Yahoo Finance

Yahoo Finance G-III Apparel (GIII) Q1 Earnings Beat, Sales Down Y/Y

G-III Apparel Group, Ltd. GIII posted better-than-expected results in first-quarter fiscal 2024, wherein the top and the bottom line beat the Zacks Consensus Estimate. Adjusted earnings of 13 cents per share outpaced the consensus estimate of a loss of 9 cents per share. However, the bottom line compared unfavorably with the year-earlier quarter’s earnings of 72 cents per share.

G-III Apparel’s digital business reported solid growth of more than 20%, mainly backed by building the Amazon business that tripled in the first quarter of last year. Growth with pure-play digital retailers has compensated the traditional digital channels. Further, the platform of the company’s own DKNY and Karl Lagerfeld Paris e-commerce sites are driven by the latest look and feel, updated loyalty programs, expanded CRM capabilities and advanced technical operations. Management has raised the outlook for fiscal 2024.

Impressively, shares of the company have increased 28% during the trading hours on Jun 6. Shares of the company have gained 27.5% outperforming the industry’s 0.4% drop.

Q1 in Detail

Net sales fell 11.9% year over year to $606.6 million but surpassed the Zacks Consensus Estimate of $560 million. Lower sales at the wholesale division, offset by higher sales at the retail unit, aided the overall top line. Net sales for the Wholesale segment were $587 million, down roughly 14% year over year and the metric at the Retail segment was $30 million, up 7.1% from the prior-year quarter’s reported figure.

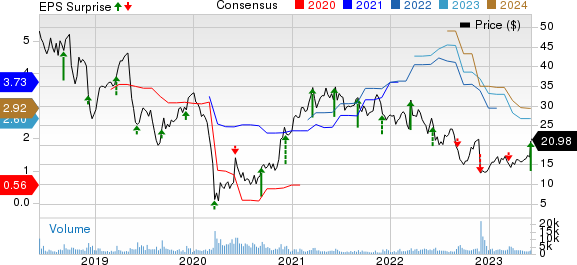

G-III Apparel Group, LTD. Price, Consensus and EPS Surprise

G-III Apparel Group, LTD. price-consensus-eps-surprise-chart | G-III Apparel Group, LTD. Quote

The company’s power brands, DKNY, Karl Lagerfeld, Calvin Klein and Tommy Hilfiger outperformed management’s expectations, led by categories, such as dresses, sportswear and suit separates. Its North American DKNY and Karl Lagerfeld Paris businesses performed well.

Moreover, gross profit jumped 1.5% year over year to $249.8 million. Meanwhile, the gross margin of 41.2% increased 550 basis points (bps), mainly attributed to the lower gross margin at the wholesale unit. The wholesale segment’s gross margin was 39.9%, up 580 bps year over year. The Retail unit’s gross margin was 50.9%, up 1000 bps from the year-ago period on lower inflationary pressures in product and transit expenses.

Selling, general and administrative expenses increased 23% year over year to $228 million. Further, operating expenses came in at $15.3 million in the fiscal first quarter, compared with $54.5 million in the year-earlier quarter.

Other Updates

Management has announced a new licensing agreement for the Halston brand, which is an American heritage brand. The company has entered into a 25-year agreement with Xcel Brands to design and manufacture all categories with the choice to buy the brand at the end of the licensing term. Halston is an American heritage brand with a legacy of glamorous designs across a range of price points First deliveries are likely to be in 2024 fall.

Management is on track with the development of Nautica and Donna Karan brands. For Nautica, the company is working on bringing the Spring 2024 jeans line to life, while for Donna Karan, it is leveraging the brand’s classic, contemporary, and elevated feel and widening its appeal to a broader consumer base.

The company’s strategic priorities include driving power brands across categories, enhancing its portfolio via ownership of brands and licensing opportunities, expanding global reach, maximizing omnichannel capabilities and scaling the private label business. Additionally, the company has seen higher warehousing costs on increased inventory levels and overall inflationary pressures.

