Yahoo Finance

Yahoo Finance 4 Auto Equipment Stocks Standing Tall Despite Industry Woes

The prospects of the Zacks Automotive - Original Equipment industry are subdued amid a potential slowdown in the vehicle growth rate. High borrowing costs and delays in the Fed rate cut have increased challenges for industry participants closely tied to auto sales. Additionally, rising operational expenses and evolving industry dynamics pose further headwinds. Balancing revenue generation appears to be difficult, with success depending on effective cost-management strategies. However, companies such as Autoliv ALV, BorgWarner BWA, Oshkosh Corp OSK and American Axle AXL are better equipped to navigate this challenging landscape.

Industry Overview

The Zacks Automotive - Original Equipment industry includes companies that engage in the designing, manufacture and distribution of automotive equipment components used for manufacturing vehicles. A few of the components manufactured by the participants include drive axle, engine, gearbox parts, steering, and suspension, as well as brakes. Demand for original equipment depends directly on the sale of vehicles, which, in turn, is heavily reliant on economic growth and consumer confidence. Importantly, rapid globalization is opening up newer avenues for auto-equipment manufacturers who need to adapt to the changing dynamics through systematic research and development. From a future competitive standpoint, the industry players need to focus on technologies that offer the best value in a short span of time to the market.

Factors at Play

Expected Slowdown in Auto Sales Growth: Following a strong sales rebound in 2023, the auto industry is expected to see a moderate growth rate this year. With pent-up demand largely met in 2023 and high vehicle financing costs, sales growth is projected to slow down. Edmunds anticipates U.S. auto sales of 15.7 million vehicles in 2024, implying a modest year-over-year increase of 1.3% compared with 13% growth seen in 2023. Cox Automotive offers a more conservative forecast, predicting industry sales to reach 15.6 million units. This deceleration in demand growth poses challenges for industry participants whose fortunes are closely linked to auto sales.

Cost Challenges Persist: The automotive equipment industry continues to grapple with high raw material and labor costs, which remain elevated compared to pre-pandemic levels. The ongoing impact of inflation is expected to persist in the near term, putting pressure on profit margins. Additionally, the extensive global operations of many industry players expose them to potential foreign exchange issues, with unfavorable currency translations likely to impact earnings and margins.

Adapting to Technological Advancements: The automotive equipment industry is undergoing significant transformation due to rapid technological advancements and digitalization. Original equipment manufacturers (OEMs) are increasingly focusing on developing advanced components for electric vehicles (EVs) and autonomous vehicles (AVs). Stringent emission regulations are driving demand for high-quality, cost-effective auto components, creating opportunities for equipment providers. However, this technological shift requires substantial investment in research and development, posing challenges for OEMs. Effective cost management is crucial for maintaining healthy profit margins. The success of auto equipment providers will depend on their ability to manage these expenses, adapt to evolving technologies, and capitalize on new revenue opportunities.

Zacks Industry Rank is Discouraging

The Zacks Automotive – Original Equipment industry is placed within the broader Zacks Auto-Tires-Trucks sector. The industry currently carries a Zacks Industry Rank #186, which places it in the bottom 26% of around 250 Zacks industries.

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates glum near-term prospects. Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than 2 to 1.

The industry’s positioning in the bottom 50% of the Zacks-ranked industries is a result of a negative earnings outlook for the constituent companies in aggregate. Looking at the aggregate earnings estimate revisions, it appears that analysts are losing confidence about this group’s earnings growth potential. Year to date, the industry’s earnings estimates for 2024 have declined 12.7%.

Before we present a few stocks that you may still want to consider for your portfolio, let’s take a look at the industry’s recent stock market performance and valuation picture.

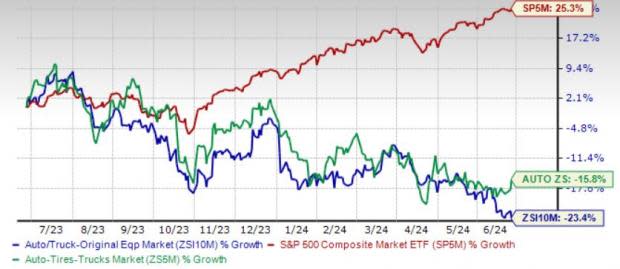

Industry Lags Sector and S&P 500

Over the past year, the Zacks Original Equipment industry has underperformed the broader Auto sector and the Zacks S&P 500 composite. The industry has lost 23.4% against the S&P 500’s growth of 25.3%. The sector has declined 15.8% over the same timeframe.

One-Year Price Performance

Industry's Current Valuation

Since automotive companies are debt-laden, it makes sense to value them based on the EV/EBITDA (Enterprise Value/ Earnings before Interest Tax Depreciation and Amortization) ratio.

