Yahoo Finance

Yahoo Finance FTSE suffers biggest daily drop in three months despite UK factory rebound

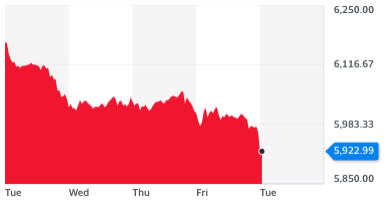

Britain’s FTSE 100 (^FTSE) suffered its biggest daily losses in three months on Tuesday, despite a strong rebound in manufacturing in the UK and beyond.

Many of Europe’s biggest stocks also reversed early gains and continued to lag Wall Street to close lower in a choppy session, despite strong eurozone and Chinese manufacturing data.

The dollar was trading at a two-year low against a basket of currencies on Tuesday, after the Federal Reserve loosened policy to allow greater inflation last week.

Gains for the euro and sterling weigh on European firms that make substantial profits overseas. "The strength in the currency has had an impact on the stocks,” said Naeem Aslam, chief market analyst at AvaTrade.

The pound was trading at its highest against the dollar (GBPUSD=X) since last December, and the euro (EURUSD=X) was trading at its highest in more than two years against the greenback on Tuesday at close to $1.20.

The pan-European STOXX 600 index (^STOXX) had opened 0.3% higher on the first day of the month after its best August since 2009. It came after purchasing managers’ index (PMI) data overnight showed Chinese factories reporting their fastest growth in almost a decade.

But the index was down 0.4% as markets closed in Europe, with travel and leisure stocks down 2.5%. The DAX (^GDAXI) carved out gains of 0.2%, but France’s CAC 40 (^FCHI) also shed 0.2%.

Britain’s FTSE 100 (^FTSE) fell further, losing 2.2% as trade resumed after the long weekend.

Neil Wilson, chief market analyst at Markets.com, noted UK stocks had lagged well behind the recovery in global and US stocks in recent months. A rising pound despite Brexit concerns has “crippled earnings expectations and therefore share price appreciation in the big foreign earners,” with companies like Shell, HSBC and Unilever reliant on global income.

He also claimed the index of Britain’s biggest 100 listed firms was “full of rather lumbering old-world stocks with precious little growth to offer,” with dividends widely slashed and far fewer popular tech stocks than economies like the US.

The declines in Europe came in spite of strong manufacturing data, which had first sent Chinese stocks higher overnight. Shanghai’s SSE Composite Index (^SSEC) closed up 0.3% after purchasing managers’ index (PMI) data for manufacturers came in at its highest since 2011 in August.

The headline figure on the index rose to 53.1, beating expectations, while exports rose for the first time this year. Figures above 50 show growth.

PMI data for the eurozone then showed EU manufacturers also continued to expand in August. The PMI headline figure for factories in the eurozone came in at 51.7 for last month.

Output and new orders both rose at “marked” rates and led manufacturers to a second month in a row of expansion, according to the data company. Output was at a two-year high, with Germany, Italy and Ireland showing the biggest increases.

UK data showed activity in British factories rose at its fastest pace since 2014.

READ MORE: Gradual drop in German firms on short-time work scheme

But the latest eurozone data marked a slight weakening in the pace of growth, with the headline figure down from the 51.8 recorded in July. Manufacturing performance stagnated in Spain and France, and declined in Greece. Job losses also accelerated in Germany, France, Spain and Austria.

Germany also revised down its 2021 GDP forecasts on Tuesday, and EU data showed inflation going into reverse at -0.2% in August, the first negative reading since 2016.