Yahoo Finance

Yahoo Finance Did Business Growth Power Oxford Biomedica's (LON:OXB) Share Price Gain of 107%?

The worst result, after buying shares in a company (assuming no leverage), would be if you lose all the money you put in. But in contrast you can make much more than 100% if the company does well. To wit, the Oxford Biomedica plc (LON:OXB) share price has flown 107% in the last three years. That sort of return is as solid as granite. It's down 3.8% in the last seven days.

View our latest analysis for Oxford Biomedica

Oxford Biomedica isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

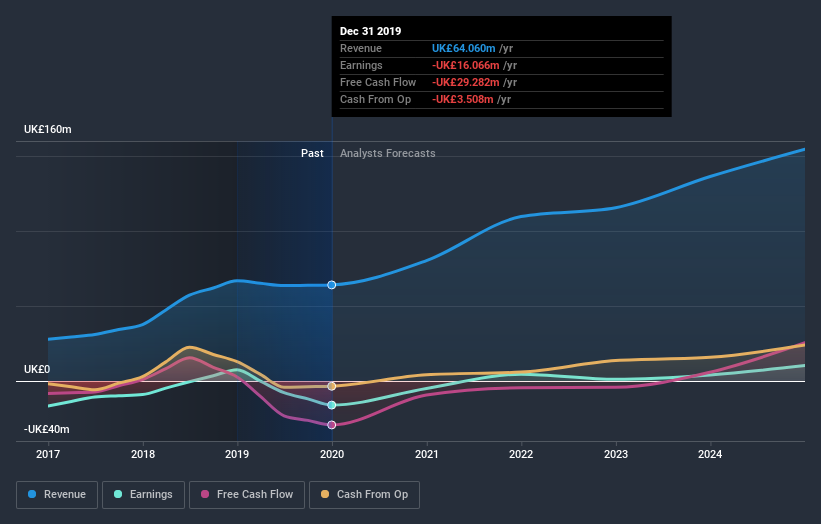

Over the last three years Oxford Biomedica has grown its revenue at 30% annually. That's well above most pre-profit companies. Along the way, the share price gained 27% per year, a solid pop by our standards. But it does seem like the market is paying attention to strong revenue growth. Nonetheless, we'd say Oxford Biomedica is still worth investigating - successful businesses can often keep growing for long periods.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

We like that insiders have been buying shares in the last twelve months. Even so, future earnings will be far more important to whether current shareholders make money. So it makes a lot of sense to check out what analysts think Oxford Biomedica will earn in the future (free profit forecasts).

A Different Perspective

It's nice to see that Oxford Biomedica shareholders have received a total shareholder return of 51% over the last year. That's better than the annualised return of 14% over half a decade, implying that the company is doing better recently. Given the share price momentum remains strong, it might be worth taking a closer look at the stock, lest you miss an opportunity. It's always interesting to track share price performance over the longer term. But to understand Oxford Biomedica better, we need to consider many other factors. Consider risks, for instance. Every company has them, and we've spotted 1 warning sign for Oxford Biomedica you should know about.

Oxford Biomedica is not the only stock insiders are buying. So take a peek at this free list of growing companies with insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on GB exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.