Yahoo Finance

Yahoo Finance Best children’s savings accounts of 2024

Setting money aside for your children is about more than just putting money into a piggy bank.

With the average cost to raise a child estimated at more than £220,000 until they reach age 18, saving money to manage life’s many milestones for your children can be beneficial.

A child savings account can help build a nest egg to cover costs such as school fees, university or their first car, while also teaching the younger generation about money matters.

There are different types of child savings accounts and some may even pay better rates than adult alternatives, albeit with certain restrictions.

Here are the best child savings accounts, and how to find them.

What makes a good child savings account?

As with any savings account, you’ll want to secure a decent rate for your child – but it’s also important to consider how much you can contribute and how easy it is to manage.

For example, can you only open the account in branch and can it be managed online? Is it possible to make withdrawals if needed?

Some providers may offer debit cards once a child is 11, which can be useful if you want to start teaching them about spending and financial responsibility.

When it comes to trying to find an account, many banks and building societies offer child savings accounts.

They can often be opened with as little as £1 by parents or guardians until the child is 18, but the child may also be able to manage the account once they are seven years old in some cases.

Parents can choose between easy access – where you can usually add or withdraw money freely – and regular saver accounts, which require deposits to be made on a regular basis.

Aimed at parents saving on behalf of children, these accounts often offer attractive rates but restrict how much you can actually deposit or how much interest is paid on to keep the total returns down.

Easy access accounts may limit how much you can save and earn interest on for your child overall, while a regular saver will have rules on how much can be contributed each month.

The rates on offer will either be fixed for a set period or variable, and can therefore change at any point.

It is important to keep an eye on the rate once a deal period ends as the rate could drop and it may be worth moving your money to seal a better return.

Watch out for minimum and maximum age requirements as this may affect when you can start saving for your child, and how long you can save for.

Watch out for tax

Children don’t usually have to pay tax on savings interest. This is because the amount saved and interest earned rarely exceeds the personal savings allowance (PSA) threshold.

But if a parent is contributing money into the account and it earns more than £100, this will go towards their own PSA.

If you are worried about this, another type of child savings account is the junior Isa (Jisa).

This has a separate annual £9,000 allowance to the adult Isa that can be put into a cash or stocks and shares Isa for children to access after the turn 18. All growth is tax-free – for both children and parents.

Best child savings accounts of 2024

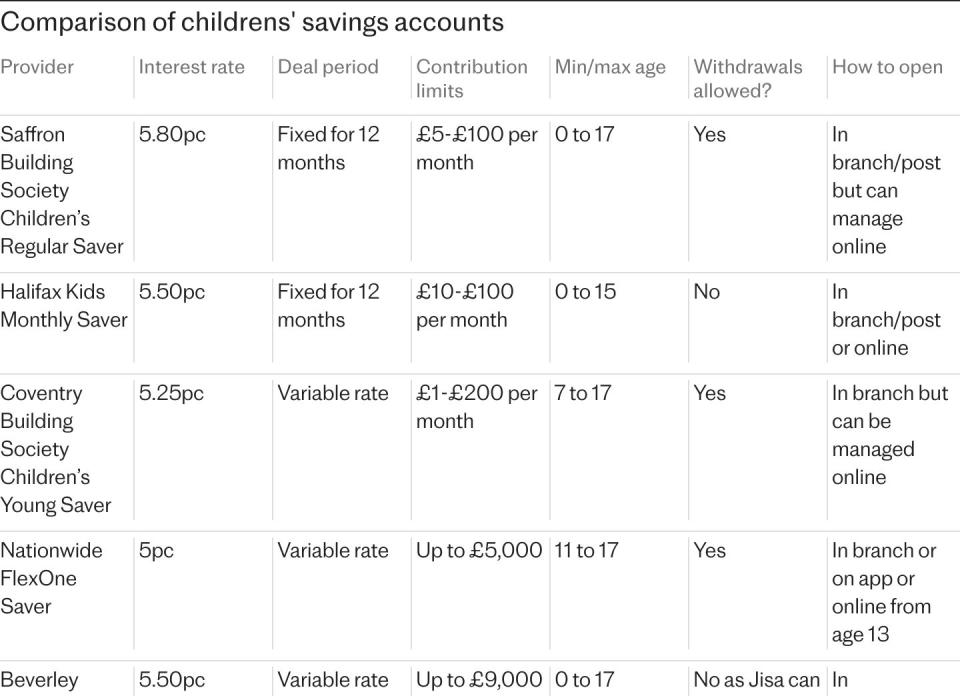

Saffron Building Society currently offers the top-rate children’s savings account on the market, which pays 5.8pc.

