Yahoo Finance

Yahoo Finance ‘I earn £105k but rely on cash-in-hand jobs to make ends meet’

A six-figure salary once meant financial freedom and a desirable lifestyle. But even being on such a high salary, in the top 5pc of earners, does not stop many families from living month-to-month, unable to save or even feel comfortable.

Last month the Chancellor Jeremy Hunt suggested that an annual income of £100,000 “doesn’t go as far as you think”. When one person’s salary crosses that key threshold, you fall into a tax trap. This particularly affects families: eligibility for the 30 hours of free childcare scheme is removed and access to £2,000 a year of tax-free childcare is denied. On top of this, the personal allowance begins to taper away.

We spoke to four people in households pulling in over £100,000 to understand why they no longer feel wealthy. They told us how crippling mortgages and rents, unprecedented taxation, sky-high house prices, substantial childcare costs, soaring utilities and food inflation had left them cutting back on holidays, meals out and luxuries, leaving them feeling not only not rich but, in some cases, like they’re just getting by.

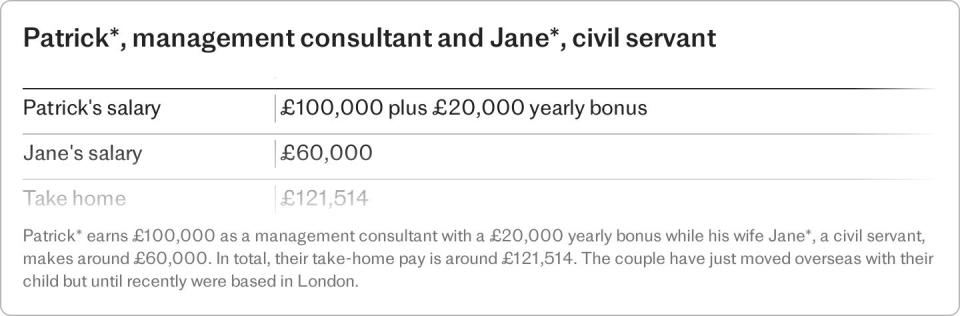

Patrick says:

To get a job that pays six figures in the UK, you need to be in the South East. People with my job title in Newcastle are paid two thirds what I get paid. But it’s a deal with the devil getting that salary in London. Your living costs will be so high that you won’t feel the extra money.

We live in an ex-council flat in a very nice location. The houses on our street are £1.5m to £2m and our flat was £390,000. For us to move into a better home so we can have a larger family, I would need to save large amounts of cash. I am self-made so I don’t have family money behind me. I am stacking away £1,500 a month which obviously affects our lifestyle. We have the same holidays we had £50,000 ago. We might go on holiday once a year to somewhere like Portugal, and we’ll stay in a Hilton. We might do a tasting menu in central London once every three months.

We didn’t have a wedding. We just got married and had coffee afterwards. We looked at the value of a wedding compared to the cost and it was unjustifiable with a baby on the way.

We remortgaged our home last year and the payments have gone up by £500 a month. The food bill has gone up, the utility bills have gone up by huge amounts. About £3,500 out of my £5,000 a month salary is going on mortgage and bills. These increased costs are eroding the money we can save and putting off the moment we can move into a spacious family home. In turn, that makes our desired second child, who we have not yet conceived, less realistic.

Recommended

Can you afford to have children? Use our child cost calculator to find out

My wife is a senior civil servant, but her monthly take-home pay is a few hundred pounds after childcare is paid for, which means all of the saving for the future, the food and the monthly bills, comes out of my salary. It gets harder for us to progress because the more I earn, the less my salary increases because of tax.

We just had our child and I’m very aware that anything I earn over £100,000 means our childcare allowance will be withdrawn. Most of my bonus would disappear because our free childcare allowance is withdrawn, but I’m still taxed on the extra £20,000 of my bonus – so that bonus just cost me £10,000, plus whatever we have lost in childcare support.

For my friends and I who are earning between £100,000 and £150,000, the sense of progression is gone. Tons of babies have been put off or cancelled. I have friends who are freezing their eggs because they can afford the monthly costs of frozen eggs more easily than they can afford a baby.

Friends who are earning six figures, and don’t have generational wealth, are doing stuff you would never expect someone on six figures to be doing. For example, I know married couples earning over £100,000 who are living with flatmates.

I would have thought recreational travel would be a big part of my life when I reached a six-figure salary. Now overseas vacations make me think: how many years is this going to add to moving to the forever home? What does this mean for the size of my children’s bedrooms? That’s a heavy thought.

My industry has had three waves of layoffs and it is not finished. I think it will be pretty tough just to reproduce the circumstances that led to my own success for my son. The idea that I could replicate those circumstances for two or three children doesn’t feel realistic. I don’t feel rich. There was a brief period during Covid where I was getting promotions, we had so much money coming in and we were able to buy a home in west London. I felt I was on my way. Now I just want to keep my job.

