Yahoo Finance

Yahoo Finance This 10.6% yielder beats every dividend share on the FTSE 100. Can it last?

Just because a dividend share comes with a mind-bogglingly high yield doesn’t automatically make it a top income stock. Often, the reverse is true.

Many see an ultra-high yield as a warning signal. Especially when it hits double digits. But I’m betting that FTSE 100 insurer Phoenix Group Holdings (LSE: PHNX) is an exception.

I bought the stock both in January and March because I felt its dividends were probably sustainable. I can’t say that for sure, though.

Sky-high income

City analysts seem positive. Today, Phoenix has a trailing yield of a staggering 10.94%, but that’s just the start. It’s forecast to yield 11.2% in 2024, rising to 11.5% in 2025. One way of checking whether a yield is sustainable is by looking at recent dividend per share growth. Here’s what the charts say.

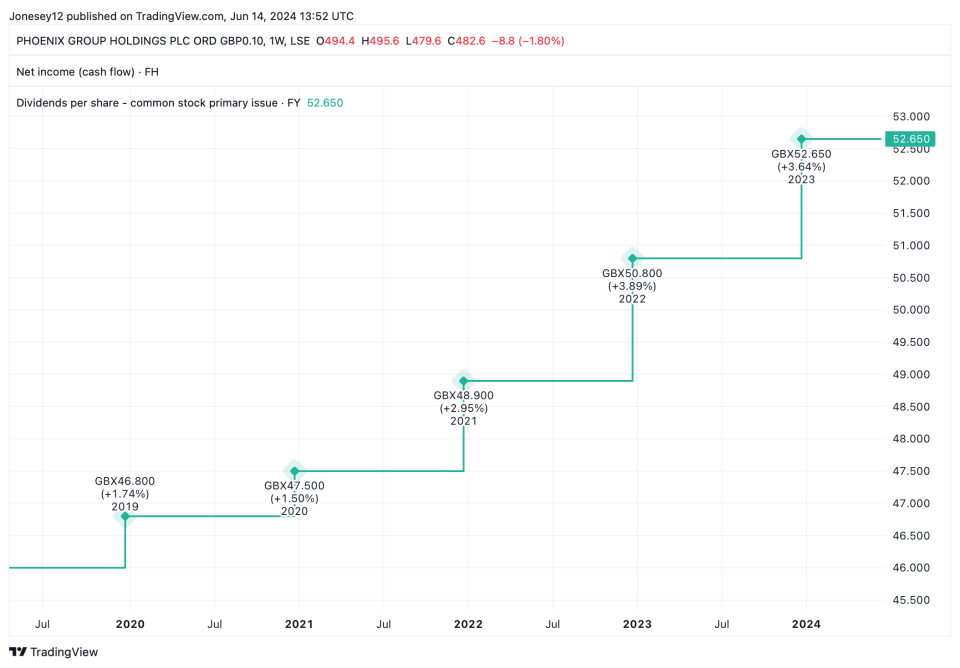

Created with TradingView

In 2019, Phoenix increase its dividend per share by 1.74% to 46.8p. It then increased payouts in each of the subsequent four years. In the last three, the percentage increases were notably higher at 2.95%, 3.89%, and 3.64%.

So rather than nervously trimming payments, management has been increasing them at a faster pace.

Investors need some reward for holding the stock, and so far it hasn’t come in the shape of share price growth. The Phoenix share price is down 12.6% over the last year, and 30.66% over five years.

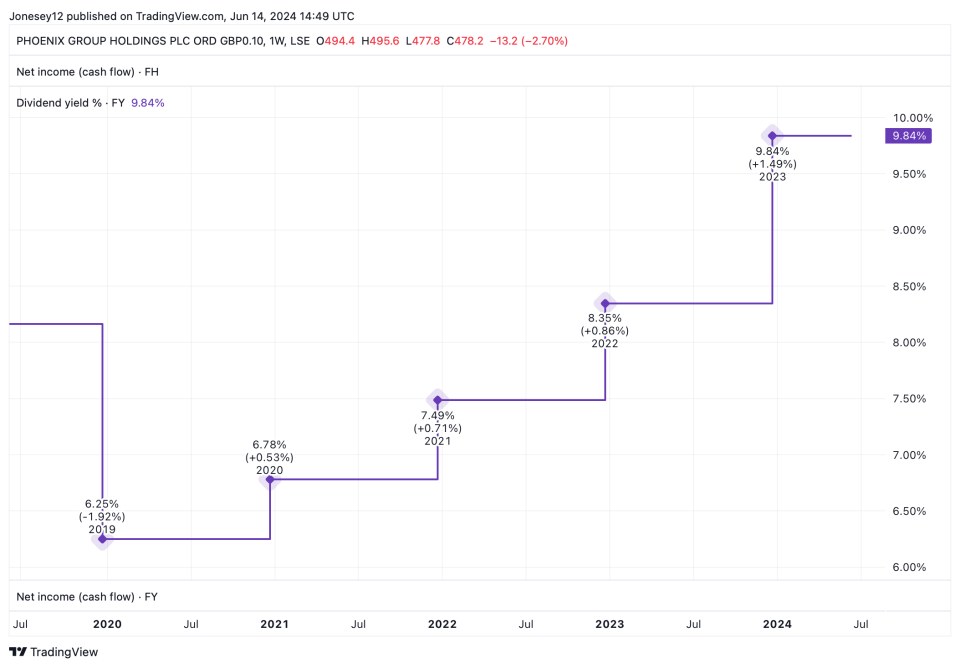

Yet the board couldn’t increase payments if it wasn’t generating enough cash. And the good news is that it is. Again, here’s what the charts say.

Chart by TradingView

In 2019, cash flows fell 1.92%. They have climbed and at an accelerating pace, rising 1.49% in 2023.

Cash flows look strong

In fact, last year was a bumper year for Phoenix. It was targeting £1.8bn of cash. It smashed that with £2bn. It boasts a solid balance sheet, too, with a Solvency II capital ratio of 176%. That’s near the upper end of its 140% to 180% target range.

Analysts are optimistic, predicting that 2023’s dividend per share of 52.65p will climb to 54.3p in 2024, 56.1p in 2025, and 57.5p in 2026. I’m feeling a little bit happier about my share purchase now.

Phoenix could get a re-rating when the Bank of England finally starts cutting interest rates. This will hit savings rates and bond yields, and make its dividend look even more attractive.

I cannot live by dividends alone. At some point, I’d like to get some share price growth too, but here the outlook is a bit more uncertain.

JPMorgan has just trimmed its Phoenix share price target from £5.25 to £5. Today, the shares trades at 4.81p. Not much scope for growth there.

For now, I’ll console myself with the income. I’ll reinvest every penny I receive to buy more Phoenix shares, and hope that one day the market comes to my point of view, and the share takes off. Fingers crossed!

The post This 10.6% yielder beats every dividend share on the FTSE 100. Can it last? appeared first on The Motley Fool UK.

More reading

Harvey Jones has positions in Phoenix Group Plc. The Motley Fool UK has no position in any of the shares mentioned. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.

Motley Fool UK 2024