Yahoo Finance

Yahoo Finance Exactly what you need to say to get a discount on your insurance and broadband

Much has been said about the pain inflicted on households by successive rises in mortgage payments, rent, energy bills, and the weekly shop.

Less remarked upon have been eye-watering increases in insurance premiums and broadband.

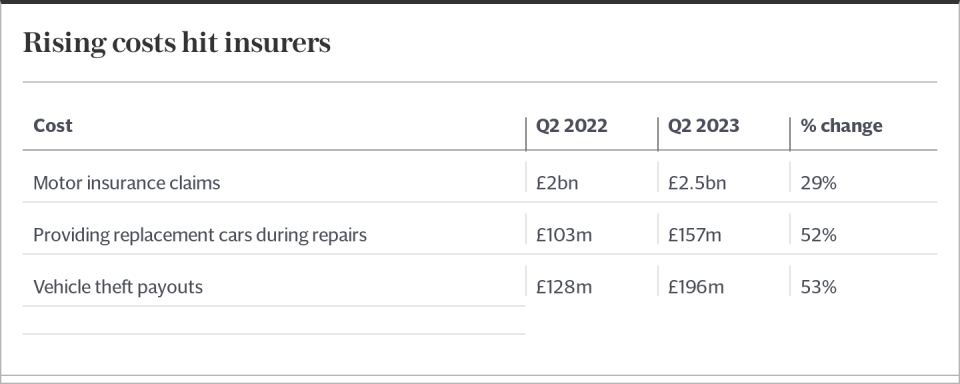

The former has been particularly egregious: car cover premiums soared by 40pc – or £222 on average – from June 2022 to June 2023, according to comparison site Confused.com.

And yet, in 2022, the Financial Conduct Authority banned service providers from enforcing “loyalty penalties”, wherein companies would sneakily and drastically raise fees after a year while simultaneously offering bargain rates to new customers.

It meant households who did not shop around were often ripped off, but this does not mean that your monthly insurance payments cannot go up when the time comes to renew.

Here, Telegraph Money explains your rights, and exactly what you need to do to secure the best rate on your monthly insurance payments.

Why has car insurance increased – and can I haggle it down?

British motorists’ driving habits have fluctuated wildly in the last four years – road accidents fell by 26pc during the pandemic as people drove less. Pre-lockdown driving habits have only recently begun to return to normal.

The gradual return to the roads has meant an increased risk of car accidents, and therefore payouts have become more expensive for insurers.

Inflation has also pushed up the cost of repairs – the Association of British Insurers (ABI) reports the cost of repairing cars rose by a third in the first half of the year.

Whether this necessarily justifies a 40pc rise in premiums is hotly contested. Experts and MPs alike have hinted that there are issues with insurers’ risk models and that some firms are taking advantage of a high-inflation environment to raise premiums beyond what is necessary.

All of this means your car insurance is likely to go up when you come to renew it – almost two in three drivers reported a rise in premiums at renewal in the first half of 2023, according to Confused.com. However, 46pc of those who looked for an alternative found they were able to save money.

Similarly, getting on the phone with your insurer to discuss price increases has also been known to work. Consumer group Which? found that roughly half of insurance customers who contacted their insurer directly to dispute price rises were able to negotiate a lower rate.

Service providers of all kinds have retention departments specifically geared toward stopping existing customers from taking their money elsewhere. These are the people you want to speak to.

Mention any cheaper rates you have been offered elsewhere, and don’t be shy about playing the loyalty card if you have been a customer for many years.

How do I actually haggle?

British people do not like talking about money – and our experience of bartering for a fair price tends to be limited to foreign markets where we are still routinely ripped off. But when it comes to negotiating a fair insurance deal, being bold is the best way to get a result.

Martyn James, the consumer expert, recommended putting the date of your insurance renewal in your diary. “It’s generally considered that negotiating three-to-four weeks before the renewal date is when you get the best-discounted price,” he said.

“The closer you get to the date, the more expensive it is.”

Some policies will contain add-ons that are unnecessary for your situation such as legal insurance, so Mr James advised “cutting the fat” and asking for them to be removed.

“Take time on the application. Price up the value of the goods in your home, for example,” he said. “Many people find that they are actually over-insuring because the value of some items has decreased the longer they have had them.

