending goes on the state pension. Fast forward 50 years, and that number will be more like £1 in every £6.

A wave of retiring boomers is expected to push up the pensions bill dramatically this decade. While raising the state pension age to 67 by 2028 will stem the rise in costs, the Office for Budget Responsibility (OBR) predicts overall spending on the state pension will be £23bn higher in 2027-28 than it was at the start of the 2020s. This jump is not happening within five decades, but five years.

Sir Charlie Bean, a former OBR official, says the world took a global peace dividend and era of cheap money for granted, spending extra money with abandon, which is now coming back to bite.

“If you go back about 50 years about a quarter of [state] spending was on health and welfare including pensions. That has risen to about half, essentially because of these demographic forces - ageing - and also the nature of technical change in the health sector,” he says, noting that medical innovations are often expensive.

“Three things have made room for it. Firstly, declines in public investment; secondly declines in defence spending [that came with] the cold war dividend; and thirdly a fall in contribution from debt interest.”

Suddenly those have reversed, with serious implications for spending in the next parliament at a time when money is already very tight.

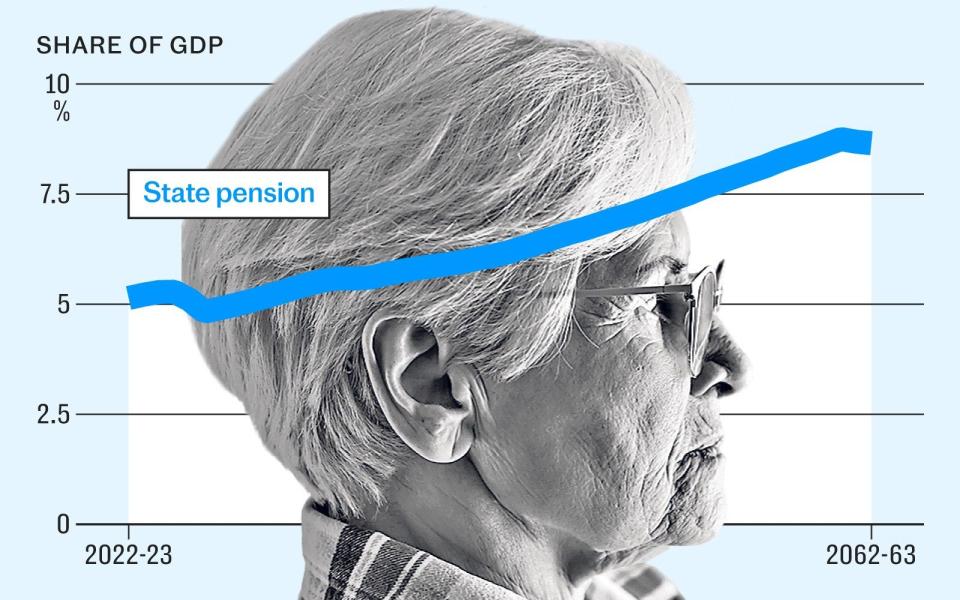

The OBR believes spending on state pensions will rise from 5.1pc of GDP this year - or around £130bn in today’s money - to 8.6pc of GDP in 2073, or around £230bn. An older population also means more demand on health spending, which is set to increase from 8.2pc of GDP this year to 15pc of GDP.

While a fall in the number of young people will reduce spending on schools over this period, the surge in older-age costs will swell the state to more than half the size of the economy, up from 33pc pre-pandemic and an estimated 38pc by the end of the decade.

Governments have two choices if they want to constrain state pension spending in the future. Make people wait longer to claim it, or make it less generous.

Life’s too short

The question of when the state pension age should rise from 67 to 68 has already been the subject of two independent reviews.

John Cridland, author of the first report in 2017, suggested it should rise to 68 between 2037 and 2039. Baroness Neville-Rolfe, the author of the second, said that based on the rule of thumb that people should spend roughly a third of their adult life in retirement, it should not rise to 68 until 2041-43.

But falling life expectancy has thrown a spanner in the works, forcing Jeremy Hunt to delay a decision on when to next increase pension age for a second time.

Advances in healthcare and better working conditions have resulted in four decades of improving life expectancy. But the rate of increase has slowed, and not just because of the pandemic.

Life expectancy growth has been slowing since 2011, with pandemic deaths in 2020 and 2021 sending progress into reverse. Life expectancy is roughly now back to where it was a decade ago, according to the Office for National Statistics (ONS).

UK life expectancy at birth is now estimated to be 78.6 years for males and 82.6 years for females, according to the ONS. That’s 38 weeks fewer for males and 23 weeks lower for females compared with 2017 to 2019.

Cridland, who wrote the first report for the Government, says: “I think there’s quite a lot of evidence that the continuing increase in longevity is topping out. And that is overlaid by the pandemic, but actually the signs were already there. If that’s the case, then you could argue the trajectory for further tightening of the state pension, both in age and support, could become more muted. My instinct is that the days of big increases in longevity are fading.”

There is also the issue of how fit people remain after they retire. The ONS defines this as an estimate of how much people believe their lives are spent in “very good” or “good” health. And the evidence suggests this is also in decline, with Scots seeing the biggest deterioration over the past few years.

Britain’s not working

Sick Britain has barely been out of the headlines since lockdown, with the number of people neither in work nor looking for a job currently at a record high of 2.8m.

