Yahoo Finance

Yahoo Finance

Global Over-the-Top (OTT) Market Report 2023: A 434.5 Billion Market by 2027 - Emerging Opportunities in Partnerships with National Producers and Film Studios Across Regions on SVOD Models

Global Over-the-Top (OTT) Market

Dublin, Feb. 20, 2023 (GLOBE NEWSWIRE) -- The "Global Over-the-Top (OTT) Market by Type (Game Streaming, Audio Streaming, Video Streaming, Communication), Monetization Model (Subscription-based, Advertising-based, Transaction-based), Streaming Device, Vertical, and Region - Forecast to 2027" report has been added to ResearchAndMarkets.com's offering.

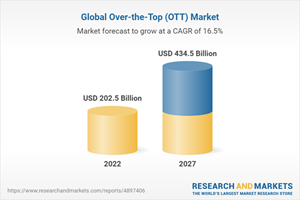

The global Over-the-Top (OTT) services market is expected to grow from USD 202.5 billion in 2022 to USD 434.5 billion by 2027, at a Compound Annual Growth Rate (CAGR) of 16.5%

During the pandemic, people were forced to be locked in their houses. This led to the rise in demand of OTT services during lockdown. Other factors such as global and local players offering freemium models in price-sensitive markets, internet proliferation with penetration of smart devices, and flexibility and ease-of-use to offer seamless customer experience resulted in high adoption of OTT services in developing countries.

Video Streaming type segment to grow at the highest CAGR during the forecast period

Due to the pandemic, people demanded new videos to be uploaded on the OTT platforms which were not related only to entertainment but to healthcare, news, information, education, tutorials etc. The pandemic gave rise to new small players in the OTT market which were focused on regional content and were adopted by the viewers at a high rate.

Existing players such as Roku, Netflix, Amazon Prime, and Apple TV saw an exponential rise in subscribers. The subscription-based VoD is expected to grow at a substantial rate, with users expressing their willingness to pay for premium services for streaming content.

Smartphones and Tablets streaming devices segment to lead the OTT services market in 2022

The vast majority of the world's internet users - 92.1% - use a mobile phone to go online at least some of the time, and mobile phones account for more than 55.7% of online time, as well as close to 60% of the world's web traffic. Smartphones and tablets thus prove to be the highest consumption devices for OTT services.

The major factors for smartphone and smart tv usage for OTT are optimized content delivery, improved mobile internet connection, and on-the-go high-definition streaming. The inception of OTT video streaming platforms, such as Netflix, Hotstar, and Amazon Prime leading to the growth of digital video consumption through these devices.

OTT entertainment apps have become the most penetrated app category among smartphone users after social networking, chatting, and eCommerce apps.

Subscription-based monetization model segment to grow at the highest CAGR during the forecast period

The subscription-based model is one of the most popular monetization models and requires fixed payment for a specific period. It is a business model where the user must pay a subscription price to gain access to video streaming services. The subscription fee may be charged daily, weekly, monthly, or annually, depending on the service opted for by the customer.

Once the user has paid for access, he can watch any number of videos on any device with sufficient internet access. This model benefits both the company and the customer due to the predictability of revenue for the company and monthly fee for the customer. Subscription pricing strategies can be made according to functionality, discounted to motivate bulk purchases, metered according to usage levels, or optimized to reward loyalty.

The subscription model depends on the time of day the service is used, is adjusted to motivate activity from geographic regions, and is term-based to secure long-term commitments or adjusted in cooperation with partner promotions and advantages of a subscription model for sellers.

The subscription-based model is widely adopted by consumers globally, as it empowers them to pay for the specific content they want and is a major reason audiences do not prefer cable and other traditional providers as much.

Media and entertainment service verticals segment to grow at the highest CAGR during the forecast period

COVID-19 has changed the way audience consume media and entertainment content. Initially the content was confined to TV, radio and cinema. However, with the digitalization of media and entertainment mediums, the consumers' can now access information or preferred channels at any time with their digital devices.

Major production houses in the media and entertainment service vertical are focusing aggressively on OTT platforms by releasing new, original content to keep the customers satisfied. Enterprises can easily communicate with their customers via messaging services.

By utilizing OTT messaging services, enterprises can interact with their consumers to deliver media and advertising content via rich messaging channels.

APAC OTT services market to grow at the highest CAGR during the forecast period

Major economies in the Asia-Pacific (APAC) include China, India, Japan, Australia and New Zealand. The proliferation of smart devices, the availability of broadband, and internet connectivity, adoption of advanced technologies such as 5G, 4G, large number of subscribers due to high population, and a dynamic local content ecosystem, are few major reasons for the growth of OTT services market in this region.

This region has also seen a major rise in local or regional OTT content providers post pandemic. People in this region want to view content in their local languages which are more related to their local culture. Due to this, the OTT market has a high demand for upcoming OTT players in this region.

Existing players offering Video Streaming such as YouTube, iQiyi, Tencent Video, ByteDance, Netflix, Amazon, Hotstar, and Hulu Japan, will account to a major share of revenue along with the huge penetration of instant messaging apps, such as WhatsApp, Facebook Messenger, Line, and WeChat.

Competitive landscape

Some prominent players across all service types profiled in the study include Meta (US), Netflix (US), Amazon (US), Google (US), Apple (US), Home Box Office (US), The Walt Disney Company (US), Fandango Media (US), Roku (US), Rakuten (Japan), IndieFlix (US), Tencent (China), and Kakao (South Korea).

Key Metrics

Report Attribute | Details |

No. of Pages | 180 |

Forecast Period | 2022 - 2027 |

Estimated Market Value (USD) in 2022 | $202.5 Billion |

Forecasted Market Value (USD) by 2027 | $434.5 Billion |

Compound Annual Growth Rate | 16.5% |

Regions Covered | Global |

Premium Insights

Rise in Number of Partnerships Between OTT Vendors and Content Producers to Support Over-The-Top Services Market Growth

Smartphones & Tablets to Account for Highest Market Share in 2022

Smartphones & Tablets and Subscription-based Monetization to Account for Largest Respective Market Shares in North America

Smartphones & Tablets and Advertisement-based Monetization to be Largest Respective Segments in Asia-Pacific

Market Dynamics

Drivers

Flexibility and Ease-Of-Use to Offer Seamless Customer Experience

Internet Proliferation with Penetration of Smart Devices

Freemium Models of Global and Local Players in Price-Sensitive Markets

Rise in Demand for Over-The-Top Services During Lockdown

Restraints

Disparity in Opinion Between Producers and Aggregators Over Licensed Business Model

Threat to Privacy of Content Consumption and Security of User Database due to Spyware

Inadequate Supply of High-Speed Internet in Emerging Economies

Opportunities

Partnership with National Producers and Film Studios Across Regions on SVOD Models

Adoption of 5G Technology

Challenges

Complex IP, Government Regulatory Frameworks, and Licensing Regimes Across Regions

Difficulty in Retaining Subscribers due to High Competition

Industry Trends

Ecosystem Mapping

Supply Chain Analysis

Company Profiles

Amazon

Apple

ByteDance

Facebook

Fandango Media

Google

HBO

Hotstar

Hulu Japan

IndieFlix

iQiyi

Kakao

Line

Meta

Netflix

Rakuten

Roku

Tencent

The Walt Disney Company

WeChat

WhatsApp

YouTube

For more information about this report visit https://www.researchandmarkets.com/r/f4ge03-over-the?w=12

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood,Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./ CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900