It is a regular saver so parents have to contribute between £5 and £100 per month to get the rate. It can only be opened by post or in branch, but can be managed online.

If you made the maximum monthly contribution of £100, the balance could be worth £1,237.70 by the end of the 12-month period.

The rate becomes variable after 12 months, so could drop or even rise.

Halifax’s Regular Saver pays 5.5pc fixed for a year, and can also be opened online.

The account can be opened once a child is born and interest can be earned until they are 15. While withdrawals aren’t allowed, you can close the account and access the money without penalty.

A £100 monthly deposit would be worth £1,233 after 12 months. Similar to Saffron, the Halifax rate could drop after 12 months, when it moves to being a variable-rate account.

Coventry Building Society offers 5.25pc for its children’s savings account.

Not only is the rate good, it is an easy access account, so the money can be deposited and withdrawn when needed, and there is no requirement to contribute every month.

It can be opened for a child from age seven until they are 17 and the deposit limit is £1 to £200 per month. The account must be opened in branch, but can then be managed online.

A monthly contribution of £100 would be worth £1,233.95 after 12 months. The rate is variable though, so could change at any point.

If you already have a FlexOne current account from Nationwide, you can also open a savings account for your child from age 11 to 17. It can be opened through the app once the child is 13, or through a branch if younger.

The account pays 5pc interest on between £1 and £5,000 and also comes with a debit card for the child.

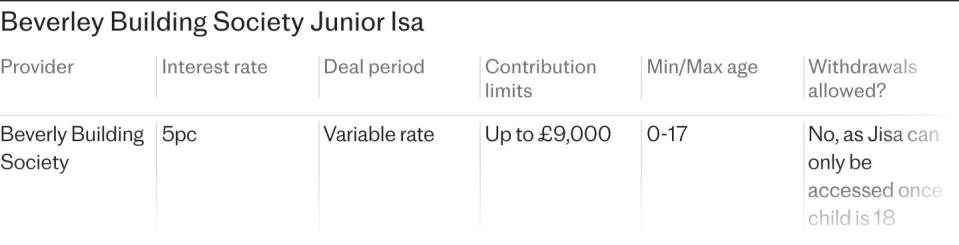

Beverley Building Society tops the tables if you want a tax-free savings option.

Its cash Jisa has an interest rate of 5.5pc from £1. A £1,000 deposit would be worth £1,055 after 12 months.

The catch is that you need to live in HU, YO or DN postcode areas and can only apply in branch or by post.

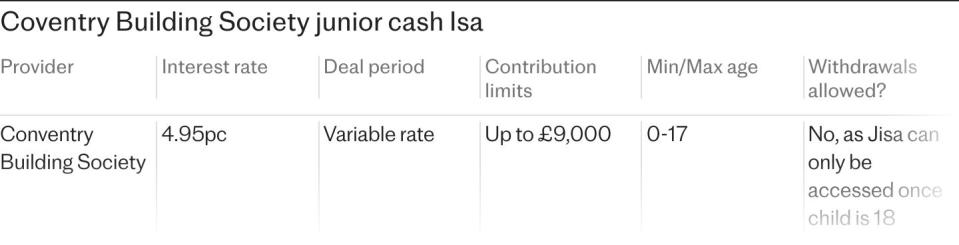

Coventry Building Society’s cash Jisa offers a slightly lower rate at 4.95pc but can be opened in branch or over the phone with no geographic restrictions.

A £1,000 balance would be worth £1,049.50 at the end of 12 months.

How to open a child savings account

Depending on the provider and type of account, some may let you open an account online or you may have to visit a branch or do it by post.

Check the small print to make sure your child is the right age and you can save the amount you want to.

Providers may have their own rules for how old a child needs to be to open an account under their own name and young children, often under 8, typically need a parent to sign and set one up on their behalf.

You may need to provide documents such as a birth certificate for the child and your own ID.

Managing your child’s account

Some accounts may let children manage the account themselves from a certain age depending on whether they were made a signatory when it was opened.

They usually convert to an adult savings account once the child turns 18, but there is more flexibility before that and you may be able to access the funds if needed.

Jisas work differently. They can only be opened by parents or guardians and other relatives or friends can contribute but the money is locked away until the child becomes an adult. It is possible to transfer the money to different Jisa accounts, though.

A Jisa can be managed by the child it was opened for from age 16 and accessed by them once they are 18. This means they could just spend all of it and there is not much you can do to stop them.

It is worth considering how much control you want over the savings when choosing a children’s savings account and if you trust your child to use the money responsibly once they get their hands on it.