Yahoo Finance

Yahoo Finance The world’s best investors are snapping up shares in this supermarket – buy now at bargain prices

French supermarket group Carrefour has been running hard to stand still for several years. Since chief executive Alexandre Bompard announced his original turnaround plan for the group, soon after his appointment in mid-2017, investors have suffered a 3pc loss on a total return basis.

The poor performance reflects intense competition and challenges for hypermarkets, which Carrefour owns a lot of. More recent worries have centred on tough economic conditions in Latin America, which accounts for about a quarter of group sales, and the cost-of-living crisis in Europe, which accounts for the rest.

However, Mr Bompard, who is currently implementing a second strategic plan to the end of 2026, has arguably had a more positive impact on the underlying business than suggested by stock market performance.

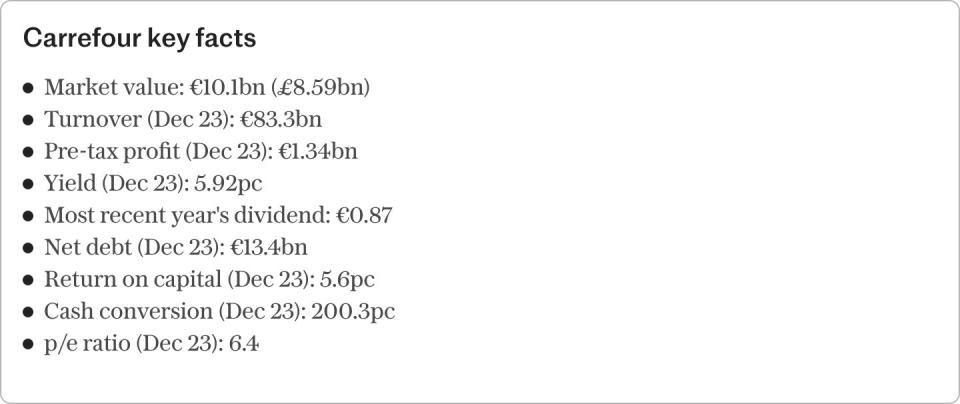

While the shares may have gone nowhere during his reign, improving business fundamentals have caused their valuation to drop significantly. On several measures, the shares are the cheapest they have been in decades and some of the world’s most successful professional “value” investors are buying.

In total, 13 of the world’s best fund managers hold shares in Carrefour. All are among the top performing 3pc of 10,000 global equity fund managers monitored by financial publisher Citywire. This has resulted in Carrefour being awarded a top AAA Elite Companies rating by Citywire, which rates companies based on the level of “smart-money” ownership.

“We think that well-managed, large food retailers are better than average businesses,” said Sean Peche, who manages the Ranmore Global Equity fund, which counts Carrefour as a top 10 holding.

“They provide a vital service to society and generate attractive returns on capital and consistent cash flow because of their favourable working capital dynamics. Under the current management team, Carrefour has doubled cash from operations over the past five years [and trades on] eight times expected earnings.”

Perhaps Carrefour’s most striking valuation credential is that free cash flow over the next 12 months is forecast to be equivalent to about 15pc of the company’s entire market value.

The balance sheet looks solid, too, boosted by last year’s €1.0bn (£852m) sale of Carrefour’s Taiwanese business. Ignoring borrowings associated with the company’s lending business and €4.9bn of lease liabilities, net debt was €2.6bn at the end of 2023. This is allowing Carrefour to return heaps of cash to shareholders.

British owners of French shares, which can be bought through most UK brokers, do need to fill out the right documents to minimise the hit from dividend withholding taxes, but Carrefour’s forecast yield stands at 6.4pc.

In addition to the chunky dividend, the company plans €700m of buybacks this year and has already reduced the share count by 17pc with repurchases since the start of 2021.

And investors can expect big cash returns to keep coming.

Management has promised 5pc-plus dividend increases out to 2026 and further annual buybacks. This is underpinned by a target to generate over €1.7bn annual free cash flow by 2026, which compares with forecasts of €1.5bn over the next 12 months. Key to hitting the target are planned cost reductions of €4bn between 2023 and 2026. Much will come from using the group’s size for better procurement, creating a leaner management and improving logistics.

Scale has recently been boosted by the company’s first major French acquisition in 20 years: the soon-to-be-completed purchase of 175 Cora and Match branded stores for €1.1bn – equivalent to 4.2 times earnings before interest, tax, depreciation, and amortisation (Ebitda) if expected cost savings are achieved. Carrefour’s Brazilian operation also had a major boost from acquisitions in 2022 with the R$7bn (£1.0bn) purchase of Grupo Big.

Efficiency is also being helped by Bompard’s strategy of operating more stores as franchises. In the company’s eight core territories, 72pc of stores now operate under such agreements.

Not all cost savings will flow to shareholders. Competition remains intense both at home and abroad and Carrefour is cutting prices to retain and win customers. This includes a target of 40pc own-label sales by 2026. The figure currently stands at 37pc, up from 25pc in 2018.

Mr Bompard believes there are also opportunities to grow profits by opening more convenience and discount stores, boosting e-commerce, redeveloping properties, and through a joint venture with advertising giant Publicis to create marketing services based on customer data.

After years of Carrefour’s shares going nowhere while fundamentals have improved, it is now priced so low that not much needs to go right for the stock to deliver. And should recent economic headwinds begin to ease, there could be significant upside.

Questor says buy

Ticker: EURONEXT:CA

Share price: €14.86

Read the latest Questor column on telegraph.co.uk every Sunday, Monday, Tuesday, Wednesday and Thursday from 8pm

Read Questor’s rules of investment before you follow our tips