Yahoo Finance

Yahoo Finance What to Expect from Dillard's (DDS) Q3 Earnings

Dillard’s DDS third quarter earnings on November 9 will be significant and insightful into the effects an economic downturn is having on the economy. Dillard’s along with big retailers like Walmart WMT and Target TGT which are set to report next week will show the magnitude that slower consumer spending is having economically.

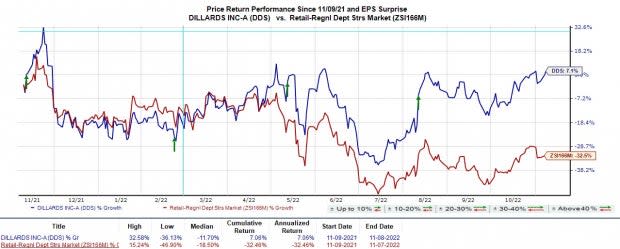

With that being said, many investors are still expecting big things out of DDS earnings. Along with its fashion apparel and home furnishing department chains that coincide with its website the company also owns a real estate investment trust (REIT) and a wholly owned captive insurance company. This diversification helps manage risks more efficiently and improve liquidity which has contributed to the stock holding up far better than the broader market and most retail and regional department stores.

Image Source: Zacks Investment Research

DDS Growth

Dillard’s growth has been remarkable, and the company has now become immensely profitable after maintaining operation and expansion costs which are largely credited to its REIT and wholly-owned insurance company. The company’s earnings have grown significantly since the pandemic and investors are hoping Dillard’s will be able to fight off the current economic downturn.

Image Source: Zacks Investment Research

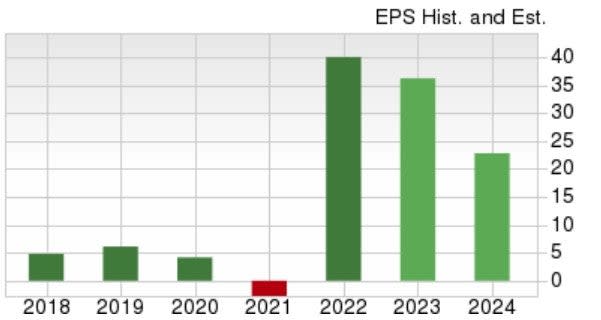

Over the last five years, Dillard’s has seen a 47% growth rate, which is well above the industry average of 23%, and the S&P 500’s 13%. DDS’s Q3 earnings will be essential in sustaining another solid year in earnings after its impressive fiscal year 2022 which saw EPS at $40.05 and revenue of $6.49 billion.

Q3 Outlook

The Zacks Consensus Estimate for Dillard’s Q3 earnings is $4.87 per share, which would be a decline of -50% from $9.81 in Q3 last year. Sales for Q3 are expected to be virtually flat at $1.49 billion. This is an indication that operation costs are weighing on DDS’s bottom line despite a tough to compete with prior-year quarter.

However, earnings estimates have largely gone up from $3.18 at the beginning of the quarter. Year over year, DDS earnings are expected to decline -9% in fiscal 2023 and drop another -37% in FY24 at $22.83 per share. It is important to note that annual earnings estimates have also trended significantly higher throughout the quarter. Sales are projected to be up 5% in fiscal 2023 and remain roughly flat in FY24 at $6.79 billion.

Earnings estimate revisions trending higher is a good sign that the company may also beat earnings expectations as well. Last quarter the company blasted earnings expectations by 223% at $9.30 per share compared to the Zacks Consensus of $2.88 per share. DDS has now beaten earnings expectations for 9 consecutive quarters.

Performance & Valuation

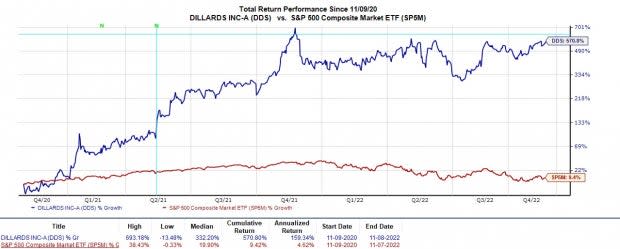

Year to date DDS is up +35% to crush the S&P 500’s -21%. This has also blasted the Retail-Regional Department Stores Markets -18%. Dillard’s performance has been stellar as it continued to cement itself as a retail leader over the last two years up an impressive +571% when including its dividend, this largely beat the benchmark and its Zacks Subindustry’s +133%.

Image Source: Zacks Investment Research

Despite the stellar run, DDS has remained fairly valued considering its exponential growth and massive earnings. Trading around $330 per share, DDS has a forward P/E of 8.9X. This is on par with the industry average. Even better, DDS trades at a discount to its decade-high of 45.8X and is nicely below the median of 12.3X.

Bottom Line

With earnings estimate revisions on the rise, DDS lands a Zacks Rank #2 (Buy). This also makes the possibility of another earnings beat more plausible. Along with stronger than expected Q3 earnings, Wall Street will be looking to see if the company’s guidance and outlook start to reaffirm the trend in rising earnings estimates.

Despite near-term headwinds associated with a fading economy, DDS’s Retail -Regional Department Stores Industry is in the top 15% of over 250 Zacks Industries with the approaching holiday season expected to still give retailers a boost. DDS also has an overall “A” VGM grade and offers investors a modest 0.25% annual dividend yield at $0.80 per share.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dillard's, Inc. (DDS) : Free Stock Analysis Report

Target Corporation (TGT) : Free Stock Analysis Report

Walmart Inc. (WMT) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research