Yahoo Finance

Yahoo Finance Budget 2017: first-time buyer stamp duty break 'misses the point'

Chancellor Philip Hammond has abolished Stamp Duty for first-time buyers on purchases of up to £300,000, and on the first £300,000 of purchases up to £500,000. Click here for a detailed report. This story was originally published on November 21.

Embattled Chancellor Philip Hammond has indicated that he will use tomorrow's Budget to address Britain's housing crisis, and a stamp duty exemption – only for those buying their first home – is expected to be a headline policy.

But mortgage lenders and housing analysts have said the initiative would do little to help those struggling to buy. Nor, they say, would it address the core problem in the housing market, which is the difficulty faced by existing owners in both moving up the ladder and downsizing.

This has led to a slump in housing transactions of approximately 35pc since the financial crisis. Support is growing for a far more radical overhaul of the stamp duty regime, as called for by this newspaper, as a way of stimulating further housing supply, labour mobility and freeing up existing stock for older home-owners keen to downsize.

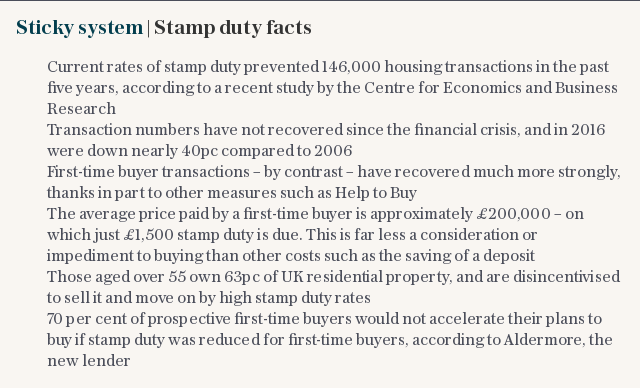

The current stamp duty regime has resulted in 146,000 fewer housing transactions during the past five years, according to a report published last week by lender Santander and think tank the Centre for Economics and Business Research.

Christian Jaccarini, an economist at the CEBR, said the inability of existing owners to take a " second step" up the ladder – thanks largely to hefty duties – "constrains the supply of homes appropriate for first-time buyers".

He added: "Clearly, building more houses in the first-time buyers' price range is key, but an efficient form of taxation is important for ensuring that we make the most of the existing property stock."

He called for a "thorough review" of stamp duty in tomorrow's Budget, as "there are other ways of earning this tax revenue without incurring these negative consequences".

Limited benefit for first-time buyers

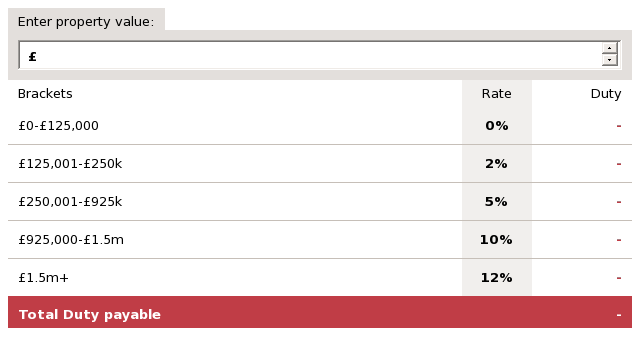

Besides London, where the average first-time buyer spends £422,000, the savings would be small relative to the other hurdles associated with buying a first property.

The average first-time buyer price across the country is £200,000.

Outside of the South and eastern England, the savings involved in scrapping duty for first-time buyers would be less than £1,000.

In all regions, large deposit requirements caused by soaring house prices and the income required to obtain a large mortgage remain the biggest problems.

Lucy Brennan, a partner at accountancy firm Saffery Champness, said: "Once first-time buyers have saved for a deposit, stamp duty might not actually be a significant cost for them at all. In London, although the stamp duty saving seems large at an average of £11,000, compared with the cost of a deposit it's not a huge saving."

Once first-time buyers have saved for a deposit, stamp duty might not actually be a significant cost for them at all

Roshini and Nicholas Agyemang, pictured above, aged 30 and 27, respectively, are currently buying their first home in south London, for £405,000. They have a 2.04pc five-year fixed deal with Nationwide requiring a 20pc deposit. Under the current rules, their total stamp duty bill would be £10,250, compared with more than £80,000 for the deposit.

Reader Service: For fee-free advice on your next move, Telegraph Mortgage Advice’s experts can provide guidance on your next mortgage. Call today on 0800 073 2322 or click here for more information.

For them, while not paying stamp duty would be a positive in the short term, the deposit was their primary problem.

"Not having to pay that money would be great – we'd be able to furnish the house. At the moment, I think we'll just be able to get a bed," said Mrs Agyemang, who works as a laboratory quality control analyst

"But we didn't think about stamp duty to start with. It came later on, when we looked at mortgage payment amounts and other details."

The real problem is in the wider market

While the Chancellor is tipped to focus on stamp duty relief at the first-time buyer end of the market in tomorrow's speech, statistics suggest the real problem is higher up the ladder.

In fact, thanks to other first-time buyer initiatives such as Help to Buy, most analysts say the lower rungs of the housing market are healthier than those higher up.

Between 2011 and 2016, the number of first-time buyer transactions increased by 75pc, according to data from mortgage trade body the Council of Mortgage Lenders. By comparison, during the same period, the number of home mover transactions increased by just 14pc.

A wider reduction in stamp duties would increase transactions across the entire property market and have a knock-on benefit for first-time buyers, explained Ms Brennan.

"For a first-time buyer to get a house, you need the people in that house to sell, and the people above them to sell, and so on. Then there are pensioners downsizing, who also face stamp duty," she said.

"For these people already on the market, who are relying on using the equity in their property to move home and who haven't been saving a deposit for years, large stamp duty bills are a very real hurdle."

Daniel Hegarty, chief executive of online mortgage broker Habito, said: "The biggest challenge for first-time buyers in the UK is still saving for the deposit, and the combined impacts of high inflation, high rental prices and the Bank Rate hike, will make it harder still.

"Would-be home-owners will be grateful for a relief from stamp duty, but it is unlikely to make the dream of home-ownership vastly more achievable for young people."