Yahoo Finance

Yahoo Finance ChatGPT isn’t an Immediate Threat to Alphabet (Nasdaq:GOOGL) - but is Likely to Change the Search Landscape

This article first appeared on Simply Wall St News

OpenAI’s chatbot, ChatGPT, has captured the world’s attention since being released two weeks ago. The chatbot uses OpenAI’s GPT-3 model to answer questions and perform tasks using natural language. The platform gained a million users within five days of its launch, no doubt aided by users sharing their interactions with the chatbot on social media platforms.

While not without its flaws, the chatbot can provide detailed and nuanced answers to surprisingly detailed questions. In many cases, it does a better job than Google search, by providing a single, detailed answer to questions.

The obvious question then is whether it’s a threat to Alphabet’s ( Nasdaq: GOOGL ) primary business.

The Business Model

ChatGPT is optimized to provide answers. On the other hand, Google is optimized to earn ad revenue while providing a list of potential answers in the form of web pages and ads.

Google search is one of the most profitable businesses in the world. At present, ChatGPT is a beta version of whatever it may become. It uses massive amounts of computing power, which is expensive, and there is no business model or revenue at present. OpenAI’s models are available to developers via API, but the chatbot which is the ‘retail’ version is free to use, and therefore a cost center for OpenAI.

Search Types

When someone uses Google search, the information they are looking for could be divided into two categories: informational or commercial. An informational search would be for something like a historical, geographical, or scientific fact, or for academic research. Most of these types of searches probably aren’t monetized by Google.

A commercial search would be for a product or service - a nearby restaurant, airline tickets, car tires, or something like that. These searches are obviously of economic value to Google because they can place ads within the results.

ChatGPT is more useful for informational searches. So while it does compete directly with Google search, it doesn’t compete as effectively with the more profitable types of searches. ChatGPT is also useful for other types of tasks - copywriting, summarizing text, and writing code - but those services don’t compete with Google search either.

Knowledge workers like journalists, analysts, and programmers who get a lot of value out of a tool like ChatGPT may be prepared to pay for it - either for a monthly fee or on a per-use basis. But that would be a relatively small group for Google to lose - and much of their search activity probably isn't profitable anyway.

Google already has its own AI models. Maybe they are better than OpenAI’s, maybe not, but they are probably quite good at searching for information. Until now, Google has had little incentive to make them available to the public because they would cannibalize search traffic. But that could change if an external chatbot becomes a threat to Google.

The Microsoft Threat

Microsoft ( Nasdaq: MSFT ) is very closely aligned with OpenAI. In 2019 Microsoft invested $1 billion in the venture and seems set to invest more going forward. OpenAI’s models run on Azure, and Azure makes those models available to its clients.

So, it’s quite possible that Microsoft will combine OpenAI models with its Bing search engine. That could lure some users away from Google’s search engine. Of course, Google could do something similar with its own AI models. Even if it wasn’t quite as good as a Bing/OpenAI product, it might be good enough to keep users on board - habits are hard to break.

Is Alphabet’s margin of safety wide enough?

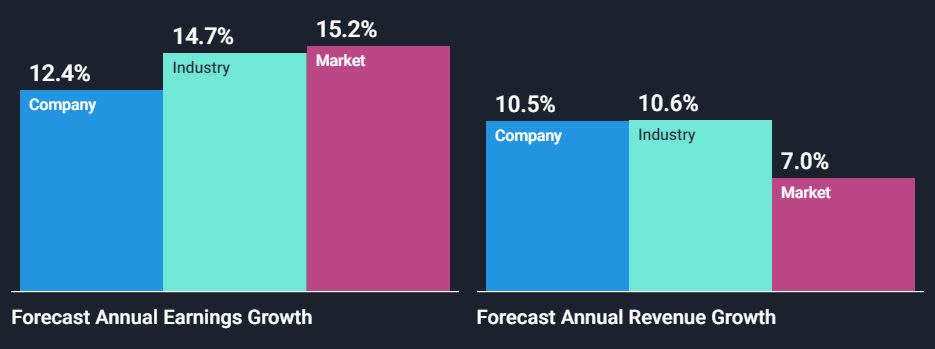

Analyst estimates for Alphabet’s EPS have fallen sharply over the last 12 months. Even EPS forecasts for 2027 are 30% below where they were in January. The current trajectory is for EPS to grow by 12% for the next five years, with revenue growing at 10%. We would say those estimates are fairly conservative.

The Simply Wall Street DCF model estimates Alphabet’s value at $168 using those growth projections. That implies a 46% discount at the current price of $90. In other words, there is a modest margin of safety.

The other five value metrics we track also suggest the stock price is reasonable - but not dirt cheap.

The Bottom Line

The threat Google faces from OpenAI may be smaller than it appears at first glance. And, Alphabet’s current valuation means there is a modest margin of safety.

Of course, there are other ways Alphabet could surprise to the upside. The company has a large portfolio of other companies that could become more profitable, and some could be spun off too. Alphabet also has a lot of space to cut costs - the current cost of sales is $123 bln and Opex is $79 bln. The company has no shortage of options.

One thing is likely though - information search is about to change for consumers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here