Yahoo Finance

Yahoo Finance The four biggest pension mistakes you can make – and how to avoid them

We all dream of living comfortably in retirement, but making this a reality is far from easy.

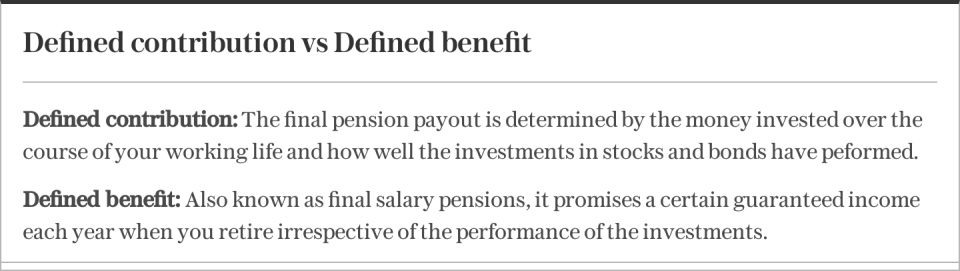

While your parents or grandparents may have enjoyed a defined benefit (DB) pension – guaranteeing them an income for the rest of their life – today, the vast majority of us will need to think much more carefully about how we save into, manage and access our retirement income.

Failing to save enough, or making poor drawdown choices are just a couple of ways you could find yourself running out of money.

Here, Telegraph Money outlines the biggest mistakes you can make with your pension, and how to avoid them.

Making the wrong type of withdrawals – and paying too much tax

Since pension freedoms were introduced in 2015, savers have had a number of different options for drawing down their pensions.

But the rules are complex, and making the “right” type of withdrawal can be a challenge – especially as the cost of living crisis has forced many to tap into their retirement savings earlier than expected. The amount of money flexibly withdrawn from pensions rose 15pc to £12.9bn in 2022-23.

Having more choice about how and when you can access your pension savings is an advantage for many people, but it requires careful thought and planning. For one thing, by rushing into a pension withdrawal, you risk paying more tax than necessary.

You can access your pension from age 55 (rising to 57 in 2028). If you have a defined contribution (DC) scheme, you can opt for flexible retirement income, where you crystallise your pension in order to take 25pc of your pot tax-free. Subsequent withdrawals will be treated as taxable income.

Kate Smith, of pension firm Aegon, said some savers make the mistake of cashing out their pension all in one go. “People spend years diligently saving in a pension and risk losing the full benefit of this if they withdraw all their pension in one tax year and cross into a higher tax bracket. This could significantly reduce their retirement income after tax is deducted.”

She added: “It would be better to spread any pension withdrawals over a few years to avoid moving into a higher tax band and getting more of your pension in your pocket.”

If you want to access your pension, but you do not want to designate funds for drawdown or buying an annuity just yet, then you can take what is called an “uncrystallised funds pension lump sum” (UFPLS).

This means 25pc of each withdrawal will be tax-free. For example, if you withdrew £5,000 then £1,000 would be tax-free and the remaining £4,000 would be added to your taxable income.

Be careful not to withdraw more than you need, as this could push you into a higher tax bracket, meaning you pay more tax than necessary. A study of over 3,000 savers by the Association of British Insurers (ABI) recently found that 86pc make the wrong decision – i.e. pay too much tax – when taking a UFPLS without detailed guidance.

Once you start taking an income from your pension pot, the Money Purchase Annual Allowance kicks in. This reduces how much you can save into your pension each year without paying tax from £60,000 to just £10,000. This can be very problematic for those who access their pensions while they’re still working, or those who take up a job later in life.

Accessing your pension too early

Just because you can access your pension from age 55, it does not necessarily mean you should.

A saver taking their 25pc lump sum from a £400,000 pension pot will miss out on £24,618 worth of investment returns over the next five years, according to analysis by Aegon.

Resisting the urge to tap into your pot and leaving it untouched for as long as possible will give your money more time to benefit from tax-free growth and compound interest.

If possible, you should also avoid raiding your pension to cover costs in later life. Unlike other parts of your estate, pensions can be passed on free from inheritance tax – so, if your boiler breaks, for example, it would be better to take the money from your savings than your pension.

Not saving enough

It is both boring and painful to hear, but it is true nonetheless: many of us are not saving enough for retirement. Thanks to auto-enrolment, over 20 million employees now participate in a workplace pension, which is an improvement compared to before the rules kicked in – however, a large number pay only the bare minimum into the scheme.

Under auto-enrolment law, your employer must ensure your minimum pension contributions are 8pc – usually split as 3pc from them and 5pc from you. While this is better than nothing, it’s unlikely to be enough to build up enough for a comfortable retirement.

Andy Parker, of consultancy Barnett Waddingham, said: “Many pension scheme members never change from this auto-enrolment level. However, contributing the absolute minimum to your pension is unlikely to be the best approach to ensure you have a healthy pot for retirement.”

According to data from the Department of Work and Pensions, around 54pc of workers save less than 6.5pc of their earnings into their pension.

The Government has come under pressure to increase auto-enrolment contributions or increase the scope to include younger workers below the age of 22, to ensure more people have decent retirement income when it comes to retirement.

There is one thing worse than saving too little – and that is not saving anything at all. Analysis from Barnett Waddingham shows that someone who delays saving into their pension by just five years will be 20pc worse off by the time retirement comes around.

In 2022-23, just under 1pc of employees had chosen to stop saving into their pension, according to the latest data. Young workers are the most likely to decide to opt out of pension contributions – with rising living costs often to blame.

Ms Smith said: “Delaying pension saving can mean a lower retirement income, or having to pay much higher pension contributions in later life. The earlier people start saving in a pension the better. People will not only save longer, but also the earliest pension contributions will be invested longer, and benefit from the magic of compounding, becoming even more valuable.”

Another common mistake savers make is not maximising pension contributions from their employer. Ms Smith said: “Some employer’s match employee’s pension contributions. So if an employee pays more, so does the employer – up to a limit. This is effectively a pay rise.”

Not considering charges

Once you are no longer contributing to a workplace pension, you may wonder if you could get better returns elsewhere. Also, if you’ve worked for a range of employers throughout your career, you could find yourself with a number of different pension pots.

If this is the case, you may want to think about consolidating your pots into a non-workplace scheme. However, be mindful that your workplace pensions may have lower charges, meaning it’s not always worth moving the money.

“Most people invest their workplace pension in default funds which are capped at an annual management charge of 0.75pc, with most charges well below this,” said Ms Smith.

“Non-workplace pensions don’t have a charge cap, so people risk paying more if they transfer their workplace pension to a non-workplace pension scheme.”

The average charge for a workplace pension was 0.48pc in 2022, according to the Pensions and Lifetime Savings Association, whereas non-workplace pension schemes can charge as much as 1pc per year.

Over 15 years, opting for the cheapest Sipp provider could save someone with a £250,000 pot almost £22,000 in fees, according to research by consumer organisation Which?, this could make a big difference when you’re trying to make your money stretch as far as possible.

Recommended

The best and worst years to retire – and how to protect your income