June said:

After tax, Daniel brings in £4,100 a month. After paying our mortgage and our bills, we are on the line. We’re not living month-to-month or day-to-day, we’re living hour-to-hour.

Our mortgage is £2,200 a month. Daniel also has to pay child maintenance support of £1,200 a month to his ex-wife. Our gas and electricity bill is £400. The price of petrol is wild and for both of us that’s about £150 a month. I have a nanny on a Tuesday for £10 an hour – which is cheaper than the local nursery – but that still leaves me in the red because I don’t get paid enough to cover childcare. The water has gone up to £200 a month and our council tax has risen too.

Daniel does bar work on the side and we live off of the cash-in-hand that brings in. He worked at one posh function and one of his boss’s friends was there and recognised him. On Monday morning, he got called in to his boss’s office and he had to admit he was really struggling. The boss said: “You get paid £100,000 a year, how are you struggling?”

We don’t go out, there are no luxuries, no holidays. The bills and the mortgage are paid and then there’s nothing. I can’t remember the last time we went on holiday, out for dinner or just had a drink in the pub. We’re not victims but it would be nice to have some extra money which is ridiculous because, on paper, we earn a lot of money. I’d like not to have holes in my knickers and I’d like my husband to be able to pay the £16 a month for his football subs.

Recommended

How rich am I?

We have had to use food banks. The first time was in March 2022 when I was pregnant, and the midwife suggested it. At the time, Daniel had to pay £2,000 a month in child maintenance payments and I was paying off a loan that I had to take out when my business collapsed during Covid. Daniel’s salary at the time had shrunk because it was commission-based, no one was buying anything and his basic salary was only about £40,000. I really don’t know how we would have survived without the food banks. As I’m a teacher and I didn’t want to be recognised, I went to food banks that were a little further away. It was a really humbling experience. It literally saved us. I don’t know what we would have done without that food.

I hate the stigma around using food banks. I went to one and the press was there and I couldn’t go in. So I went to another one and they just filled up my car. I sat there sobbing. They sorted us out with a month-and-a-half’s worth of groceries. It was amazing. My whole mantra is that people should be able to ask for help, but it’s sometimes utterly impossible because on the surface my husband makes great money. We should be fine. But our monthly expenditure wipes us out.

We’ve got a Ukrainian refugee lodger at the moment. It helps our lodger and the £500 a month ‘thank you payment’ really helps us. But I don’t want a stranger living in my house for the rest of my life. As a new mum, it was really difficult. I wanted to be able to walk around with leaky boobs on my own in my own house with my new baby.

We don’t qualify for child benefit which is obscene because we really need it. Our friends who live in a council house diagonal to us go on three holidays a year and have a brand new car. I had far more money as a single mum. I used to have my nails done, my hair done, regular waxes. That’s not even on my radar anymore. My last haircut I won as a prize in a raffle. I was so happy.

I know those are all things that you don’t need – what I need is to put food on the table for my children. That’s what is important. But I do feel that we work really hard, and we are just so squeezed at a time when we really could just do with a little bit of help.

Claudia said:

When I started out on £13,000 a year, this kind of salary was beyond my wildest dreams – but it’s not what I thought it would be like. I watch my money a lot and often I think, “no, I’m not going to buy that” or “I’m not going to do that” because it’s too expensive.

I buy whatever I like in the supermarket but that supermarket is Aldi. I buy my clothes second hand on Vinted. This year we are going to go to Spain to stay for free with friends who live there; I would have preferred to go to a villa in Greece, but we can’t afford the accommodation. We can just about afford flights and spending money.

I feel guilty when I spend money. If I have an unplanned night out and spend £50 on drinks and £22 on an Uber, the next morning I’ll think: “I shouldn’t have done that”.

My partner and I go to gigs, have weekends away in the UK and meals out, but we are probably only going out on average one or two nights a week. I don’t feel the financial insecurity I experienced at the beginning of my career, but I would have thought that someone on this salary would feel rich and that’s just not the case. I know there are people in far worse positions than me but I don’t feel like I have loads of disposable income.

Half of my £3,800 a month take-home pay goes on bills. My mortgage on a two-bedroom home is £1,100 a month. I took a loan out for home improvements when I bought my home and I pay £300 a month for that. The electricity and gas has gone up to nearly £200 a month. My council tax has gone up to £1,350 a year. We spend between £400 and £500 a month on groceries. We run two cars because we both need to drive for our jobs. The car insurance has just doubled and my house insurance has gone up too. We don’t split everything half-and-half because I earn more and bought the house, so I pay most of the mortgage. But if James hadn’t moved in with me, I would have struggled to afford to run a household on my own. I only save £150 a month.

I always dip into my overdraft at the end of the month. As the bills have gone up, I’ve cut back. I used to have Aesop hand wash in the bathroom and I would spend money on luxury skincare; now I buy Carex handwash instead. I don’t buy designer clothes and I don’t go on luxury holidays. I really don’t think I live an extravagant lifestyle.

