Yahoo Finance

Yahoo Finance G7: Rising Debt Heightens Sovereign Risks Amid Election Uncertainty

Debt-to-GDP ratios of most G7 sovereigns are likely to continue rising. The fiscal rules of many G7 governments – further weakened during the pandemic crisis – are insufficient to curb rising levels of borrowing while current higher interest rates might complicate fiscal consolidation.

Elections in several G7 nations – France, the United Kingdom and the United States for this year – are unlikely to result in post-electoral reversals of their debt trajectories.

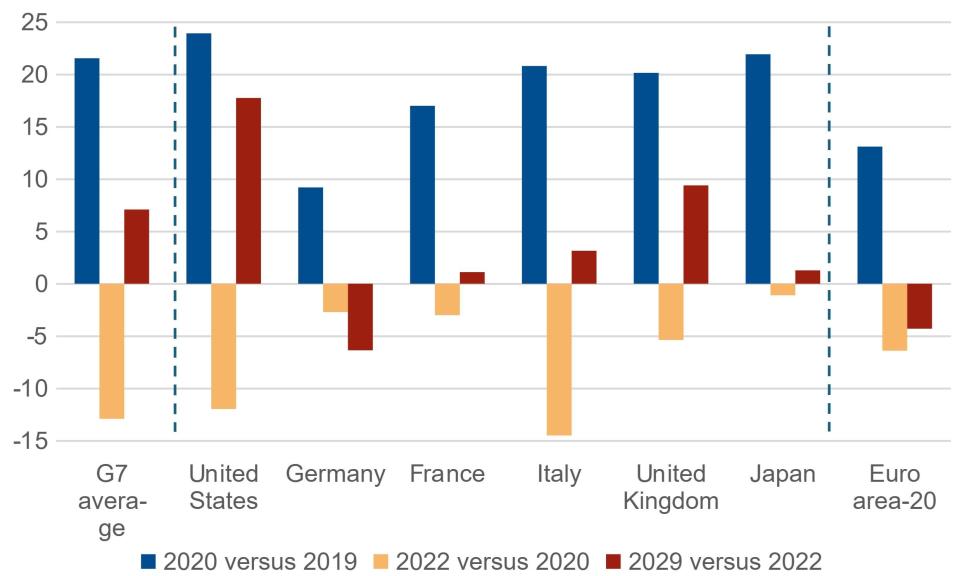

Scope projects G7 general government debt will rise to 135.2% of GDP by 2029, approaching the recent 2020 peak of 139.6% (Figure 1). This increase is driven primarily by the rising debt stock of the United States, the world’s benchmark “risk-free” borrower.

Figure 1: G7 debt ratios declined in 2020-22 but have since increased

Changes in general government debt ratios, pps of GDP

US Has Limited Incentives to Reduce Sovereign Debt

As the issuer of the global safe asset, the US faces few incentives to cut its debt despite warnings from rating agencies and fiscal watchdogs concerning long-run fiscal risks.

The debt ceiling remains the single element within the US fiscal framework with real bite to enforce budgetary rectitude. However, it unfortunately also introduces a risk of technical default every year or two.

Rising French and Italian Debt Trajectories; German Debt Declining

Inside the euro area, French deficits are expected to remain above 3% of GDP through 2029, even before any policy changes after forthcoming second-round legislative elections, which might hinder programmed budgetary consolidation. The rise in French debt, which at this stage is set to increase gradually to 113% of GDP by 2029 from the 110.6% at the end of last year, could make the sovereign vulnerable to further investor unease.

The contagion from France to other euro-area sovereign markets has been modest so far. Nevertheless, Italy displays budgetary risk, having debt forecast to rise to 143.6% of GDP by 2029, from the 137.3% as of end-2023. Germany remains an outlier among the G7, forecast for budget deficits of under 2% of GDP this year and the years ahead alongside declining debt.

UK Debt to Increase; Japan’s Credit Outlook Improves

Meanwhile, the UK is in similar position to that of the US in facing a significant rise in general government debt to 110% of GDP in 2029 from 101% in 2023. Memories of the mini-budget crisis two years before are unlikely on their own to be enough to ensure tight fiscal policy after parliamentary elections.

Scope Ratings recently revised its Outlook of another G7 sovereign state: Japan (rated by Scope A) to Stable, from Negative, as more-durable inflation has supported the public-debt outlook.

The Higher-for-longer Interest Rates Alters Outlook for Debt Sustainability

The outlook of rates to stay higher for longer changes things for sovereigns. Rising debt-to-GDP not only raises questions over long-run debt sustainability but also limits governments’ near-term budgetary headroom. Before the pandemic crisis, the prevalence of ultra-low rates ensured interest payments fell even as governments increased their borrowing. Today, the proportion of government expenditure servicing government debt is rising as older low-cost debt is re-financed at higher rates even without assuming any change in the stock of borrowing.

The G7 economies with rising government debt – such as France, Italy, the UK and the US – need to find ways to reinforce their fiscal frameworks and achieve adequate budgetary consolidation even allowing for the significant institutional advantages they have.

Access the full report from Scope Ratings

For a look at all of today’s economic events, check out our economic calendar.

Make sure you stay up to date with Scope’s ratings and research by signing up to our newsletters across credit, ESG and funds. Click here to register.

This article was originally posted on FX Empire