Yahoo Finance

Yahoo Finance If You Like EPS Growth Then Check Out Industria de Diseño Textil (BME:ITX) Before It's Too Late

It's only natural that many investors, especially those who are new to the game, prefer to buy shares in 'sexy' stocks with a good story, even if those businesses lose money. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses.

In the age of tech-stock blue-sky investing, my choice may seem old fashioned; I still prefer profitable companies like Industria de Diseño Textil (BME:ITX). While that doesn't make the shares worth buying at any price, you can't deny that successful capitalism requires profit, eventually. In comparison, loss making companies act like a sponge for capital - but unlike such a sponge they do not always produce something when squeezed.

See our latest analysis for Industria de Diseño Textil

How Fast Is Industria de Diseño Textil Growing?

If you believe that markets are even vaguely efficient, then over the long term you'd expect a company's share price to follow its earnings per share (EPS). It's no surprise, then, that I like to invest in companies with EPS growth. Industria de Diseño Textil managed to grow EPS by 6.5% per year, over three years. While that sort of growth rate isn't amazing, it does show the business is growing.

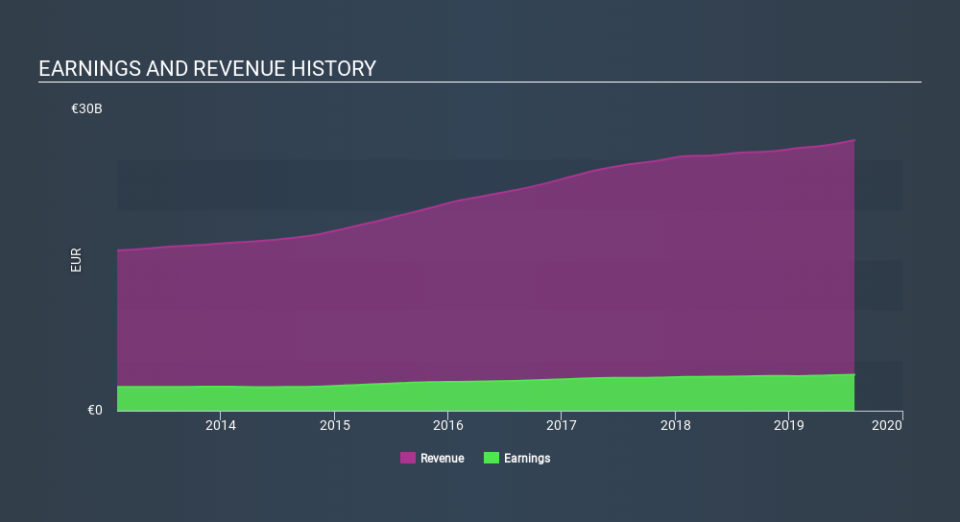

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). Industria de Diseño Textil maintained stable EBIT margins over the last year, all while growing revenue 4.9% to €27b. That's a real positive.

In the chart below, you can see how the company has grown earnings, and revenue, over time. For finer detail, click on the image.

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for Industria de Diseño Textil's future profits.

Are Industria de Diseño Textil Insiders Aligned With All Shareholders?

Like standing at the lookout, surveying the horizon at sunrise, insider buying, for some investors, sparks joy. Because oftentimes, the purchase of stock is a sign that the buyer views it as undervalued. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

One shining light for Industria de Diseño Textil is the serious outlay one insider has made to buy shares, in the last year. Indeed, Executive Chairman Pablo Isla Álvarez de Tejera has accumulated shares over the last year, paying a total of €1.0m at an average price of about €26.64. It doesn't get much better than that, in terms of large investments from insiders.

The good news, alongside the insider buying, for Industria de Diseño Textil bulls is that insiders (collectively) have a meaningful investment in the stock. Given insiders own a small fortune of shares, currently valued at €62m, they have plenty of motivation to push the business to succeed. This should keep them focused on creating long term value for shareholders.

Is Industria de Diseño Textil Worth Keeping An Eye On?

One important encouraging feature of Industria de Diseño Textil is that it is growing profits. Better yet, insiders are significant shareholders, and have been buying more shares. To me, that all makes it well worth a spot on your watchlist, as well as continuing research. Of course, identifying quality businesses is only half the battle; investors need to know whether the stock is undervalued. So you might want to consider this free discounted cashflow valuation of Industria de Diseño Textil.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Industria de Diseño Textil, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.