Anglo American plc (AAL.L)

| Previous close | 2,182.00 |

| Open | 2,158.50 |

| Bid | 2,090.00 x 0 |

| Ask | 2,250.00 x 0 |

| Day's range | 2,138.50 - 2,193.50 |

| 52-week range | 1,630.00 - 2,658.00 |

| Volume | |

| Avg. volume | 5,939,795 |

| Market cap | 29.146B |

| Beta (5Y monthly) | 1.30 |

| PE ratio (TTM) | 114.68 |

| EPS (TTM) | N/A |

| Earnings date | N/A |

| Forward dividend & yield | 0.76 (3.48%) |

| Ex-dividend date | 14 Mar 2024 |

| 1y target est | N/A |

- Bloomberg

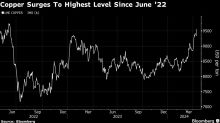

Copper’s Rally Continues as Ore Shortage Meets Resurgent Demand

(Bloomberg) -- Copper continued its upwards charge, hitting the highest since June 2022, as investors bet that curtailed ore supply will struggle to keep up with rising global demand.Most Read from BloombergTexas Warns of Possible Power Emergency Next WeekBiden to Return to White House as Israel Restricts Public LifeIsrael Bracing for Unprecedented Direct Iran Attack in DaysIsrael Versus Iran — What an Open War Between Them Could Look LikeRisk-Addicted Wall Street Funds Are Shaken as Bad News Pi

- Simply Wall St.

Investors in Anglo American (LON:AAL) have unfortunately lost 18% over the last three years

Anglo American plc ( LON:AAL ) shareholders should be happy to see the share price up 11% in the last month. But that...

- Fool.co.uk

Down more than 20% in 2023, Fools are backing these 3 UK stocks to reverse that – and then some! – by 2025

This is quite a claim. But these are quite some stocks, according to Fool UK contributors! The post Down more than 20% in 2023, Fools are backing these 3 UK stocks to reverse that – and then some! – by 2025 appeared first on The Motley Fool UK.