On the basis of the trailing 12-month enterprise value to EBITDA (EV/EBITDA), the industry is currently trading at 12.51X compared with the S&P 500’s 19.83X and the sector’s 14.94X.

Over the past five years, the industry has traded as high as 19.87X, as low as 3.96X and at a median of 10.79X, as the chart below shows.

EV/EBITDA Ratio (Past Five Years)

4 Stocks to Buy Now

American Axle: The company is a supplier of driveline and drivetrain systems, modules and components for the automotive market.American Axle’s efforts to diversify its business, products and customer base are generating impressive results. Optimization of its portfolio via buyouts is enhancing the firm’s position. The acquisition of Metaldyne Performance Group has widened American Axle’s operating scale, customer base and end markets.As the shift toward electrification takes place, AXL is positioned as a leader in embracing this transformation through its advanced electric propulsion technology. Robust business backlog also bodes well. The company’s gross new and incremental business backlog (2024-2026) is estimated to be approximately $600 million in future annual sales.

American Axle currently carries a Zacks Rank #1 (Strong Buy) and has a VGM Score of A. The Zacks Consensus Estimate for 2024 top and bottom lines implies year-over-year growth of 3% and 544%, respectively. The consensus mark for 2024 and 2025 EPS has moved up 5 cents and 30 cents, respectively, over the past 60 days.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Price & Consensus: AXL

BorgWarner: It is one of the leading providers of clean and efficient technology solutions required for combustion, hybrid and electric vehicles. BorgWarner’s EV-focused mergers and acquisitions, coupled with the Charging Forward project, are boosting its prospects. The company expects 2024 eProduct sales to rise 25-40% year over year, with high demand for battery systems being the main driver. Frequent business wins are set to drive top-line growth. It also anticipates strong business opportunities with traditional combustion engine vehicles in North America, which would fuel its sales, profits and cash flow. Its manageable leverage, high liquidity and commitment to maximizing shareholders’ value are other positives. BWA has returned roughly 3.1 billion of capital to shareholders since 2020.

BorgWarner currently carries a Zacks Rank #2 (Buy) and has a VGM Score of B. The Zacks Consensus Estimate for 2024 and 2025 EPS implies year-over-year growth of 8% and 14.5%, respectively. The consensus mark for 2024 and 2025 EPS has moved up 15 cents and 33 cents, respectively, over the past 60 days.

Price & Consensus: BWA

Oshkosh: It is a producer and seller of a varied range of vehicle bodies and specialty vehicles.Oshkosh’s innovative new products and frequent business wins are set to drive its prospects. A solid consolidated backlog of $16.35 billion provides visibility into the coming years. The acquisition of JBT's AeroTech business has strengthened Oshkosh's Vocational segment. The company’s efforts toward modernizing fleets and broadening capabilities bode well for the Defense segment's prospects. A strong balance sheet and investor-friendly moves are other positives.Healthy demand for products, solid business execution across segments, the launch of innovative offerings, capacity expansion and acquisition synergies are boosting the company’s growth.

Oshkosh currently carries a Zacks Rank #2 and has a VGM Score of B. The Zacks Consensus Estimate for 2024 and 2025 EPS implies year-over-year growth of 12% and 6.4%, respectively. The consensus mark for 2024 and 2025 EPS has moved up 12 cents and 10 cents, respectively, over the past 30 days.

Price & Consensus: OSK

Autoliv: The company is at the forefront of automotive safety technology. With content per vehicle on the rise, Autoliv is set to gain from the growing demand for front-center airbags, rear-side airbags and pedestrian protection products. Electric vehicles are opening new growth avenues for the firm. In 2023, order win rates for new EV platforms were high, with around 45% for EVs.Strategic structural initiatives, stringent cost control measures and effective customer compensation strategies are expected to boost Autoliv’s operating margins in 2024.Encouragingly, Autoliv envisions operating cash flow for 2024 to be $1.2 billion, up from $982 million in 2023.The firm remains committed to increasing shareholder returns thanks to its strong financials.

Autoliv currently carries a Zacks Rank #2 and has a VGM Score of B. The Zacks Consensus Estimate for 2024 and 2025 EPS implies year-over-year growth of 19% each. The consensus mark for 2024 and 2025 EPS has moved up 7 cents each, respectively, over the past 60 days.

Price & Consensus: ALV

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Autoliv, Inc. (ALV) : Free Stock Analysis Report

BorgWarner Inc. (BWA) : Free Stock Analysis Report

American Axle & Manufacturing Holdings, Inc. (AXL) : Free Stock Analysis Report

Oshkosh Corporation (OSK) : Free Stock Analysis Report