“It’s worthwhile getting detailed on things like repairs to the structure of a building or roof, for example, or exactly when your car passed its MOT.”

But what about going above the heads of customer service teams and straight to the CEO? Sadly, this is unlikely to work, said Mr James.

“Threatening to go to make a complaint to the CEO used to make a difference to businesses in the past,” he explained. “But bear in mind that the person you are speaking to might know full well that you aren’t going to get anywhere near their office these days.”

Instead, Mr James recommended going through the specific renewal line, not the helpline.

“Tell them you have much better offers elsewhere and you want to see if they can improve or match them, or you’ll leave,” he said.

Threatening to contact “head office” is more effective when lodging a complaint, however. Mr James said: “A formal complaint must be logged and details of how they are dealt with go to the regulator.

“You will make more progress if you make it clear you will take the case to the Financial Ombudsman if not happy, which charges businesses a case fee if they take on the case.”

What about my home insurance?

Home insurance premiums reached an all-time high in August this year, rising by more than 26pc in the past year, according to Pearson Ham, the pricing consultancy.

As with cars, insurance firms claim the cost of repairs has shot up due to inflation pressures.

The rise in premiums from last year can be attributed largely to damage from severe weather – including February’s storms and the record-breaking summer heatwave. The ABI estimated insurers could pay out as much as £212m from claims made in 2022.

That’s all well and good, but for you – a homeowner facing a more expensive premium – what matters is not getting ripped off. Thankfully, the received wisdom for driving down your insurance premium is the same for homes as it is for cars.

Try and get hold of the retentions department, as outlined above. Be sure to shop around and have better value quotes ready to cite. If your insurer fails to match them, you can always vote with your feet.

My broadband is also going up – why? And how do I secure a better deal?

Like any service provider, broadband companies raise their prices every year to cover inflation and business costs. Broadband providers also introduce annual mid-contract price rises.

These are tied to the Consumer Price Index, published in January, which this year was 10.5pc. Broadband companies also tack on an additional 3-4pc, meaning some households were hit with costs of up to 14.5pc more, according to comparison site uSwitch.

But broadband providers can be haggled with, just like home and car insurers. Ernest Doku, uSwitch’s telecoms expert, said: “Many of the best offers are reserved for new customers. So, even if you are happy with your current provider, it is worth seeing what deals are out there to avoid paying a “loyalty tax”.

“If you can see better deals are available elsewhere, tell your current provider you are considering leaving. Suppliers really don’t want to lose customers, so if there is a better deal elsewhere they may be inclined to match it.”

But, he added, customers should be wary that they are eligible to switch without paying any early termination fees. It’s a good idea to check your policy details or contact your provider to find out whether you are out of contract and can switch providers for free.

“For broadband customers, deals can vary by location, so the best approach is using your postcode to search and compare deals in your area,” Mr Doku said. “You can save up to £174 by switching broadband providers, and many providers offer additional incentives to new customers, such as bill credit or vouchers.

“Look out for new broadband providers moving into your local area. Those local flyers through your door promising fast speeds and better reliability – don’t just throw them away.”

Threatening to leave can also set the cat among the pigeons in retention teams – and broadband providers have been known to ape the techniques of subscription services by offering hitherto undiscovered discounts.

Some streaming services are also known to use analytics data to preemptively offer discounts to customers who they think are likely to cancel, according to Stephen Hateley, head of product and partner marketing at DigitalRoute, which works with several global streaming services.

“Subscription fatigue has also arisen as a result of over-subscription during the pandemic – this includes music and video but also meal prep, beauty boxes, and alcohol,” he said.

“Consumers are increasingly realising that they don’t need these recurring services anymore or are cutting their outgoings.”

Amanda Mesler, chairman and CEO at Minna Technologies, the subscriptions management fintech firm, said: “In the subscription economy, value and flexibility outweigh cost.”

A survey by the company showed nine in ten consumers would rather accept an offer on their subscription than cancel, eight in 10 would rather upgrade or downgrade than cancel and seven in ten would rather pause than cancel.

Ms Mesler said: “By giving customers personalised incentives and packages, businesses can re-engage inactive subscribers to mitigate churn and encourage them to upgrade.”

In short, even if you are not a disaffected customer, telling a service provider that you are can net you some incredible value.

Recommended

Terrible internet? Here’s how to get the broadband speed you were promised