Nonetheless, the company has been making progress on rightsizing its inventory. As port congestion and lead times have normalized, management has adjusted the warehouse space appropriately. This trend is likely to continue throughout the year, driven by moderate freight costs.

Other Financial Details

G-III Apparel ended first-quarter fiscal 2024 with cash and cash equivalents of $289.7 million and total debt of $543 million. Total stockholders’ equity was $1,380.4 million.

It ended the fiscal first quarter in a net debt position of roughly $250 million versus $83 million in the prior year. The increase in net debt was buoyed by the $170 million in net cash utilized to complete the Karl Lagerfeld buyout and $44 million for stock repurchases. The company had cash and availability of about $800 million under its revolving credit agreement at the end of the quarter.

This Zacks Rank #3 (Hold) company has returned $17 million to its shareholders via stock repurchases.

Outlook

The fiscal 2024 outlook includes the inflationary pressures on consumers and on the company’s operations, along with incremental costs related to managing increased levels of inventory. Management expects solid cash flows this year as the inventory levels normalize.

For fiscal 2024, management projects net sales of about $3.29 billion and net income between $125 million and $130 million, or between $2.65 per share and $2.75 per share. It reported net sales of $3.23 billion and a net loss of $133.1 million, or $2.79 per share in fiscal 2023.

Management anticipates gross-margin improvement in fiscal 2024, up nearly 350 bps year over year, driven by highly moderated freight costs. SG&A will de-lever on higher warehousing costs related to higher inventory levels and inflationary pressures.

Further, the company predicts adjusted EBITDA between $267 million and $272 million, compared with the adjusted EBITDA of $266.1 million in fiscal 2023. Adjusted net income is anticipated in the range of $132-$137 million, or $2.80-$2.90 per share for the current fiscal year versus net income of $138.8 million, or $2.85 per diluted share in fiscal 2023.

For the fiscal second quarter, management expects net sales of nearly $595 million, compared with $605.2 million in the prior-year quarter. The company forecasts a net loss for the same quarter in the band of $(5.0) million and break even or between $(0.10) per share and $0.00 per share, versus a net income of $36.3 million, or 74 cents per share, in the prior year’s quarter.

The company envisions an adjusted net loss of $3 million and net income of $2 million, or between a loss of 6 cents per share and earnings of 4 cents per share for the fiscal second quarter, versus an adjusted net income of $19 million, or 39 cents per share recorded in the second quarter of fiscal 2023.

Management also focuses on DKNY, Karl Lagerfeld, Donna Karan and Vilebrequin along with the other owned brands. These brands have been performing well and accounted for an aggregate of $1.3 billion in annual net sales last year. Owned brands are likely to generate nearly $1.5 billion in annual net sales this fiscal year.

Eye These Solid Picks

Some top-ranked companies are Royal Caribbean RCL, Crocs CROX and lululemon athletica LULU.

Royal Caribbean sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

RCL has a trailing four-quarter earnings surprise of 26.4%, on average. The Zacks Consensus Estimate for RCL’s 2023 sales and earnings per share (EPS) indicates increases 47.9% and 158.3%, respectively, from the year-ago period’s reported levels.

Crocs, which offers casual lifestyle footwear and accessories, presently carries a Zacks Rank #2 (Buy). The expected EPS growth rate for three to five years is 15%.

The Zacks Consensus Estimate for Crocs’ current financial-year sales and EPS suggests growth of 13.1% and 2.8% from the year-ago period’s reported figure. CROX has a trailing four-quarter earnings surprise of 21.8%, on average.

lululemon athletica is a yoga-inspired athletic apparel company. LULU has a Zacks Rank of 2 at present.

The Zacks Consensus Estimate for lululemon athletica’s current financial-year sales and EPS suggests growth of 16.7% and 18%, respectively, from the year-ago corresponding figures. LULU has a trailing four-quarter earnings surprise of 9.9%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

lululemon athletica inc. (LULU) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report

G-III Apparel Group, LTD. (GIII) : Free Stock Analysis Report