A rise in back and neck pain among older workers is partly to blame. The UK is one of eight OECD countries where at least 20pc of adults aged over 65 report “severe limitations in their daily life”, according to the think-tank.

Alongside Denmark and Norway, Britain also has the highest levels of statin consumption per head in the OECD, and the third-highest use of antidepressants.

This matters because the state pension is paid from the taxes of people in work today, so the more people there are in work relative to those retired, the better.

In 2020, there were around 30 pensioners for every 100 people of working age. That has already risen to almost 32 pensioners, and will hit 35 before the decade is out – the timeline over which financial decisions at next week’s Budget are being made.

Making people wait longer to claim their pension may seem obvious, but it also risks widening the inequality gap. A recent report by the Longevity Centre suggests that people may need to work until they’re 71 before receiving the state pension to maintain the number of workers per retiree.

If that’s the case, the average person in Newton Heath and Moston in Manchester would die before receiving it. Life expectancy here is just 70.2 years old, compared with 85.6 years in nearby Deansgate.

Healthy life expectancy also varies wildly depending on where you were born. A man in Rutland can expect to live 75 years in rude health, while in Blackpool that number is just 54 years.

Even this rapidly worsening picture does not tell us everything.

Looking at the number of people of working age is one thing. Looking at how many are actually in work – and paying the taxes needed to fund the state pension – is another.

The number of working age people who are economically inactive has been rising, hitting 9.3m at the last count. That is equivalent to 21.9pc of all people aged between 16 and 64.

Lord Turnbull, a former permanent secretary to the Treasury and cabinet secretary, says major trends which have helped in past decades are no longer enough to keep the dependency ratio healthy.

“Immigration helps redress the balance, but we are now going through a phase about where have all the workers gone? There has been this huge increase in inactivity,” he says.

“By and large activity had been rising as more women came into the workforce, but inactivity turned up in pandemic and almost uniquely among comparable countries, it has not returned to its trend level - it stayed up.”

In particular, he frets that “we are the sickest country in Europe”, pushing people out of the workforce and leaving the public purse bearing the cost of healthcare bills without tax receipts.

Cridland suggests that ensuring the state pension remains fair will involve tough choices.

He says that within the next decade, if Britain wants to “start to put in place a plan to constrain cost increases without having to rob the health budget, or rob the education budget or put up taxes, the next logical thing you would do after deciding when the state pension age goes up, would in my judgment be to remove the triple lock”.

Recommended

'I spent a week living on little more than the state pension – it wasn't much of a life'

Lock and load

The policy, which was introduced at the start of the last decade, ensures that payments to pensioners rise by the highest of 2.5pc, inflation or earnings growth, whichever is higher.

It is understood that the Conservative Party will put the commitment in its election manifesto.

A Tory source said: “The triple lock is a Conservative Party creation, has been in every Conservative Party manifesto since we introduced it, and we will commit to it again.”

Labour signalled it would do the same and challenged the prime minister to put the commitment on record.

Rachel Reeves, the shadow chancellor, says: “The difference between being in retirement and being of working age is that when you’re in retirement, it is very difficult to increase your income. And so I think that stability and certainty that your income is protected is important.

“We’ve always supported the triple lock.”

A Labour spokesman added: “The Labour Party will always stand up for working people to have a fair, decent pension and financial security in retirement.

“Rishi Sunak’s government has previously broken their promise to pensioners and now need to be clear about their intention to maintain the triple lock, to ensure pensioners’ incomes don’t fall behind what is needed to give them a decent standard of living.”

Pensions minister Paul Maynard describes the state pension as a safety net for millions of people.

“I want to ensure the State Pension remains the foundation of income in retirement for future generations in a way that it is sustainable and fair,” he says.

“This Government introduced the triple lock to do just that, and since 2011 we’ve lifted 200,000 older people out of poverty. With the full rate of the new state pension rising to £11,500 in April this is vital additional money for our hard-working pensioners who rely solely on this income.

“We are taking long term decisions to build a brighter future for millions – one that delivers for the pensioners of today and tomorrow.”

But not everyone is a fan of the triple lock. Peter Lilley, a former Work and Pensions Secretary, describes it as “absurdly generous and unsustainable in the long-term”.

He adds: “Why pensioners should get an increase when neither prices are going up nor wages are going up is absurd.”

Lord Turnbull says the triple lock is “daft, but terrifically difficult to get rid of”.

“When we get a shock, an output shock or a prices shock, you suddenly find you have significantly made the pension more generous,” he adds.

“But it wasn’t a considered decision, it just happened. It is a very silly way to do it.”

The Government is committed to reviewing the state pension age again in the first two years of the next parliament.

Sir Steve Webb, the pensions minister who helped to introduce the policy, says it’s time to look at government spending as a whole to find solutions to keep the state pension on a sustainable path.

“There’s lots of things you can do to make the state pension system more affordable apart from just hiking the pension age. One of which is making more people of working age economically active,” he says.

The OBR estimates that the total annual tax loss as a result of rising health-related inactivity and in-work ill-health is likely to stand at almost £9bn a year. This would be more than enough to cut 1p off income tax - and keep paying for the triple lock.

“That’s a far better thing to focus on than just repeatedly hiking the pension age,” says Sir Steve.

“The risk is we think that the solution to the affordability of the state pension lies exclusively within the state pension system, and it just doesn’t.”

There might be more than one solution to the problem. But the state pensions time bomb is still ticking down – and hiding from reality is no longer an option.