Yahoo Finance

Yahoo Finance

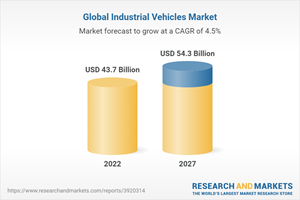

Global Industrial Vehicles Market (2022 to 2027) - Increasing Demand for Battery-Operated Industrial Vehicles Presents Opportunities

Global Industrial Vehicles Market

Dublin, June 14, 2022 (GLOBE NEWSWIRE) -- The "Global Industrial Vehicles Market in terms of Vehicle Type, Drive Type (ICE, Battery-operated, Gas-powered), Application, Capacity, Level of Autonomy, Aerial Work Platform (Boom Lifts, Scissor Lifts) and Region - Forecast to 2027" report has been added to ResearchAndMarkets.com's offering.

The global industrial vehicles market is projected to grow from USD 43.7 billion in 2022 to USD 54.3 billion by 2027, at a CAGR of 4.5%.

Parameters such as increasing growth of e-commerce sector, along with the increasing demand for autonomous solutions in material handling across end-use industries will boost the demand for the industrial vehicles. In addition, the growing adoption of battery-operated industrial vehicles, paired with the advent of smart factories in the manufacturing sector will create new opportunities for this market.

Manufacturing segment is expected to grow at a significant rate during the forecast period, by application

The manufacturing segment of the industrial vehicles market is projected to grow at the noticeable rate during the forecast period. The increasing adoption of industrial vehicles in automotive, chemical, food & beverages, and healthcare, among others, is expected to drive the manufacturing segment of the market during the forecast period.

These vehicles are used in manufacturing processes to store and retrieve inventory for the production line. Benefits such as short downtime, labor cost savings, reduced accidents on the production floor, and increased efficiency and flexibility have been encouraging manufacturers to invest in new product development. These benefits will drive the demand for industrial vehicles during the forecast period.

North America is expected to be the significant market during the forecast period

North America is a hub for various renowned industrial vehicle manufacturers known for delivering quality and high-performance industrial vehicles. Factors such as large e-commerce industry and an established ecosystem for industrial as well as manufacturing companies with their own warehousing capabilities make North America an attractive market for industrial vehicle manufacturers. Moreover, an extensive 3PL network has led to the growth of the warehousing sector in North America. Exhibitions and trade shows such as ProMat and MODEX, which are held annually, also help material handling equipment manufacturers to look for prospective customers in North America.

The North American automotive industry is one of the most advanced in the world; it houses major OEMs such as Ford Motors, Tesla, General Motors, and Fiat-Chrysler. The North American Free Trade Agreement (NAFTA) has fostered the growth of the automotive industry in the region. The US, which has traditionally been a global technological leader, is the largest automotive market in North America.

A large customer base and high disposable income levels in the country have fueled the demand for electric vehicles, resulting in increased manufacturing activities by local automotive OEMs. This, in turn, requires material handling solutions to transport chassis, car bodies, engines, and other components in the automotive manufacturing units in North America. Industrial vehicles are important for handling eccentric-shaped loads, and hence their adoption in this region is growing.

Freight & Logistics segment is estimated to be the second largest market in the industrial vehicles market during the forecast period

Freight & Logistics is expected to be the second largest segment by application during the forecast period. Logistics and freight operations include material handling processes on ports, logistics hubs, and large distribution centers. With the rising intricacy of logistics operations and freight processes, the issue of waiting time and in-travel goods damage is gaining traction in the intralogistics industry. End use industries that have multinational production operations like automotive and electronics have been trying to reduce the loss and damages during logistics processes.

Logistics and freight operations include material handling processes on ports, logistics hubs, and large distribution centers. With the rising intricacy of logistics operations and freight processes, the issue of waiting time and in-travel goods damage is gaining traction in the intralogistics industry. End use industries that have multinational production operations like automotive and electronics have been trying to reduce the loss and damages during logistics processes. All these factors are expected to drive the freight & logistics segment in the Asia Pacific region during the forecast period.

