Yahoo Finance

Yahoo Finance ‘Can I afford to semi-retire – and spend winters abroad?’

Would you like a Telegraph Money Makeover? Apply here or through the form at the bottom of the page

Charlie Burrows, 47, and wife Anna have lived in Cambridge happily for the past 16 years, but increasingly they find themselves dreaming of a life in the sun.

“I was born in Australia. My family moved over there in the 1960s, so it’s somewhere I have a lot of nostalgia for. I have an Australian passport so moving there, at least for part of the year, is definitely a possibility,” said Mr Burrows.

Mr Burrows works in technology, while his wife is the founder of her own company, Cherry Hinton Accounting. Their jobs are intense and recently the couple have been drawing up plans to semi-retire in 10 years’ time, taking off to Australia every year for some winter sun.

But there are a number of questions they want answered so they can make their dream a reality. The first is whether they are taking the right steps to grow their pension so they can enjoy life by the pool. Charlie has a pension worth around £140,000, 30pc of which is invested in the stock market, 58pc in cash, and the rest in bonds and property funds. He contributes about £10,000 a year.

The second question is what to do with their rental property in London. The £425,000 two-bed flat generates an income of £1,300 per month, and it could also be a home for their children once they graduate, so there are strong arguments for keeping it.

But, says Mr Burrows, “it will become difficult to manage renting it out if we do move abroad for part of the year. I wonder if we should eventually sell and invest that money elsewhere.”

Ideally, Mr Burrows and his wife would also be debt-free by the time they are semi-retired. They are in the lucky position of almost owning both their properties outright. They have just £35,000 outstanding on their Cambridge home, with their 3pc mortgage deal ending in 2025, and a £5,000 mortgage on their London flat.

“We have £23,000 in savings which could be used to pay off the debt, but perhaps it would be better to invest this money,” said Mr Burrows.

His wife Anna is also considering opening a small self-administered pension scheme or “Ssas” through her limited company, and wants some advice on the pros and cons of doing so.

Olly Cheng, associate director at Saunderson House, says:

With a current pension pot of around £140,000 and expected contributions of £10,000 per year, the growth rate of the pension over the next 10 years will be crucial to determine what income they would be able to draw in retirement.

If we assume 3pc growth each year, they would have a final pot of £284,000, while a growth rate of 6pc per annum would generate a pot of around £351,000, which is a very significant difference.

This raises some big questions about how their pension should be invested. Over a 10-year period, investing a higher proportion of pension assets in equities would be likely to provide a higher rate of return (although this isn’t guaranteed), and therefore could be a good way of trying to increase their pension income in retirement.

The current asset allocation, with over half the pension held in cash, is quite cautious, and should definitely be reviewed to see if it is appropriate. However, it is important to understand that more equity exposure, and the higher volatility that comes with it, isn’t right for everyone, and so it would be best to speak to an adviser and have an in-depth conversation about risk before making any changes.

Assuming a 4pc rate of drawdown, a pension of £351,000 would give an annual income of around £14,000, although if they retire at age 57, they may want to take a slightly higher amount in the first 10 years before their state pensions come into payment. Cashflow forecasting could help with understating the pros and cons of this approach.

Based on today’s rates, a higher annual income could potentially be obtained by purchasing an annuity. However, on the basis that they may need a higher income for the first 10 years of retirement to bridge the gap before their state pensions, I’d be cautious about this option.

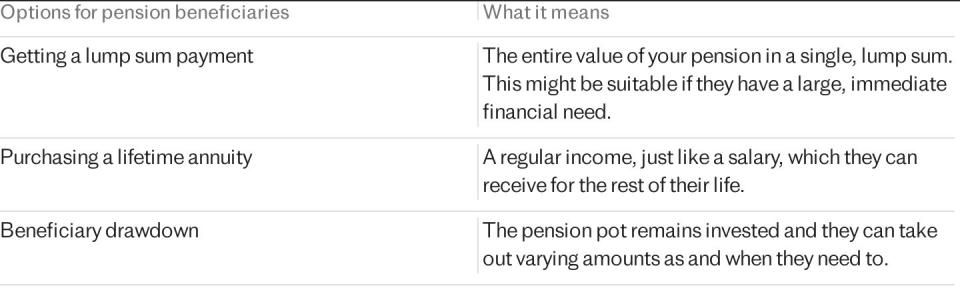

It would also mean less money left to their eventual beneficiaries.

Finally, using a small self-administered pension scheme is a major decision and one to take professional advice on.

The advantages include: the ability to buy commercial property and potentially lease it back to your company; the opportunity to invest in your company by buying an equity stake; and the ability to loan money to the company.

However, all of these investment strategies do tie your retirement plans in very closely with your business, and there is a real possibility of getting to retirement age and finding that these assets can’t be liquidated, so please proceed with caution.

Holly Tomlinson, financial planner at Quilter, says:

When considering whether to clear your mortgages, it is important to first explore whether there would be any fees payable if you opted to do so. Many mortgages will have an early repayment charge, which will be a percentage of what you still owe on your mortgage agreement, so given the relatively short amount of time left on your fixed term deals it may be worth waiting until the end of them to clear the mortgages to help avoid these exit penalties.

If there are no exit charges payable, check where your cash is being held to see whether it is earning more than the 3pc interest you are currently paying on the mortgage.

If it is, it may be worth leaving the cash where it is and paying off the lump sum when the mortgage deals come to an end.

For your buy-to-let property, the first port of call would be to have a conversation with your children about the options you have available to you regarding the flat. Though they are still relatively young, you may be able to come to a decision as a family which could help discount one or other of the options, and help you make a more confident decision.

If you opt to sell the flat to alleviate the pressures that come with managing it and to allow you to freely spend the winter months in Australia, it is important to remember that capital gains tax will be applicable when selling.

Recommended

Six easy (and completely legal) ways to avoid capital gains tax

However, it is likely that a tax efficient wrapper could be utilised to invest the funds, which would be able to provide you with a similar, if not better return than the rental income. Assuming you are currently paying basic-rate tax on the rental income, by investing this money in a more tax-efficient solution such as pensions and Isas you may be able to reduce your tax liability while also providing yourselves with a better future income when you look to semi-retire.

Based on investing £425,000 into a moderate fund for 10 years, assuming roughly 4pc growth, you would have a fund value of around £520,000. This equates to around £30,500 of annual income paid via an annuity until death.

Simplifying your investments by potentially selling the flat, clearing the mortgages on both of your properties at the end of the fixed rate term or sooner if you will not incur a fee, and reinvesting in tax efficient wrappers such as pensions and Isas will be a good place to start to ensure you are well placed to semi-retire when you are ready to.