Yahoo Finance

Yahoo Finance Annual growth in house prices turns positive for first time since January 2023

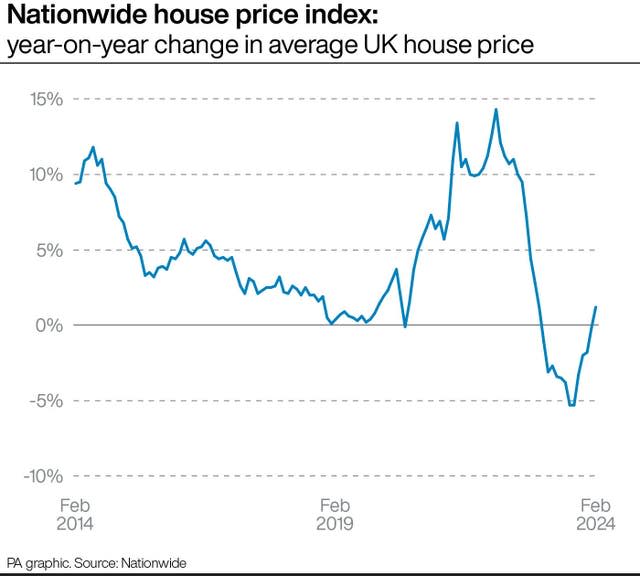

Annual growth in house prices turned positive for the first time in around a year in February, according to an index.

Across the UK, property values increased by 1.2% annually in February, following a 0.2% fall in January, Nationwide Building Society said.

It marked the first month since January 2023 that Nationwide recorded positive annual growth in house prices. In that month, there was a 1.1% year-on-year increase.

On a month-on-month basis, house prices increased by 0.7% in February, taking the average UK house price to £260,420.

Robert Gardner, Nationwide’s chief economist, said: “House prices are now around 3% below the all-time highs recorded in the summer of 2022, after taking account of seasonal effects.”

He continued: “The decline in borrowing costs around the turn of the year appears to have prompted an uptick in the housing market. Indeed, industry data sources point to a noticeable increase in mortgage applications at the start of the year, while surveyors also reported a rise in new buyer inquiries.

“Nevertheless, near-term prospects remain highly uncertain, in part due to ongoing uncertainty about the future path of interest rates. After falling sharply in late December, swap rates, which underpin fixed rate mortgage pricing, have drifted back up.

“Borrowing costs remain well below the highs recorded last summer but, if the recent upward trend is sustained, it threatens to restrain the pace of any housing market recovery.

“While the squeeze on household budgets is easing, with wage growth now outstripping inflation by a healthy margin, it will take time to make up for the ground lost over the past few years, especially given consumer confidence remains fragile.”

Earlier this week, the Bank of England said that the number of mortgage approvals made to home buyers jumped to the highest level since October 2022 in January this year.

HM Revenue and Customs (HMRC) figures showed this week that 82,000 home sales took place in January, which was 12% lower than January 2023 and 2% higher than December 2023.

It was the first month-on-month increase in house sales since August 2023 – however, it was still the lowest level of house sales recorded in January since 2013, HMRC said.

Alice Haine, personal finance analyst at Bestinvest by Evelyn Partners, the wealth manager, said: “While buyer appetite is likely to have been boosted by easing mortgage rates in the first few weeks of the year, some lenders increased rates in February as uncertainty around Bank of England interest rate cuts clouded the outlook.”

Tom Bill, head of UK residential research at Knight Frank, said: “Buyers feel confident that the only way for the base rate is down, which has seen demand and house prices pick up in recent months.

“However, the upwards pressure on mortgage rates in recent weeks shows sellers the importance of getting the asking price right.”

Mark Harris, chief executive of mortgage broker SPF Private Clients, said: “Mortgage rates are more attractively-priced than they were several months ago, even if the ‘best buy’ deals have been pulled recently.

“There will be ups and downs in mortgage pricing in the weeks and months ahead but there is a growing feeling of optimism that the situation is improving overall, which will be welcomed by hard-pressed borrowers.”

Nicky Stevenson, managing director at estate agent group Fine & Country, said: “We’re heading into one of the prime seasons for home sales, and sellers should look at this as a great time to get their home on the market.

“Properties tend to sell fastest at this time of year, and motivated buyers are still snapping up homes in desirable areas.”

Yasin Patel, co-founder of property investors Autarky Sukuk, said: “While these figures give a good overview of the current state of house prices, they don’t show how wildly they can vary from place to place.”

Sarah Coles, head of personal finance at Hargreaves Lansdown, said: “As average house prices rise back over £260,000 it raises another problem, because higher house prices, coupled with rising mortgage rates, risk pushing property out of reach for buyers again.”

Iain McKenzie, chief executive of the Guild of Property Professionals, said: “We’re expecting to see the housing market back on the march this year, and a return to positive annual price growth is another good sign.

“Growth will be welcomed by sellers that have been cautious to stick out the ‘for sale’ signs since prices began to ease.”

Martin Beck, chief economic adviser to the EY Item Club, said: “February’s outturn bolsters the EY Item Club’s view that the correction in property values seen in late 2022 and part of last year has ended. An improving economic outlook has helped.”

But he continued: “There’s already evidence that quoted mortgage rates are rising in response to markets paring back expectations of the scale of Bank of England rate cuts this year. This is likely to continue over the next few months. But even allowing for this, the EY Item Club now thinks 2024 should be a year of modest growth, rather than stagnation, in house prices.”