Yahoo Finance

Yahoo Finance Broker Revenue Forecasts For 2seventy bio, Inc. (NASDAQ:TSVT) Are Surging Higher

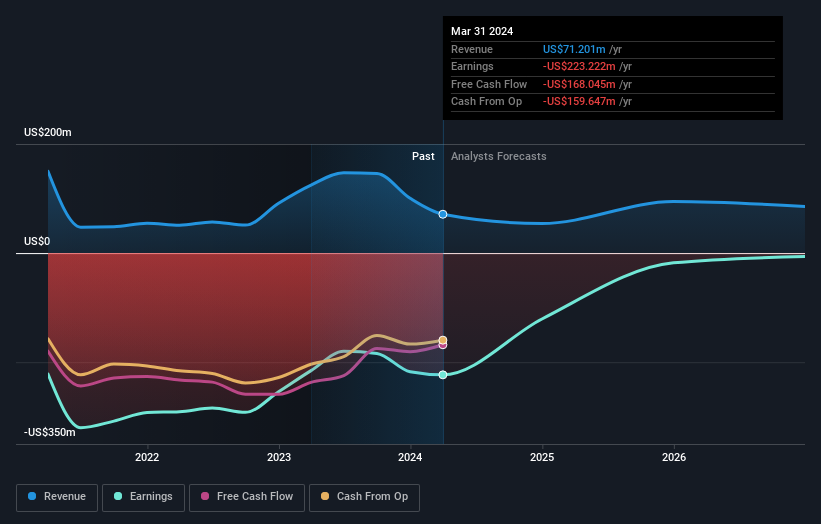

Celebrations may be in order for 2seventy bio, Inc. (NASDAQ:TSVT) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The revenue forecast for this year has experienced a facelift, with analysts now much more optimistic on its sales pipeline. The market may be pricing in some blue sky too, with the share price gaining 11% to US$4.01 in the last 7 days. We'll be curious to see if these new estimates convince the market to lift the stock price higher still.

Following the latest upgrade, the seven analysts covering 2seventy bio provided consensus estimates of US$54m revenue in 2024, which would reflect a stressful 24% decline on its sales over the past 12 months. The loss per share is anticipated to greatly reduce in the near future, narrowing 42% to US$2.53. Yet prior to the latest estimates, the analysts had been forecasting revenues of US$46m and losses of US$2.71 per share in 2024. So there's been quite a change-up of views after the recent consensus updates, with the analysts making a sizeable increase to their revenue forecasts while also reducing the estimated loss as the business grows towards breakeven.

See our latest analysis for 2seventy bio

Of course, another way to look at these forecasts is to place them into context against the industry itself. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 31% by the end of 2024. This indicates a significant reduction from annual growth of 16% over the last three years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 18% per year. It's pretty clear that 2seventy bio's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The highlight for us was that the consensus reduced its estimated losses this year, perhaps suggesting 2seventy bio is moving incrementally towards profitability. Pleasantly, analysts also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow slower than the wider market. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at 2seventy bio.

Analysts are clearly in love with 2seventy bio at the moment, but before diving in - you should be aware that we've identified some warning flags with the business, such as a short cash runway. For more information, you can click through to our platform to learn more about this and the 2 other concerns we've identified .

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com