Yahoo Finance

Yahoo Finance Some Confidence Is Lacking In Philip Morris International Inc.'s (NYSE:PM) P/E

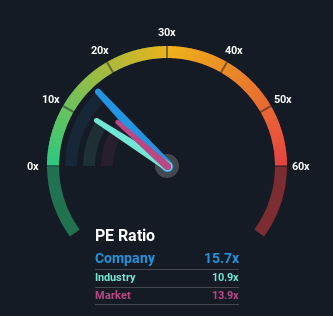

There wouldn't be many who think Philip Morris International Inc.'s (NYSE:PM) price-to-earnings (or "P/E") ratio of 15.7x is worth a mention when the median P/E in the United States is similar at about 14x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

Philip Morris International could be doing better as it's been growing earnings less than most other companies lately. One possibility is that the P/E is moderate because investors think this lacklustre earnings performance will turn around. If not, then existing shareholders may be a little nervous about the viability of the share price.

Check out our latest analysis for Philip Morris International

Keen to find out how analysts think Philip Morris International's future stacks up against the industry? In that case, our free report is a great place to start.

Is There Some Growth For Philip Morris International?

In order to justify its P/E ratio, Philip Morris International would need to produce growth that's similar to the market.

Retrospectively, the last year delivered a decent 2.6% gain to the company's bottom line. The latest three year period has also seen a 16% overall rise in EPS, aided somewhat by its short-term performance. Therefore, it's fair to say the earnings growth recently has been respectable for the company.

Turning to the outlook, the next three years should generate growth of 3.5% per annum as estimated by the analysts watching the company. That's shaping up to be materially lower than the 9.6% each year growth forecast for the broader market.

With this information, we find it interesting that Philip Morris International is trading at a fairly similar P/E to the market. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Final Word

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Philip Morris International's analyst forecasts revealed that its inferior earnings outlook isn't impacting its P/E as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the moderate P/E lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Having said that, be aware Philip Morris International is showing 1 warning sign in our investment analysis, you should know about.

You might be able to find a better investment than Philip Morris International. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a P/E below 20x (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here