Key Topics Covered:

1 Introduction

2 Research Methodology

3 Executive Summary

4 Premium Insights

4.1 Attractive Opportunities in Industrial Vehicles Market

4.2 Industrial Vehicles Market, by Vehicle Type

4.3 Industrial Vehicles Market, by Drive Type

4.4 Industrial Vehicles Market, by Application

4.5 Aerial Work Platform Market, by Type

4.6 Industrial Vehicles Market Growth Rate, by Region

5 Market Overview

5.1 Introduction

5.2 Market Dynamics

5.2.1 Drivers

5.2.1.1 Growing E-Commerce and Warehousing

5.2.1.2 Technological Advancements Aimed at Increasing Productivity

5.2.1.3 Increasing Demand for Automation Solutions in Material Handling Across Industries

5.2.1.4 Rising Focus on Improving Workplace Safety

5.2.2 Restraints

5.2.2.1 High Cost of Automation

5.2.2.2 Lack of R&D Facilities and High Maintenance of Industrial Vehicles

5.2.3 Opportunities

5.2.3.1 Increasing Demand for Battery-Operated Industrial Vehicles

5.2.3.2 Advent of Smart Factories in Material Handling Industry

5.2.4 Challenges

5.2.4.1 Government Regulations and Safety Concerns

5.2.4.2 Low Labor Costs Restrict Adoption of Industrial Vehicles in Emerging Economies

5.3 Trends & Disruptions Impacting the Market

5.4 Industrial Vehicles Market Scenarios (2022-2027)

5.4.1 Most Likely Scenario

5.4.2 Optimistic Scenario

5.4.3 Pessimistic Scenario

5.5 Porter's Five Forces

5.6 Industrial Vehicles Market Ecosystem

5.7 Value Chain Analysis

5.8 Pricing Analysis

5.9 Key Stakeholders & Buying Criteria

5.9.1 Key Stakeholders in Buying Process

5.9.2 Buying Criteria

5.10 Macroeconomic Indicators

5.10.1 Gdp Trends and Forecast for Major Economies

5.10.2 World Motor Vehicle Production Statistics in 2020 & 2021

5.11 Patent Analysis

5.12 Case Study

5.12.1 Thyssenkrupp's Decision for Flexible Automation

5.12.2 Automation of Coko-Werk GmbH & Co. Kg

5.12.3 Toyota Delivers Sustainable Agv Solutions for Panasonic Energy

5.12.4 Large Toyota Agv Fleet Helped Future-Proof Albert Heijn's Distribution Centers

5.12.5 Toyota's Automated Forklifts Supported Elm.Leblanc's 4.0 Journey

5.12.6 Inductive Charging System for Agvs

5.13 Technological Analysis

5.14 Trade Analysis

5.15 Regulatory Landscape

5.16 Key Conference & Events in 2022

6 Industrial Vehicles Market, by Vehicle Type & Capacity

6.1 Introduction

6.1.1 Operational Data

6.1.2 Assumptions

6.1.3 Research Methodology

6.2 Forklift

6.2.1 Growth of E-Commerce Industry to Drive Segment

6.2.2 Forklift Market, by Capacity

6.2.3 <5 Ton

6.2.4 5-10 Ton

6.2.5 11-36 Ton

6.2.6 >36 Ton

6.3 Aisle Truck

6.3.1 Increasing Adoption of Narrow Aisle Arrangements in Warehouses to Drive Segment

6.3.2 Aisle Truck Market, by Capacity

6.3.3 <1 Ton

6.3.4 1-2 Ton

6.3.5 >2 Ton

6.4 Tow Tractor

6.4.1 Increasing Focus on Automation in Manufacturing to Drive Segment

6.4.2 Tow Tractor Market, by Capacity

6.4.3 <5 Ton

6.4.4 5-10 Ton

6.4.5 11-30 Ton

6.4.6 >30 Ton

6.5 Container Handler

6.5.1 Steady Growth of Maritime Transport to Drive Segment

6.5.2 Container Handler Market, by Capacity

6.5.3 <30 Ton

6.5.4 30-40 Ton

6.5.5 >40 Ton

6.6 Automated Guided Vehicles

6.6.1 Growing Need for Automation in Material-Handling Processes to Drive Segment

6.6.2 Challenges of Agvs

6.6.2.1 Low Labor Costs Restricting Adoption of Agvs in Emerging Economies

6.6.2.2 Technical Challenges Related to Sensing Elements

6.7 Personnel Carriers

6.7.1 Increasing Levels of Industrialization to Drive Segment

6.8 Key Primary Insights

7 Industrial Vehicles Market, by Drive Type

7.1 Introduction

7.1.1 Operational Data

7.1.2 Assumptions

7.1.3 Research Methodology for Drive Type Segment

7.2 Ice Industrial Vehicles

7.2.1 Increasing Usage in Heavy-Duty Applications to Drive Segment

