Yahoo Finance

Yahoo Finance The battle to take on BT in Britain’s brutal broadband war

Ensconced in a hotel off Barcelona’s La Rambla, Telefonica boss Jose Maria Alvarez-Pallete was in a jubilant mood.

The Spanish telecoms executive, who is well known in his home country, was mobbed by reporters as he celebrated Telefonica’s 100th anniversary on the sidelines of the Mobile World Congress conference last week.

Yet amid the festivities there was a bum note: Virgin Media O2. Telefonica’s milestone came less than a week after it wrote down the value of its stake in VMO2, which it jointly owns with Liberty Global, by €1.8bn (£1.5bn).

The lower valuation belies wider struggles in the broadband market. After years of start-ups and rivals attempting to challenge the dominance of BT, the full-fibre broadband race is now coming to a head.

Despite competition, BT has expanded its dominant network at pace and is now shifting its focus to connecting more customers.

Meanwhile, the industry is bracing for a wave of consolidation as scores of smaller “alt-net” rivals teeter on the brink of collapse after a surge in borrowing costs.

VMO2 hopes to pounce on these stragglers as it looks to build a national fibre network to take on BT. Yet it has its own mountain of debt to contend with, while tight margins and tough competition in its mobile business are also taking their toll.

It is a make or break moment. One former Virgin Media executive says: “I think the whole sector has got some horrendous headwinds at the moment and the models of old are under huge, huge pressure.

“Bring in the spectre of debt on top of it and it’s hard. It’s a very, very hard business.”

When VMO2 was formed in a £31bn mega-merger three years ago, bosses hailed a “game-changing” deal that would bring together mobile and broadband services into one major player. The company had ambitions to challenge BT as a truly national telecoms giant.

The tie-up created lucrative synergies but also left the company laden with £20bn of debt. Surging interest rates have now driven up the cost of servicing those borrowings.

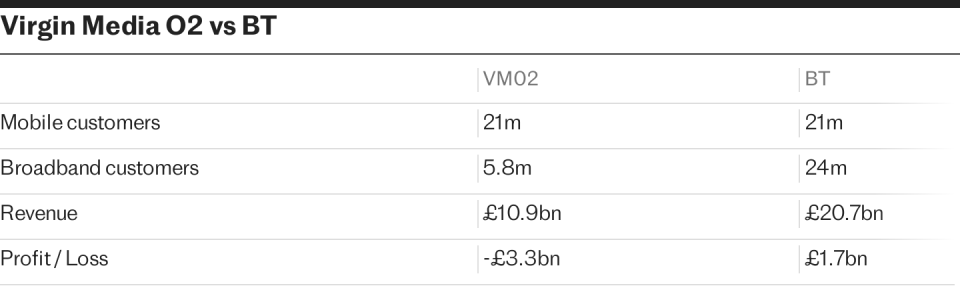

The telecoms group reported a £3.3bn loss last year, largely driven by a £3.1bn writedown in its valuation, which shareholders blamed on higher rates as well as wider economic malaise in the UK.

At the same time, the cost of living crisis has taken its toll on VMO2’s business as consumers spend less on new handsets and ditch mid-level TV packages. Mobile revenue was broadly flat at £5.95bn last year, while consumer fixed revenues, which cover broadband, TV and landline, fell 2.3pc to £3.3bn.

VMO2 has confirmed it will raise prices by nearly 9pc this April, though this will provide less of a boost than the inflation-busting increases pushed through last year.

Meanwhile, competition in the mobile market is increasing. Vodafone and Three are poised to merge in a £15bn deal that will create the UK’s largest mobile network.

Karen Egan, head of mobile at Enders Analysis, warns VMO2 faces a “tricky” year ahead.

“On both mobile and fixed the company had significant advantages in the market for a long time – custom plans on mobile and very high speeds on fixed,” she says.

“Those advantages are now largely eroded, making it much more difficult to make headway in the market.”

