Yahoo Finance

Yahoo Finance Willis Towers Watson (NASDAQ:WLTW) Shareholders Booked A 60% Gain In The Last Five Years

Want to participate in a research study? Help shape the future of investing tools and earn a $60 gift card!

If you want to compound wealth in the stock market, you can do so by buying an index fund. But you can do a lot better than that by buying good quality businesses for attractive prices. For example, the Willis Towers Watson Public Limited Company (NASDAQ:WLTW) share price is up 60% in the last five years, slightly above the market return. It's fair to say the stock has continued its long term trend in the last year, over which it has risen 22%.

See our latest analysis for Willis Towers Watson

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

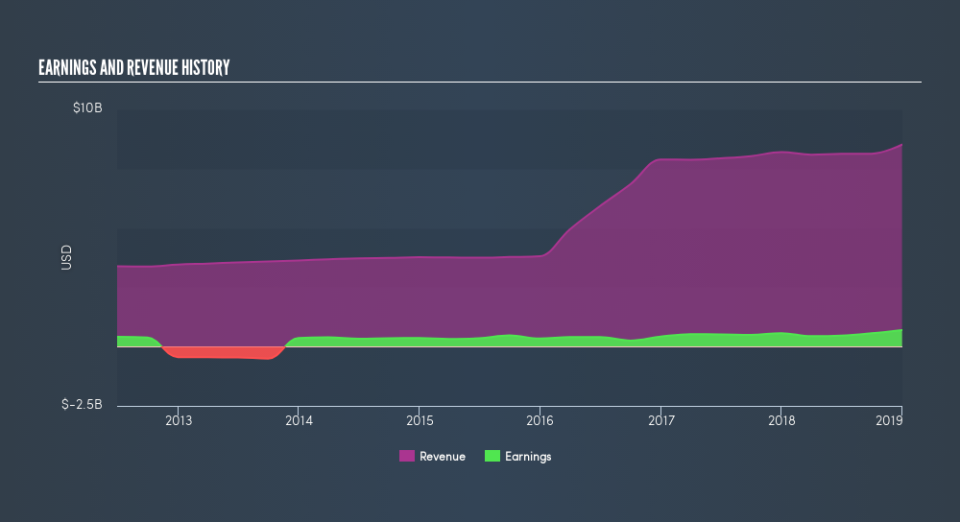

During five years of share price growth, Willis Towers Watson actually saw its EPS drop 0.8% per year. So it's hard to argue that the earnings per share are the best metric to judge the company, as it may not be optimized for profits at this point. Therefore, it's worth taking a look at other metrics to try to understand the share price movements.

The modest 1.5% dividend yield is unlikely to be propping up the share price. In contrast revenue growth of 21% per year is probably viewed as evidence that Willis Towers Watson is growing, a real positive. It's quite possible that management are prioritizing revenue growth over EPS growth at the moment.

Depicted in the graphic below, you'll see revenue and earnings over time. If you want more detail, you can click on the chart itself.

It's probably worth noting that the CEO is paid less than the median at similar sized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. You can see what analysts are predicting for Willis Towers Watson in this interactive graph of future profit estimates.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). Whereas the share price return only reflects the change in the share price, the TSR includes the value of dividends (assuming they were reinvested) and the benefit of any discounted capital raising or spin-off. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. As it happens, Willis Towers Watson's TSR for the last 5 years was 77%, which exceeds the share price return mentioned earlier. This is largely a result of its dividend payments!

A Different Perspective

We're pleased to report that Willis Towers Watson shareholders have received a total shareholder return of 24% over one year. Of course, that includes the dividend. That gain is better than the annual TSR over five years, which is 12%. Therefore it seems like sentiment around the company has been positive lately. Given the share price momentum remains strong, it might be worth taking a closer look at the stock, lest you miss an opportunity. If you would like to research Willis Towers Watson in more detail then you might want to take a look at whether insiders have been buying or selling shares in the company.

We will like Willis Towers Watson better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.