7.3 Battery-Operated Industrial Vehicles

7.3.1 Growing Co2 Emission Concerns Across the Globe to Drive Segment

7.4 Gas-Powered Industrial Vehicles

7.4.1 Suitability in Outdoor Applications to Drive Segment

7.5 Key Primary Insights

8 Industrial Vehicles Market, by Application

8.1 Introduction

8.1.1 Operational Data

8.1.2 Assumptions

8.1.3 Research Methodology for Application Type Segment

8.2 Manufacturing

8.2.1 Increase in Global Manufacturing Post-Pandemic to Drive Segment

8.2.2 Automotive

8.2.3 Metals & Heavy Machinery

8.2.4 Chemical

8.2.5 Healthcare

8.2.6 Food & Beverages

8.2.7 Others

8.3 Warehousing

8.3.1 Increasing Product Differentiation and Reduced Pallet Size to Drive Segment

8.4 Freight & Logistics

8.4.1 Need for Reduction in Delivery Time and Rising Concerns Over Damages and Loss of Goods to Drive Segment

8.5 Others

8.6 Key Primary Insights

9 Industrial Vehicles Market, by Level of Autonomy

9.1 Introduction

9.2 Non/Semi-Autonomous

9.3 Autonomous

10 Aerial Work Platform Market, by Type

10.1 Introduction

10.1.1 Operational Data

10.1.2 Assumptions

10.1.3 Research Methodology for Type Segment

10.2 Boom Lift

10.2.1 Growth of Construction Sector to Drive Demand

10.3 Scissor Lift

10.3.1 Growth of Logistics Sector to Drive Demand

10.4 Key Primary Insights

11 Industrial Vehicles Market, by Region

12 Competitive Landscape

12.1 Overview

12.2 Revenue Analysis of Top Companies

12.2.1 Market Share of Key Players

12.3 Competitive Scenario

12.3.1 Deals

12.3.2 New Product Launches

12.3.3 Others, 2018-2022

12.4 Company Evaluation Quadrant for Industrial Vehicles Market

12.4.1 Stars

12.4.2 Emerging Leaders

12.4.3 Pervasive

12.4.4 Participants

12.5 Sme Evaluation Quadrant for Industrial Vehicles Market

12.5.1 Progressive Companies

12.5.2 Responsive Companies

12.5.3 Dynamic Companies

12.5.4 Starting Blocks

12.6 Company Evaluation Quadrant for Aerial Work Platform Market

12.6.1 Stars

12.6.2 Emerging Leaders

12.6.3 Pervasive

12.6.4 Participants

12.7 Right to Win, 2018-2022

13 Company Profiles

13.1 Key Players (Industrial Vehicles Market)

13.1.1 Toyota Industries Corporation

13.1.2 Kion Group Ag

13.1.3 Mitsubishi Logisnext Co., Ltd.

13.1.4 Jungheinrich Ag

13.1.5 Crown Equipment Corporation

13.1.6 Hyster-Yale Materials Handling, Inc.

13.1.7 Hangcha Group Co., Ltd.

13.1.8 Clark

13.1.9 Anhui Heli Co. Ltd.

13.1.10 Konecranes

13.2 Other Key Players (Industrial Vehicles Market)

13.2.1 Komatsu

13.2.2 Doosan Industrial Vehicle

13.2.3 Manitou Group

13.2.4 Cargotec Corporation

13.2.5 Action Construction Equipment Ltd.

13.2.6 Hyundai Construction Equipment India Pvt. Ltd.

13.2.7 V. Mariotti Srl

13.2.8 Combilift

13.2.9 Daifuku

13.2.10 Jbt

13.2.11 Lonking Machinery Co., Ltd.

13.2.12 Hubtex Maschinenbau & Co. Kg

13.2.13 Godrej & Boyce

13.2.14 Svetuck Ab

13.2.15 Stocklin Logistik Ag

13.2.16 Omg Srl.

13.2.17 Paletrans Forklifts

13.2.18 Genkinger GmbH

13.3 Key Players (Aerial Work Platforms)

13.3.1 Jlg Industries, Inc.

13.3.2 Tadano Ltd.

13.3.3 Terex Corporation

13.3.4 Linamar Corporation

13.4 Other Key Players (Aerial Work Platforms)

13.4.1 Haulotte Group

13.4.2 Aichi Corporation

13.4.3 Palfinger Ag

13.4.4 Imer International Spa

13.4.5 Sinoboom Intelligent Equipment Co, Ltd.

13.4.6 Altec Industries

13.4.7 J C Bamford Excavators Ltd.

13.4.8 Noblelift Intelligent Equipment Co, Ltd.

13.4.9 Bronto Skylift

13.4.10 Snorkel

14 Analyst's Recommendations

15 Appendix

For more information about this report visit https://www.researchandmarkets.com/r/sf5v3e

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood, Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900