It feels like every year the bills go up and life becomes more expensive, and I’m becoming less financially secure. All my friends – even the ones who earn great salaries – are constantly broke. One friend makes a decent amount and her husband is a banker on six figures, but they have two children and she says they are skint. It doesn’t feel like anyone is carefree or wealthy right now.

I was on the fence about having kids but James doesn’t want them. Even though it wasn’t my decision, I’m really glad we are not going to have them because I don’t know how we would afford them. My friends tell me about sky-high nursery fees. We’d need a bigger house with a bigger mortgage. I’m sure we could make do, I know people on lower salaries manage to have children, but we would have to make a lot of sacrifices to our lifestyle and I don’t want to do that.

I worry about the future because the industry I work in is quite precarious. If I lost my job, my outgoings are about £2,000 a month. I had savings before but I put them all into buying my house and now I have just a few hundred pounds. I have lost sleep over the fear that I could lose my job. The stakes are much higher now. I’d lose everything if I lost my job.

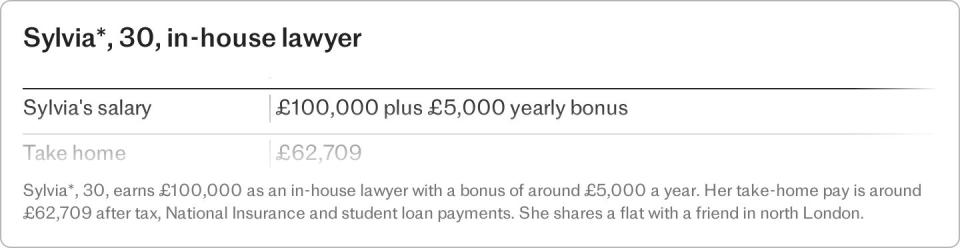

Sylvia said:

I’m from a middle-class background in Manchester and I’m earning more than either of my parents earned, but I don’t have the quality of life that they had at my age.

I share a two-bedroom flat with a friend, spending £1,500 a month on rent and bills. I couldn’t afford to rent on my own anywhere I’d want to live in London. Anywhere I could afford to buy would either be so small that it wouldn’t feel worth it, or so far out that I’d feel isolated. My housing situation feels precarious because I live with my last single female friend. If her situation changes and she wants to move out, I’m either 30-plus living with a stranger or trying to buy somewhere but not feeling able to afford it.

At the moment, I’m saving £800 to £1,000 a month, but I do dip into that pot when I go on trips. I have about £50,000 saved which could be a deposit, but the mortgage would be crippling.

I nearly bought somewhere 18 months ago. It was a very small flat on a commercial high street and the mortgage was going to be £2,100 before bills. In hindsight I’m so glad that I didn’t go ahead because it was an insane amount of money for such a small flat, and I wouldn’t have been able to save anything.

I am fairly left leaning and I believe we should all be paying tax in accordance with what we earn. I earn a lot more than quite a few of my friends and it’s right that I’m being taxed more. But tax, National Insurance and my student loan payments account for half of my salary.

My biggest gripe is my student loan. I was in the first year of students paying £9,000 a year student loans. We were told by the Government that they were low interest loans and worth taking out. We lost my dad when I was quite young and there wasn’t a steady income to pay for me, so I took out a full maintenance loan too. I have been paying my £45,000 loan back on an interest rate of 6-7pc.

In the first few years of my law career, where I was earning considerably more than most of my friends, I wasn’t even chipping into the actual debt, I was just paying interest. At the end of my two-year legal training contract, my student loan had gone up, not down. I’m paying back 9pc of everything I earn on my student loan. There are people on my team who went to university two years before me, who are essentially being paid – after tax – £500 more a month than me because they don’t have a student loan. That feels unfair.

Everything’s gone up. Water, council tax, electricity, the whole lot. But rent increases have been the most noticeable. I used to pay £920 a month plus bills but the landlord said he couldn’t afford his mortgage anymore, so he sold the flat and we had to find somewhere else. Now I pay far more for a property of the same quality. I used to have a car on a lease but after Covid it got more expensive. With the cost plus the permits and the fines you get in London, it wasn’t worth it.

I wonder whether I should go back to Manchester. I could buy a house with a garden in a good area for £250,000 to £350,000, and here I’m struggling to find a one-bedroom for £450,000. It’s something I think about quite a lot but I don’t want to do it.

I’m lucky to be in a profession where I don’t think I’ll be out of work. But when I picture where I might be living long term, I don’t picture myself as happy.

The ‘tax’ on being single is crazy. If I met someone who earned around the same as me, I think I’d have security and a decent quality of life. You would think if you were earning £100,000, working at one of the best in-house teams in the City and pretty good at your job, you would be able to live where you want to live and have a decent quality of life. But I feel like, unless I meet someone, I’m not going to have that.

*All names have been changed.