VMO2’s rapid broadband speeds have now been matched by BT and alt-nets, while other mobile operators have imitated O2’s split contracts that allow customers to pay for handsets and airtime separately.

The company announced up to 2,000 job cuts last July and insiders acknowledge that the sweeping redundancies have hit morale. VMO2 has also suffered several recent executive departures, including chief operating officer Jeff Dodds and networks boss Rob Evans.

For boss Lutz Schüler, 2024 is a turnaround year. The company is planning higher investment, splashing out on marketing as it looks to boost customer numbers and return to growth.

It has also taken more drastic action. VMO2 recently announced the launch of a new infrastructure business that will open up its network to other providers for the first time.

The former executive describes the move as “radical”, adding: “Historically they were always very reluctant to allow anyone else on to their network.

“But if they open that up to providers I think that makes a lot of sense. It’s reflecting the pressure they’re under that they’re prepared to share that core asset.”

The new division is expected to provide a vehicle for the company to snap up struggling alt-nets, whose debt-funded business models have been put under strain by rising interest rates.

VMO2 has previously explored a potential £3bn takeover of largest alt-net Cityfibre, which would give it significant firepower to challenge BT’s network.

It has also held talks about an acquisition of TalkTalk’s consumer network, in a move that would enable it to expand out of its traditional premium business and into the lower end of the market.

VMO2 could also look to drum up outside investment for its infrastructure arm – an appealing prospect for investors looking for predictable returns without the headaches of a consumer business.

James Ratzer, an analyst at New Street Research, says the company will require ongoing investment to maintain its services against the backdrop of slowing growth, the cost of living crisis and BT’s rapid full-fibre rollout.

Ultimately, a merger with Nexfibre, a separate infrastructure business also co-owned by Liberty Global and Telefonica alongside French private equity firm InfraVia, could be on the cards.

Even if there is no tie-up, change may be on the cards. Both Liberty Global and Telefonica have the right to initiate a stock market float in June under the terms of VMO2’s original merger deal.

With the telecoms sector out of favour with investors and VMO2 laden with debt, bosses acknowledge that now is not the right time to float.

Still, Liberty is actively looking at ways to monetise its assets. The US group has outlined plans to list its Swiss business later this year as it slims down its telecoms empire.

It plans to strip 1.5bn Swiss francs of debt from the business ahead of the initial public offering, providing a potential template for VMO2.

It is also selling off assets elsewhere, including offloading Gogglebox producer All3Media to RedBird IMI, the Abu Dhabi-backed fund that is also trying to buy The Telegraph.

Telefonica’s long-term plans are less clear, but the company has tried to sell off its holding in O2 twice before.

To many observers, the 50:50 tie-up between Liberty and Telefonica raises questions about who is in control and what they want to do with the business.

“Liberty Global tends to take a very financially pragmatic approach to businesses – they don’t let sentimentality get in the way of a good deal,” says Egan.

“Telefonica is likely to have a more strategic view of the UK business, something that aligns well with their other operations around the world.”

VMO2 insists its shareholders are aligned. Still, their joint control of the venture could be up for review as part of a stock market float.

With the company at a crossroads, questions have also been raised about the future of Schüler, who has held the top job for five years.

Industry insiders suggest Stephen van Rooyen, who recently stepped down as UK chief executive of Sky, could be a potential replacement if Schüler does move on. Speculation is also rife about the next move for Marc Allera, the EE boss who was overlooked for the top job at BT.

Insiders insist that Schüler is not going anywhere soon and his immediate priority is to return VMO2 to growth. But as the dust settles after Barcelona’s celebrations, he is likely to have shareholders breathing down his neck.

A VMO2 spokesman said: “While 2024 has a tougher outlook, this year is all about making key investments that will lay foundations for growth – we will increase our capital expenditure to over £2bn while still guiding to produce around half a billion of free cash flow this year.

“The underlying health of the business is unquestionable, and we have the full backing of our shareholders on this long-term strategy.”